The great thing about 4% or 5% on term deposits and federal money market funds is that it’s riskless free money.

Admittedly, the “full faith and credit” pledge sounds more ironic all the time in light of acute dysfunction inside the Beltway, but for now, T-bills are as good as cash and an FDIC guarantee is as good as… well, as good as gold in the literary sense, if not in the convertibility sense. Hell, we even learned in March that when push comes to shove, FDIC insurance actually extends to all deposits, not just those under the official limit.

So, for no risk at all you can earn between 4% and 5% on USD cash. It’s not a bad deal. Particularly now that inflation is below 4%. Or at least according to the BLS.

The bad thing about 4% or 5% on riskless cash and cash equivalents is that it’s not 40% or 50% which is what you could get gambling on the next viral chatbot by way of an index fund that charges just a handful of basis points to faithfully track a cap-weighted benchmark dominated by an omnipresent oligopoly.

In 2022, you wanted the high-yielding cash because, as a direct result of the policy decisions pushing up yields on your riskless dollars, shares of the oligopoly were de-rating rapidly. In 2023, mega-cap multiples stopped caring about high yields, though, and as a result, your cash underperformed significantly.

But that 2023 underperformance didn’t stop folks from piling into money market funds. Indeed, 2023 was a year like no other for MMF AUM, which ballooned by $1.1 trillion (and counting).

That’s a lot of dry powder. Notwithstanding the first outflow in two months during the latest weekly reporting period, it may keep accumulating for a while yet. Unless, of course, too many investors catch a bad case of FOMO. Hold that thought.

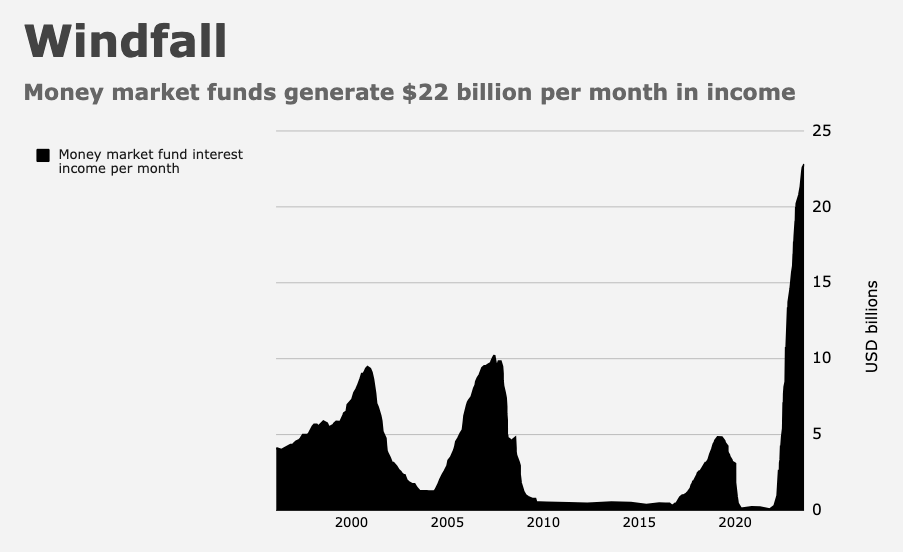

While sitting on the proverbial sidelines, MMF cash served two important purposes. It bolstered consumption through the interest income it generated (some $20 billion per month) and it helped prevent a liquidity squeeze through the MMF-RRP-T-bill nexus, wherein money funds rotated out of the Fed’s parking garage and into bills, mitigating reserve drain as Treasury rebuilt its cash balance.

From the day the debt ceiling deal was done in early June through the end of November, RRP drained by $1.3 trillion.

All of the above presents an interesting conundrum for the first half of 2024. On one hand, $6 trillion in money fund AUM could be a source of funds for a melt-up in risk assets. On the other hand, MMF redemptions could remove a key systemic backstop at a delicate juncture.

With that in mind, consider the following excerpts from a Thursday note penned by Nomura’s Charlie McElligott, who sketched the contours of a $6 trillion question while looking ahead to January.

How do you fund [a] chase into risk assets now that the Fed and other central banks look set to preemptively commence easing before the recession hits? Well, let’s just say that the the 4.00-5.00% you were picking up in money market funds over the past 1.5 years looks increasingly unattractive now in light of a world where fixed income yields are again cratering lower against massive price appreciation from risk assets thanks to impulsive global FCI easing and the perception of benevolent central banks going forward. As investors look at the paltry returns from the past few years, they inherently want to FOMO into said benevolent policy easing backdrop, which then increases the risk of ‘MMF as source of funds’ to chase further out onto the risk curve. [The] implications of MMFs as a source of funds for a market melt-up are twofold as far as feeding divergent ‘tail’ scenarios:

- MMF assets at all-time highs can easily provide fuel for the fire to get us a crash-up to fresh all-time highs in equities and chasing into other risky assets as investors re-gear portfolios into long risk exposures via this extremely ‘QE-like’ portfolio rebalancing channel which the Fed just kicked off.

- [But] at the same time, MMF redemptions could risk disrupting the profound calm that MMF cash has provided the market in absorbing the big potential ‘liquidity shocks’ in 2023, lapping up supply with perpetual demand for bills through non-stop asset inflows. The case of hypothetical MMF redemptions then risks losing / draining this lubricant, at the same time that RRP is being drawn down and QT continues, as a potential catalyst for the much-discussed repo / front-end shock if we begin having to aggressively reprice paper to make issuance clear.

For now, this is not a threat due to ongoing lubrication currently available in the system, but it could be down the road, and ironically in the case we get said potential MMF redemption drain to chase into risky assets instead.

{kind=link}