You can’t say Bill Dudley wasn’t direct.

“I changed my mind,” Dudley said Wednesday. “The Fed needs to cut rates now.”

That was actually the title of an Op-Ed Dudley penned for Bloomberg Opinion.

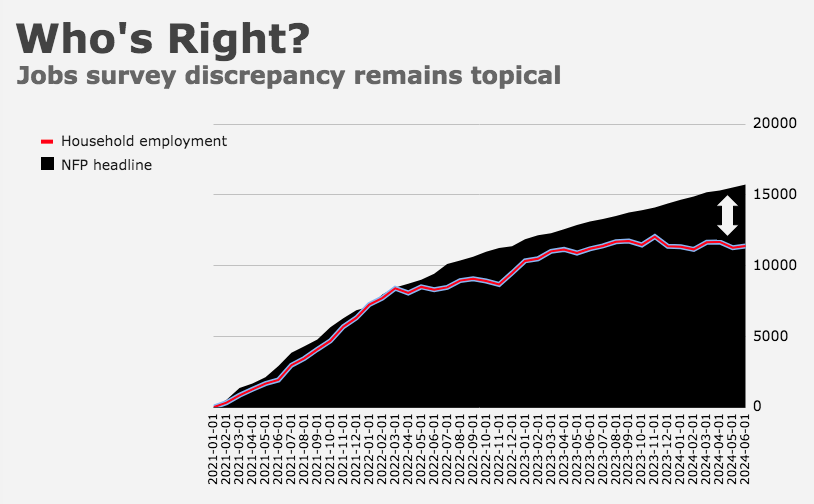

In explaining his about-face, the erstwhile higher-for-longer advocate pointed to mounting evidence of a slowdown, including the yawning disconnect between the household and establishment surveys in the monthly jobs report, the JOLTS-derived openings-to-unemployed ratio (which he noted is back to pre-pandemic levels) and, of course, the Sahm Rule.

The figure above shows Claudia’s eponymous recession indicator, the only indicator with a better track record than the yield curve. Long story short, it’s on the brink of triggering.

Dudley went on to cite a series of benign reads on inflation to help make the case that if the Fed’s really interested in landing the proverbial plane softly, the time for so-called “insurance cuts” is now. Where “now” means beginning at next week’s meeting.

But the Fed isn’t going to cut next week. Why not? If September’s a lock anyway (and it probably is) why wait? Dudley offered that the Committee’s suffering from PTSD and doesn’t want get “fooled again” by inflation head fakes. Further, Powell may be keen to get unanimous, unequivocal buy-in from his colleagues before embarking on cuts with core inflation still running well above target. Finally, Dudley mused, “Fed officials don’t seem particularly troubled by the risk that the unemployment rate could soon breach the Sahm Rule threshold,” perhaps given assumptions about immigration (i.e., a larger workforce) being the cause of a higher jobless rate.

Dudley doesn’t find any of those excuses compelling, or at least not to an extent that should stop Powell from cutting at this month’s meeting. In fact, Dudley suggested it might already be too late to avert a recession.

Of course, the real, practical reason the Fed can’t cut next week is that markets aren’t priced for it. At all. If you’re the Fed, you can’t deliver a cut when the market-implied odds of a move are negligible. You’ll scare everybody to death. Dudley should know that. Does know that. Dudley surely knows that.

Writing in a Wednesday note, Nomura’s Charlie McElligott spelled it out. “The difference between the currently-priced ‘two insurance cuts by year-end’ scenario and that outright Dudley ‘surprise July cut,’ is monumental: Client convos on the ‘Why Wait?’ scenario are absolutely consensus as to how equities would respond to a July cut,” he said. “Everybody [is] saying stocks would get absolutely smoked on that ‘Man, it must be really bad’ perception.”

Invariably, someone (which is to say a lot of people) will claim Dudley’s playing politics. That he’s trying to goad the Fed into rate cuts in order to preempt a recession between now and November. I won’t weigh in on that other than to say it’s irrelevant: 25 “early” basis points (i.e., a cut in July) isn’t going to make a shred of difference if a recession’s that imminent. If Bill wanted to influence the election, he should’ve started earlier.

{kind=link}

They could announce their intention to cut rates soon at the july presser. They could announce a date certain end of qt at the July meeting. Powell could follow up with a dovish speech at Jackson hole. Finally, they could wait until September and throw a fifty at that meeting. I would recommend all of the above.

If rate cuts take time to flow through the real economy and we’re already on the verge of a potential recession what good would even a 25bps cut do now? It would almost make more sense to wait until September and do something significant like a 50bps reduction which again might not do much in the short term but could have a medium to longer term impact.

Does that mean someone pushed the down button on the elevator? The Fed is looking for the stairs and the rest of us are just waiting for the ding and the doors to open.

Time to bring back Alan Greenspan’s crystal ball. At least it was clear they were winging it back then versus the current hand wringing over dot plots. I agree that a quarter point is already priced in and won’t make a hill of beans difference in where the economy is going. In my experience from the 70s the Fed has generally been behind the curve and too heavy handed when it finally is forced to act.