JPMorgan fired the starting gun on US earnings season Friday with what looked like a beat on most key metrics. There was an important caveat: Q1 NII looked a little short, as did the full-year forecast.

Net interest income for the quarter rose 11% YoY to $23.20 billion. The Street wanted $23.22 billion. Excluding First Republic — which Jamie Dimon bought “way” back last year after a botched rescue attempt — NII rose 5%.

As the figure below shows, Q1 marked the first sequential NII decline (-4%) since the Fed started hiking rates.

JPMorgan sees full-year NII of $90 billion ($89 billion ex-Markets). “Market dependent,” of course.

That’s a bit of a let down. I don’t mean to suggest the shares are destined to retreat in the near-term (trying to predict how bank shares will behave in the immediate aftermath of earnings releases is a fool’s errand), but analysts were looking for something closer to $91 billion on the full-year NII guide. So, $90 billion probably won’t cut it.

Speaking of cutting it (or not, in this case), the NII situation’s pretty fluid. The FOMC’s best-laid plans (with allowances for the Committee’s shrill “The dot plot’s not a plan!” protestations) were upended in recent weeks by resilient US macro data and a trio of stubborn CPI reports. A higher (or just high, without the “er”) for longer rates regime has implications for banks’ NII.

The rest of the numbers from Dimon were fine. FICC revenue of $5.30 billion fell YoY but constituted a beat nevertheless (consensus was something like $5.20 billion).

The bank cited lower activity in Rates and Commodities versus Q1 of last year for the FICC drop-off, with securitizations picking up the slack.

Equities revenue was flat at $2.70 billion. Consensus was $2.50 billion there. Overall, Markets revenue fell 5% to $8 billion (the figure above includes Securities Services).

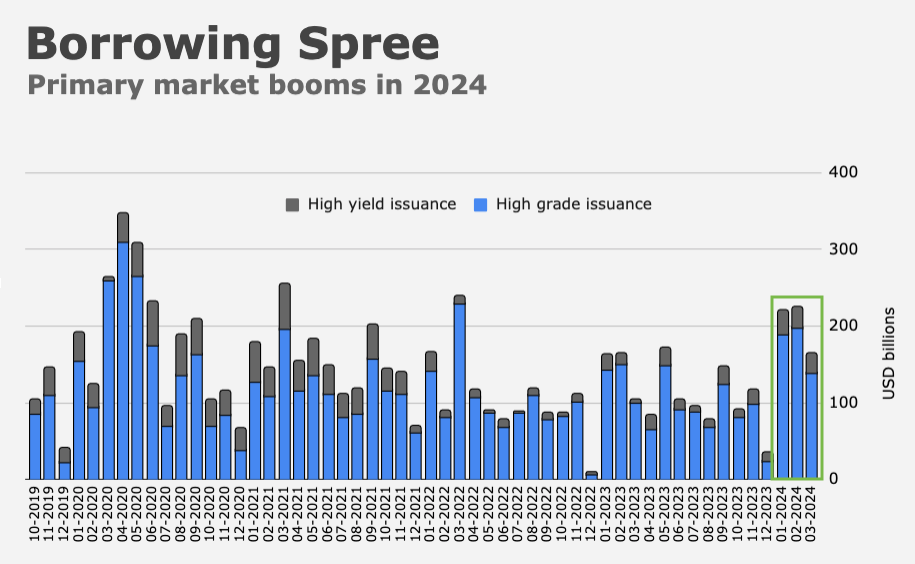

Debt underwriting picked up dramatically. Revenue of $1.048 billion was the most for any quarter since Q4 2021. Consensus expected just $778 million.

The first quarter, you’ll recall, saw a veritable tsunami of corporate issuance, including blockbuster high grade supply.

Equity underwriting remained subdued, but revenue of $355 million was a beat too. Consensus was looking for $342 million. Overall IB revenue of $1.99 billion comfortably topped the $1.81 billion estimate.

On the top and bottom lines JPMorgan beat. Adjusted revenue of $42.5 billion was $900 million ahead of consensus and EPS of $4.44 ($4.63 if you exclude an increase in the FDIC special assessment) easily eclipsed the $4.17 estimate. The bank’s expense guidance for the full-year, at $91 billion, looked a little high. Total deposits were $2.428 trillion. Loans were $1.31 trillion (that was a miss).

Dimon reiterated some boilerplate talking points around NII, which’ll likely normalize going forward. As is custom, he cautioned on an uncertain world. “Terrible wars and violence continue to cause suffering, and geopolitical tensions are growing,” he said Friday, adding that “there seems to be a large number of persistent inflationary pressures, which may likely continue.”

Of course, JPMorgan will be fine come hell or high water. The firm’s “prepare[d] for a wide range of potential environments to ensure that we can consistently be there for clients,” Dimon promised.

All in all, markets may be a little fussy about the ostensible NII undershoot (and upside expense guide), but other than that, JPMorgan’s results were fine. Or “strong,” as Dimon put it.

{kind=link}