“When you give roses to others, the fragrance lingers on your hand.”

So said Xi Jinping on Wednesday, when China convened 130 countries to discuss and otherwise celebrate the 10th anniversary of the Belt and Road initiative, Xi’s pet global infrastructure project.

It was the biggest gathering China’s hosted since the pandemic, and it came on a day when Beijing unveiled crucial economic data.

The Chinese economy expanded 4.9% YoY in Q3 and 1.3% from the previous quarter, the NBS said. Those figures were better than expected, and suggested China will meet its full-year growth target with relative ease.

The sell-side lifted its full-year GDP forecasts in light of Wednesday’s numbers, but a word of caution: It’d be naive to take the data completely at face value.

As ever, I’m not suggesting the figures are fabricated, per se. All I’m saying is that in an autocratic, centrally-planned state where the regime depends heavily on economic performance to legitimize its grip on power, it’s not unreasonable to suggest that officials are under immense pressure to manage the data such that the economy meets or exceeds stated (and state) targets.

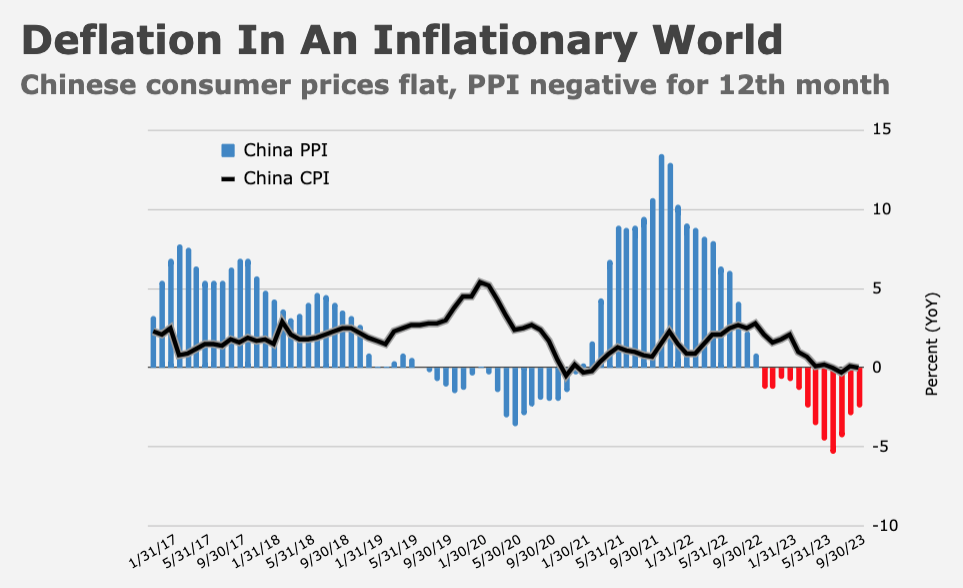

Some observers went far further on Wednesday. Producer prices in China are mired in deflation, and one economist at S&P Global said Chinese officials are “basically overstating real growth” when PPI falls, and quite possibly by a lot. In addition, Q2 growth was revised lower, which flattered the Q3 figures.

Activity data for September, released concurrently with the GDP figures, was suspiciously better where it needed to be and conspicuously weak where it was difficult to suggest otherwise. Retail sales rose 5.5% YoY, considerably better than the 4.9% consensus.

