It’s the liquidity! It always is.

Last year was remarkable for a number of reasons, not least of which was the “unusual combination of higher rates and equity valuations in the context of weak earnings growth,” as Morgan Stanley’s Mike Wilson put it this week.

You’ll recall that the US did experience a shallow profit recession. Suffice to say stocks, to the extent they priced it in at all, did so preemptively, in 2022, when rising rates and a dramatically bad year for bonds undercut equities.

Although some worry we could be in for a double-dip profit downturn, the earnings recession ended in Q3. Corporate bottom lines will show growth for Q4 as well.

Still, Wilson’s correct to suggest there was something a bit odd about a conjuncture that found equity multiples expanding despite stubbornly elevated real rates and negative aggregate YoY profit growth for three consecutive quarters.

What explained that? Well, as noted here at the outset, it was the liquidity, with a fiscal kicker.

“It’s not typical to run elevated deficits with unemployment as low as it is,” Wilson remarked, noting that not all of the deficit was intentional.

“The take up rate on the Inflation Reduction Act proved to be greater than expected and tax receipts were well below expectations,” he said, adding that rising inflation meant big COLA increases.

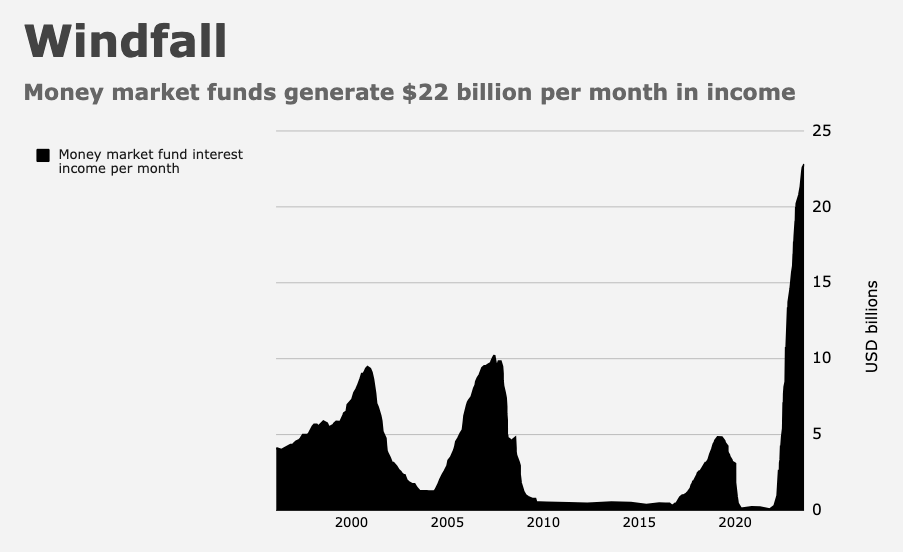

I’d quickly note that an estimated $22 billion in monthly interest income for those fortunate enough to have large sums parked in money market funds probably helped too. Ironically, the Fed’s rate hikes might’ve subsidized spending through that channel, at least for consumers with meaningful “cash” investments.

As for monetary support, the Fed raised rates, but thanks to depositor bailouts and RRP drain, liquidity conditions remained very forgiving. Indeed, despite QT running in the background and in the face of massive T-Bill issuance, reserves actually rose.

As discussed here on too many occasions to count, RRP transformation (i.e., MMFs rotating out of the facility to absorb bill supply) was a crucial systemic stabilizer in 2023.

To cap it all off, Treasury’s (wise) decision to acknowledge the term premium increase witnessed from late-July through October (where “acknowledge” means coupon increases in the November refunding were lower than expected), and the Fed’s dovish pivot, eased financial conditions materially over the final two months of the year.

The figure above is familiar by now. But it really is crucial to internalize the message.

Things should be different in 2024, Wilson said. At least on some fronts. “The liquidity picture is unlikely to be as supportive this year given the extent to which the reverse repo has already been drained,” he wrote. “Further, the Bank Term Funding Program is scheduled to end in March and the likelihood of an extension isn’t clear given the loosening in financial conditions.” (For more on the BTFP point, see here.)

All of that said, Fed cuts and the likely end of balance sheet runoff may help cushion the blow as 2023’s liquidity tailwinds fade. Although Lorie Logan was keen to emphasize during a speech on January 6 that easier financial conditions could make it harder for the Fed to finish the job on inflation, she also began the process of socializing the discussion around slowing QT. That was arguably more important than her remarks about the recent FCI easing.

“While the current level of ON RRP balances provides comfort that liquidity is ample in aggregate, there will be more uncertainty about aggregate liquidity conditions as RRP balances approach a low level,” Logan said. “Given the rapid decline of RRP, I think it’s appropriate to consider the parameters that will guide a decision to slow the runoff of our assets.”

Oh, and don’t forget: It’s an election year. So…

{kind=link}

What is your view of the importance of US M2’s unprecedented stagnation?

Interesting question! +1

From the lower panel of the chart, it seems like from Mar 2023 to now about $1TR of liquidity was added.

How does that compare with the $6TR of cash in MMF? Suppose that $2TR of that is money that normally lives in bank deposit accounts, and investors are carrying cash 2X normal levels. Thus suppose up to $2TR of cash in MMF are available to move back into longer-duration investments.

Does that imply there is significant additional liquidity potentially available? Maybe not using the strict definition of liquidity, but in the sense that there is cash that can flow into markets without coming from bank reserves.

I was, by the way, surprised to see that bank deposits are only down about -$0.3TR since Mar 2023 https://fred.stlouisfed.org/graph/fredgraph.png?g=1dU1o