Is the thrill gone again for retail investors?

Maybe. And to the extent everyday market participants (as distinct from professionals, who, like economists paid to be wrong about the macro, extract enormous sums from clients in exchange for habitually underperforming low-cost index funds) are less enthusiastic about equities, they won’t be blamed. After all, last month was somewhat vexing.

A confluence of factors engendered turmoil in bonds, and that, in turn, undercut stocks. It worked out in the end. As the curtain closed on August, a bevy of top-tier data offered good news for the Fed’s inflation fight and two-year US yields tumbled accordingly. Stocks rose as September dawned.

But by then, it was too late for sentiment. Although individual investors’ mood improved slightly in the week to August 30, the A.I. / debt ceiling deal bump is gone. Not even another blockbuster report from Nvidia could save it.

Indeed, bullish sentiment was 16 points lower over the course of August on AAII’s gauge. The local peak was almost 20 points higher on July 19.

Note that the deterioration in sentiment (and also last week’s small uptick) was consistent with the trend in equity fund flows.

US equity-focused ETFs and mutual funds saw net outflows for three straight weeks last month, before taking in $4.5 billion in the week to August 30. Overall, US-focused funds shed a net $9.88 billion last month+.

The simple figures above from Deutsche Bank give you some long-term perspective on AAII sentiment, in case that’s in any way helpful.

“The US retail impulse into equities appears to have waned in August, after rising significantly in the previous two months,” JPMorgan’s Nikolaos Panigirtzoglou said, weighing in on the same dynamic.

He cited a number of indicators including small lot option flows. “After rising significantly in June and July, call option buying declined abruptly in August,” he remarked.

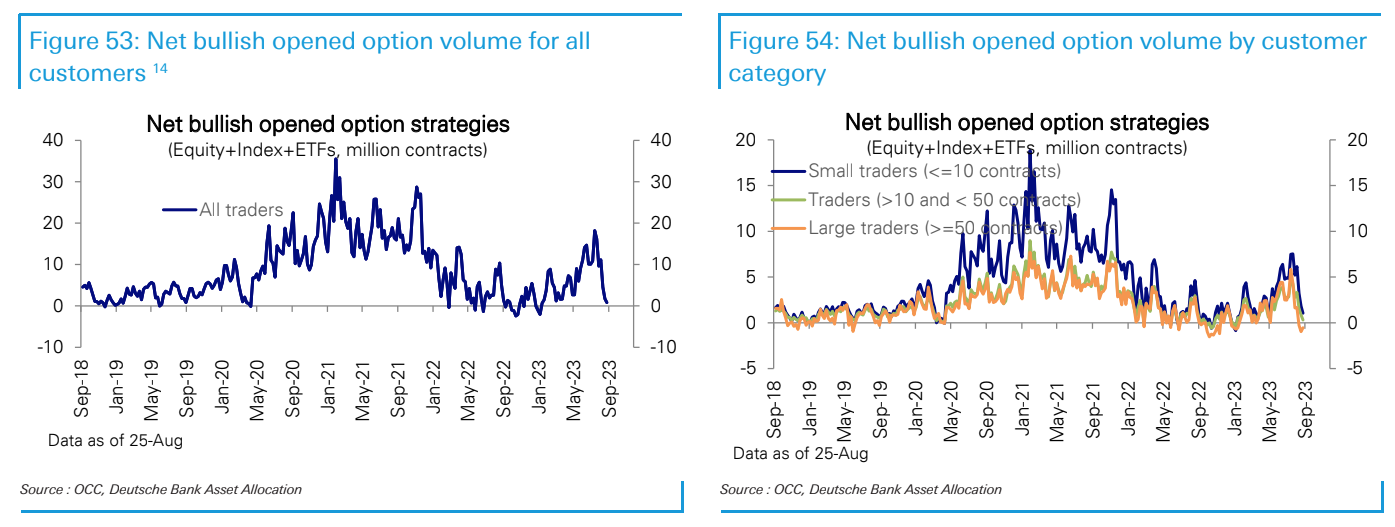

There are, of course, any number of ways to slice and dice options data. Frankly, you can tell just about any story you want to tell depending on how you go about presenting the numbers.

That said, looking simply at the difference between, on one hand, call-buying and put-selling (bullish expressions) and, on the other, put-buying and call-selling, you come away with the impression that “net bullishness” (if you will) has declined significantly. And it’s not confined to small traders.

It’d be fairly easy to suggest that sentiment among retail investors isn’t likely to get any better over the next few weeks. The September seasonal isn’t kind to stocks and a lot of younger investors (gamblers) are set to resume student loan payments next month.

If “stimmy” contributed to the surge in retail activity in 2020 and 2021 (which it unquestionably did), then it’s reasonable to ask if the end of the loan moratorium (the opposite of “stimmy”) might curtail such activity.

{kind=link}

Would be interesting to see these data sets divided into demographics..