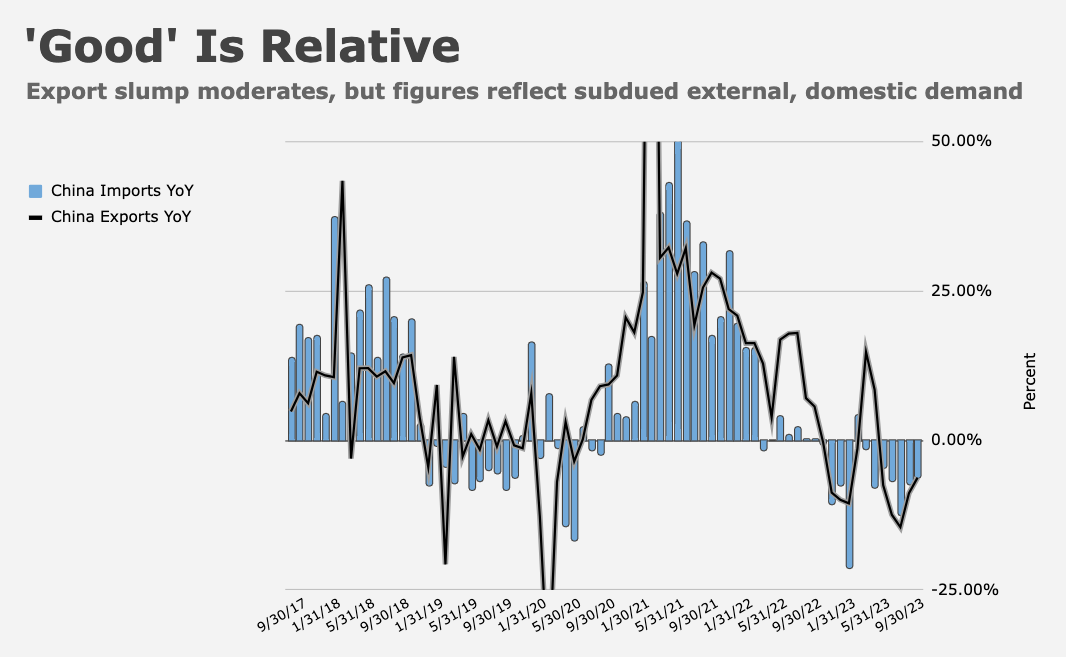

China really (really) needed to show evidence that domestic demand is picking up. CPI data released last week suggested consumer price growth is still flirting with deflation. Imports are mired in a seven-month contraction. A poor retail sales print would’ve underscored concerns about an anemic domestic consumption impulse.

Industrial output rose 4.5% last month, China said. That was 0.1% ahead of the 4.4% consensus. Fixed asset investment missed. The cumulative increase for the nine months through September was 3.1%. The YTD decline in property investment, which it’d be impossible to flatter without raising eyebrows under the circumstances, deepened to 9.1%.

I should be clear: It’s not as if China publishes these figures and walks off the proverbial stage. The statistics bureau releases a detailed breakdown, and as you’d expect, it suggested that retail sales were less robust in categories with links to property and real estate. Officials also reiterated what, by now, are familiar concerns around lackluster domestic demand and a very challenging external environment.

So, there is transparency. And there is an effort on the part of the NBS to be forthcoming about the myriad downside risks. And there is plenty of underlying data for analysts to sort through on the way to refining their forecasts and views.

Sometimes I forget I’m writing for generally audiences, and I wouldn’t want to give the impression that Chinese economic data are literally made up. They’re not. When I use terms like “made up” in this context, it’s an allusion to the notion that centrally-planning an economy the size of China’s is impossible, almost by definition. So when you see the main aggregates meet expectations or beat by a little bit or miss by a little bit, and the overarching takeaway is that the Party has succeeded in managing growth to meet a fairly specific target, it’s hard not to harbor doubts about the veracity of the narrative, while not necessarily implicating the NBS in crimes against statistics.

Whatever the case, China needs more stimulus. Even if you think the figures are 100% accurate and the NBS is the most forthcoming institution on the planet, the data unequivocally points to a still struggling property sector and a domestic consumption impulse that needs help if it’s expected to sustain a recovery amid fragile sentiment.

Tellingly, Chinese property stocks retreated to a 14-year low on Wednesday amid renewed concern around Country Garden, which looks likely to default. Evergrande faces a liquidation order later this month.

Xi and Vladimir Putin, in back-to-back speeches Wednesday, played up Belt and Road as a compelling economic alternative to the “old” world order. The soundbites were predictably farcical. Putin said Russia and China aspire to “equal and mutually beneficial cooperation” for all nations in the interest of promoting “universal sustainable and long-term economic progress” which “respect[s] the right of each state to its own development model.”

Russia is increasingly dependent on Xi after being cut off from Western markets and the dollar-based financial system last year. I’ve called Russia a vassal state of China. That’s not an exaggeration, or at least not economically. The economic asymmetry between the two countries is profound. Russia’s economy is smaller than Italy’s. China’s is the second-largest on Earth.

For his part, Xi painted Belt and Road, which has been criticized for being nakedly exploitative and an instrument of Chinese foreign policy, as a win-win for everyone involved. He also characterized himself as a benevolent force for good in a world of egotistical, selfish fiends. “Helping others is also helping oneself,” he said. “Viewing others’ development as a threat or taking economic interdependence as a risk will not make one’s own life better or speed up one’s development.” It was a thinly-veiled critique of America’s efforts to restrict the PLA’s access to advanced technology.

Later, after a three-hour bilateral, Putin said the two dictators spent at least 60 minutes commiserating about “confidential topics.” The discussion, he said, was “productive and meaningful.”

The event marked Putin’s second foreign trip since the ICJ called for his arrest in connection with allegations that Russia is engaged in the systematic kidnapping of Ukrainian children. Putin also held a bilateral meeting with Viktor Orban, the only EU leader to attend Xi’s summit.

{kind=link}

{kind=link}

That China, Russia, and Iran are all allied (or “axis”?) together despite absolutely fundamentally different core beliefs and economies tells me “The West” (plus the non-West Japan, South Korea, Australia, etc) are all doing a pretty good job.

Sadly the naive do not understand how fallible we all are, some more fallible than others… such that Orban, La Pen (father and daughter), and He-Who-Must-Not-Be-Named are “upright leaders” who can win elections because they’re appealing (ignore the where the money comes from, nothing to see here!).