On the heels of an exceedingly unfortunate three months during which both equities and bonds sold off simultaneously, some key investor cohorts were under-positioned.

Meaningful exposure reductions left those investors vulnerable in the event of a rekindled rally. That was part and parcel of the “Santa melt-up” blueprint as sketched here early last week.

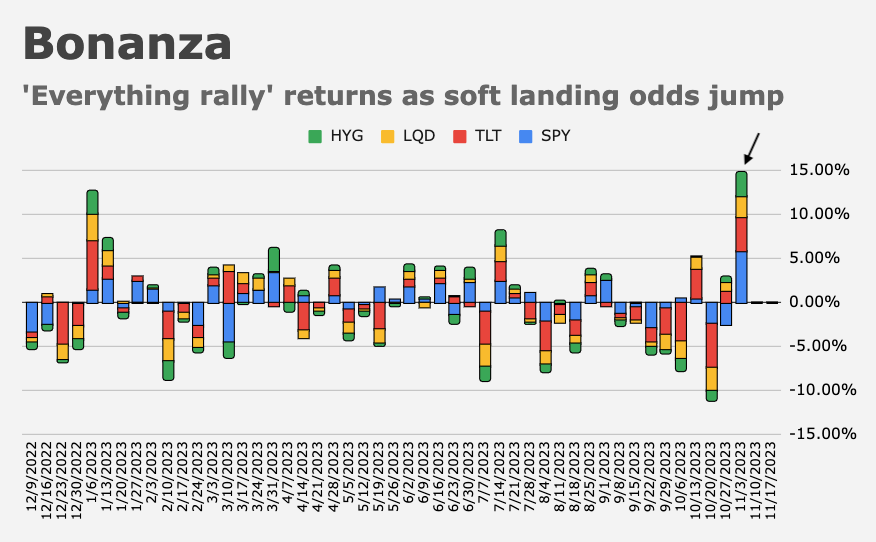

Within days, US equity futures were 6% higher, spurred on by a sharp drop in long-end US yields. Equities notched their best week in a year and 10-year Treasurys their best week since SVB. High grade credit and junk were along for the ride. The “everything rally” was back.

Given the stark juxtaposition between the big surge for stocks and the under-positioning mentioned above, it’ll come as no surprise that last week was “just awful” for the macro universe and also for the long/short crowd.

“We knew the US equities ‘downside hedge unwind into delta chase to the upside’ was coming,” Nomura’s Charlie McElligott said Tuesday. “I’d been stating for the past few weeks [that] the largest pain trade would come in the form of a beta rally, when nobody has any net on, so the past one-week period in particular was just awful for macro and L/S funds.”

As the figures above show, the sudden turn led to anomalous underperformance, where that means 1%ile and below. Note that macro funds were particularly hard-hit.

McElligott talked last week about the prospect of winners being monetized on the year-end approach. He touched on that again Tuesday. “The trader mentality over the past month has been about ‘monetizing (rare) winners with extreme prejudice’ in a year where performance has been difficult to come by,” he said. “The ‘good news’ here is that the downside hedges did their job, and enabled many to close the trades and roll those profits immediately into upside expressions to chase the rally.”

As noted here at least twice last week while editorializing around the sequencing which ended up playing out over a few days rather than over a few weeks or two months, additional gains for equities which prompted more downside hedge bleed would lead to large delta-to-buy and a reset lower for both vol and vol-of-vol. Charlie on Tuesday described the positive delta impulse as “biblically-massive.”

The tables above show a 100%ile delta surge event. “Puts were unwound, calls were grabbed into and skew got mushed,” McElligott added.

So, what now? Well, hopefully not a series of new US macro escalations. Hot data could reverse last week’s macro “softness” which, together with Treasury’s (wise) decision to undershoot expectations for coupon increases, catalyzed the bond rally underpinning the bullish cross-asset tone.

In that case (i.e., in the presence of another run of hot data), we’d be right back into the maddening, FCI reflexivity hall of mirrors. Indeed, you could argue we’re already there thanks to the return of the “everything rally.”

“Ironically, it’s the duration rally and easing of financial conditions which again threatens the whole trade,” McElligott wrote, summing up. “The risk to all this bond / STIR bullishness becomes another ‘resilient data’ setback, hypothetically then forcing the market to adjust” expectations for Fed easing, which “then acts like a fresh tightening of FCI.”

And around we go.

{kind=link}