“It’s quiet. Too quiet,” as the old cliché goes.

As the new week dawned, some market observers were keen to note that the outcome distribution for US equities recently compressed.

Specifically, it’s been a dozen sessions since the benchmark moved up or down by more than 1%.

On one simple calculation (illustrated above) the index is at least as calm as it’s been at any other point this year.

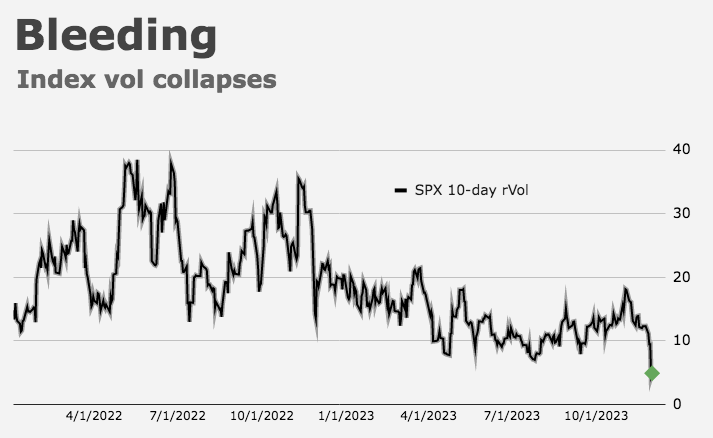

Needless to say, that’s mirrored in both realized and implied vol. 10-day rVol, regular readers will recall, collapsed almost entirely in recent days.

The figure below shows the range compression alongside one-month realized.

As ever, that’s conducive to a latent bid from the vol control universe. Indeed, on Nomura’s estimates the mechanical reallocation bid from that space was almost $46 billion over two weeks.

Vol-selling is a factor. And vol-selling can perpetuate itself. I went over this again and again in recent days, but one account of the “eerie calm” published by the mainstream financial media on Sunday didn’t mention the relevant dynamics (although it did note that the sudden calm may be fortuitous, not scary). The vol expansion that accompanied the three-month selloff in rates and equities from August to October was a prime short candidate in the event the macro-policy backdrop shifted, which it did over the last three/four weeks.

I’ll recycle a short excerpt from a Friday note penned by Nomura’s Charlie McElligott. “[The] current SPX index vol zeitgeist is a function of incessant index vol-selling across the usual suspects, creating a dynamic where dealers and market makers are getting stuffed on bleeding gamma / vega, which then forces them to ‘join the parade’ and short front-end vols themselves, in order to stop the PNL bleed.” So, they’re shorting near-dated vol into the decline.

As discussed here over the weekend, the current setup isn’t necessarily indicative of complacency. “The ‘mechanical’ conditions for a disorderly equities selloff are simply not in place at this juncture,” McElligott wrote, noting that the absence of demand for downside protection is in no small part a function of relatively subdued underlying equities exposure. The only “tail” demand is in right-tail expressions — i.e., crash-up protection.

“Everyone’s emotionally bullish, but still intellectually bearish, and likely to stay that way,” BofA’s Michael Hartnett said. Note that although the contrarian “buy” signal on the bank’s pseudo-famous “Bull & Bear Indicator” ended late last month, at just 2.7 the indicative metric is nowhere near neutral to say nothing of the 8 level it’d need to achieve to trigger a “sell” warning.

Now let me go knock on some wood and find a rabbit’s foot before it all falls apart.

{kind=link}

How do you predict a year like 2017?

I can’t remember who it was (Marko?) who referred to the Yellen Fed as a “supplier of convexity,” but it really feels like the Federal Reserve is well positioned to reprise that role this year.

First, they have the option to end QT, second, they have the option for “insurance cuts” where they yell, “It’s not a cut! We just want to avoid mechanical tightening from rising reals!”

A steady supply of convexity makes for smooth sailing. (Assuming, of course, we don’t go to war with China.)

That was Aleks Kocic at DB. He’s retired now.