I was skeptical of the so-called “Wile E. Coyote” moment narrative for the US economy. “Was,” past tense. I’m tentatively on board with it now.

On innumerable occasions looking back 12 or so months, I suggested a “sudden stop” scenario was unlikely, mostly because firms were still having a lot of trouble sourcing workers, which suggested demand was still a semblance of robust.

The labor market is (famously) a lagging indicator, but the pace of hiring last year (and even into 2023) meant that positing a “cliff” scenario entailed suggesting businesses across America would go from hiring anybody who could successfully complete the “First Name” section of a job application to firing people, en masse, four weeks later. “Welcome aboard Jim, it’s great to have you! We’re going to introduce you to your co-workers now, and then you’ll need to go ahead and turn in your name tag.” “What? Why?” “Because you’re fired.”

With allowances for the possibility that hindsight may one day suggest recession roadsigns were hiding in plain sight earlier this year, there was virtually no chance of a sudden stop in Q1. Only recently have job gains moderated such that one might plausibly argue for a Looney Tunes gravity moment.

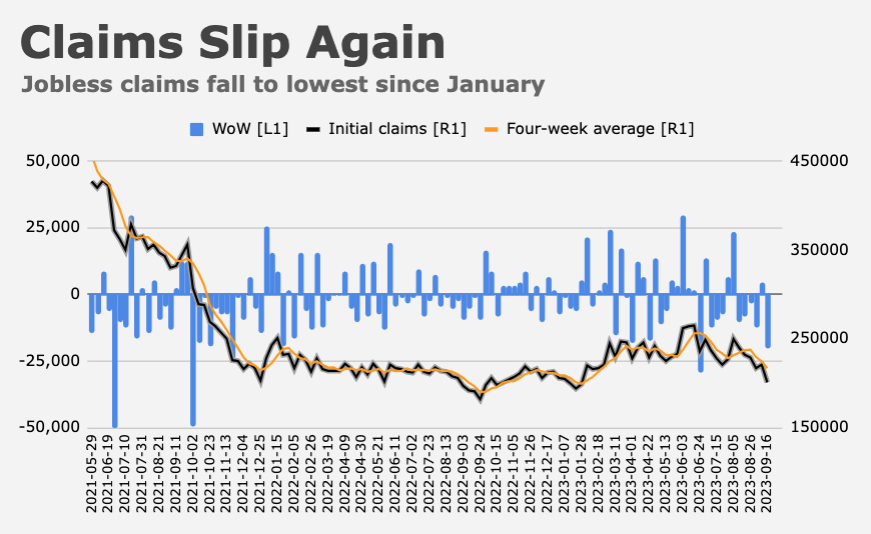

To be sure, the labor market still appears to be quite healthy. Indeed, initial jobless claims were the lowest since January last week. But the color from Friday’s preliminary S&P Global PMIs for September was telling, I think. Hiring was apparently vigorous, but it wasn’t difficult. There were “reports that staff retention was improving” and companies noted that “vacancies were filled with greater ease than had been seen in recent months.” Firms, S&P Global’s economists said, demonstrated “a greater ability to find suitable candidates for roles.”

Irrespective of what September’s jobs report tells us, and with allowances for the fact that job gains actually accelerated into July and August (revisions for the August NFP headline and the second revision for July’s might change that story, at least at the margins), it seems reasonable to suggest the labor market is more likely to cool going forward than heat back up. If, as the PMI anecdotes suggested, workers are more inclined to fill the millions of open positions tipped by the JOLTS report and less inclined to quit, that means they view the economic environment as more tenuous and may be more concerned about their own financial prospects as a result. And what are workers when they aren’t working? They’re consumers.

Maybe the deluge of labor market data that’ll inundate investors during the first full week of October will say otherwise, but my guess is that at some point over the next quarter or two, Jerome Powell’s “plane” is going to run into trouble. Maybe it’s birds, and he can Sully Sullenberger the economy onto the Hudson. A soft landing. Hopefully it’s not a midair “malfunction.” “Nice economy you got there. Shame if someone Yevgeny Prigozhin’d it.”

