Who’s going to buy all the bonds?! Shrieked the audience.

Although there’s still no firm consensus on what, exactly, was behind recent volatility at the US long-end (and the accompanying rise in the term premium), a simplified narrative says the market is finally pricing the implications of increased supply (i.e., more issuance) to fund bigger deficits at a time when price-insensitive buyers (including and especially the Fed, but also banks, FX reserve managers and foreign investors) are stepping away from the market.

Here’s a slightly longer version, as recounted by Goldman’s David Kostin:

The US federal debt-to-GDP ratio averaged 43% from 1970-2019. GS Economics forecasts debt/GDP will exceed 100% by fiscal year 2025 and will rise to 123% over the next decade. The deterioration of the federal government’s fiscal position has been led by a ballooning deficit. “Higher-for-longer” yields will increase the interest expense of the federal government in coming years and contribute to the widening budget deficit. GS Economics expects the deficit will reach $1.9 trillion by FY 2025, nearly double the $984 billion level of FY 2019, and account for 28% of federal spending, up from 22% in the fiscal year ending October 2019, just prior to the arrival of COVID. Rising deficits must be financed by Treasury issuance: Our rates strategists expect nearly $2 trillion of Treasury issuance in calendar year 2023, with $1.6 trillion of issuance already completed through September. Treasury issuance during calendar year 2022 totaled $1.4 trillion. This increasing issuance alongside quantitative tightening has led investors to worry about a supply/demand imbalance in Treasury bonds.

Is this something to worry about? I don’t know, honestly. Deficits don’t matter for the US in and of themselves, and Treasurys aren’t properly “debt,” but for my sanity and yours, I’ll sidestep that discussion and pretend. If price-insensitive buyers step back, price discovery will reassert itself (“Make Markets Markets Again”), which means the “cost” of issuing interest-bearing dollars will be higher. If you issue ever more of those obligations and the market continues to demand more to purchase them, it’s ostensibly problematic, particularly if the market’s concerns center around the suspicion that the US is experiencing a crisis of government.

Ultimately, though, the allure of relatively high yields and the prospect of capital appreciation in a rally should underpin demand. Goldman, for example, doesn’t believe a supply/demand mismatch will push yields materially higher from recent peaks. “Treasury yields are likely to remain contained given the attractive risk/reward of owning a ‘risk free’ asset yielding well in excess of the economy’s potential growth rate,” Kostin wrote.

Recall that the return asymmetry for bonds for a given move in yields is now highly skewed, where that means very favorable. If you ask BofA’s Michael Hartnett, recent Fed rhetoric (i.e., Fedspeak centered around the notion that the tightening in financial conditions seen in August and September can stand in for the final rate hike tipped by the dots) suggests 5% for long-end Treasury yields is “clearly a big line in the sand.”

Last week’s fireworks — as dovish Fedspeak and a haven bid tied to events in the Mideast collided with a poor 30-year auction to whipsaw bonds — pushed up volatility on the largest Treasury ETF.

Although the volatility (and expectations of more to come) is plainly a concern when it emanates from a market which purports to be the deepest, most liquid on Earth and from an asset which is supposed to be a bastion of stability in portfolios, the pushback from the Fed as 30-year yields kissed 5% and 10-year yields looked poised to make a run at a five-handle too, should’ve been a clarion call for bears keen to press their luck.

Even if that’s not the correct interpretation of Fed communications in October, the turmoil in Israel was a reminder that exogenous shocks do come along from time to time, and when they do, investors’ first instinct is very often to grab for USD duration.

Coming full circle, if the question is who’s going to buy the bonds, one answer is… well, people. Households bought almost $700 billion in Treasurys during the first half, according to Fed data, but as Goldman noted, a lot of that is the other side of the basis trade, given that hedge funds are counted in the “household” category.

Households own just 9% of the market versus nearly 40% of the US equity market.

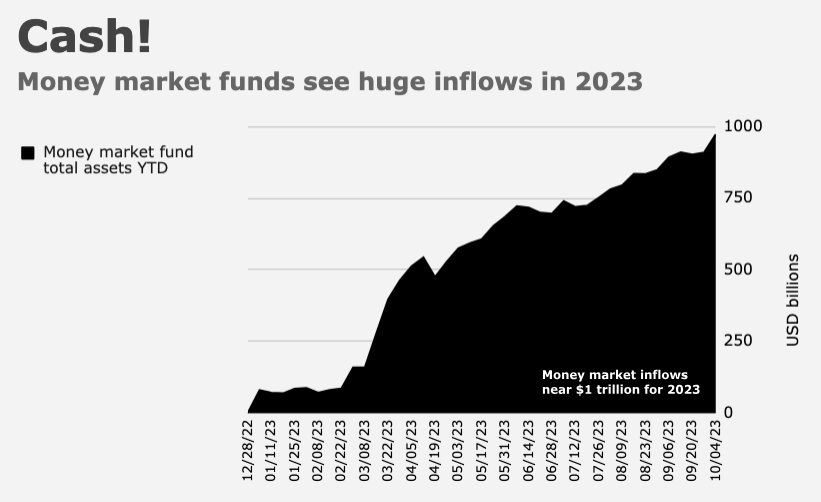

BofA’s private clients now hold 15.4% of their AUM in cash and T-bills, well above the long run average and consistent with levels seen in the dash-to-cash panic following the onset of the pandemic, while money market AUM is up $1 trillion in less than a year.

In the event the economy goes south and the market starts to anticipate rate cuts, investors expecting lower cash yields may see a big opportunity in oversold long-end bonds.

There’s “loads of cash” on the sidelines, BofA’s Hartnett said, on the way to suggesting that quite a bit of it could end up in bonds in 2024. “But investors first need a recession and Fed cuts if they’re going to ‘sell cash,'” he added.

{kind=link}

Read that in Sept the Treasury announced they would begin to buy back their treasury bonds when necessary to help market liquidity. This sounds like the beginning of YCC, or didn’t they used to call that QE? Seems like a big deal to me, but I’m not a sophisticated investor….

That would add money into the system and increase inflation; the thing they are trying to correct.