Bonds bears will tell you Treasurys aren’t priced for the macro and geopolitical regime shifts I spent the last year and a half obsessing over. Better late than never, I suppose. Bond bulls might counter that after grievous losses, bonds aren’t priced for a hard landing.

Earlier this week, the popular long-end ETF closed at the lowest in a dozen years. The drawdown from the “everything rally” peaks is now near 50%. If the economy goes into a tailspin, let alone crashes, there’s considerable scope for a rally, with the obvious caveat that bears could easily be correct. It’s possible that the market isn’t anywhere near done repricing the long-end of the US curve to account for higher deficits, more issuance, fewer buyers, Fed QT, perceived fiscal recklessness, a higher neutral rate, a larger term premium and on and on. But… well, that narrative is pretty consensus now.

Last week, I chuckled at BofA’s Michael Hartnett for his “respect the lags” remark. It sounded like just another nebulous recession warning from someone with a flair for the dramatic. To some extent anyway, that’s exactly what it was, but this week, he put some numbers to it. “Economic growth is not linear,” he said. “Average real GDP was 3% and nominal GDP 7% in the month prior to the start of the past 12 recessions since World War II.”

So, nobody rings a bell at the top. And the bottom can very well fall out without warning.

In the first half, the “surprise was ‘no recession,'” Hartnett went on. In the second half, the surprise is “higher-for-longer.” If “lower-for-longer” rates and yields “caused bubbles and booms in the 2010s and in 2020/21, ‘higher-for-longer’ means hard landing risks, bubble pops and busts in the first half of 2024,” Hartnett said.

At this point, I’m inclined to agree, in part because I suspect the “yields are destined to go higher” narrative is too ubiquitous for comfort.

{kind=link}

Higher for longer might indeed lead to a hard landing, at first solely an economic one with the expected decline in risk assets, but the real hard landing will occur if the economic recession arrives just in the middle of the presidential election cycle, helping Trump return to the WH. A hard landing leading to a calamity, where the yield on the 30 year bond sits at that juncture will be the least of our worries.

The gop is certainly planning to wreck the economy before the election.

So many variables to consider when trying to guess the future of the US economy. Here is yet another one to consider;

The WSJ published an article today titled, “Rebound in Immigration Comes to Economy’s Aid” which covered :

“the rise in foreign-born labor force boosts worker supply, eases wage pressure and aids Federal Reserve’s goal of ‘soft landing’”.

These two paragraphs got my attention (in a good sense – as our country desperately needs workers and, at the same time, we can help people who have the personal resolve to physically make it to our borders with the goal of working to improve their families lives).

“This year, average monthly growth in the foreign-born labor force is about 65,000 higher compared with 2022 on a seasonally adjusted basis, a Goldman Sachs analysis found. After plunging at the start of the pandemic, the size of the foreign-born labor force has rebounded, nearing 32 million people in August.”

“Foreign-born workers’ share of the labor force—those working or looking for work—reached 18% in 2022, the highest level on record going back to 1996, according to the Labor Department. It has climbed further this year to an average of 18.5% through August, not adjusted for seasonal variation.”

Congress needs to update legislation to provide a legal pathway for immigrants to live/work in the US.

WSJ only a month behind me on that GS piece: https://heisenbergreport.com/2023/08/28/the-us-labor-market-is-normalizing-thank-immigrants/

They’re getting faster!

I totally agree. Sadly, folks like the Great White Hope Ronnie DeSantis do not. Let’s see how those needed flows hold up if our GOP gets to follow through with proposals to order “shoot to kill” border enforcement as well as invading northern Mexico in the name of stemming drug flows. It would be very tempting for a Mexican government to retaliate by stopping their measures to reduce the flow of migrants from Central America or elsewhere.

Someone placed a large SOFR June/24′ call a year ago.