Market interest in the July vintage of the Fed’s senior loan officer opinion survey was muted compared to the last installment.

That’s a high bar, though. April’s SLOOS (the survey should win an award for worst-sounding acronym) was the single-most anticipated in recent memory, as it reflected changes in credit standards and demand for bank loans during the period encompassing the worst financial sector turmoil since Lehman.

The results, released on May 8, were a bit anticlimactic. Lending standards tightened, but perhaps not as acutely as many feared. The more notable takeaway was a collapse in demand for loans.

Fast forward three months and the latest edition showed — drumroll — that standards remained tight, and demand weak. The net percentage tightening C&I standards to large and middle-market firms exceeded 50%.

If you don’t count COVID, that’s the highest since the beginning of 2009.

Banks tightened all queried loan terms on C&I loans, and likewise turned the screws on the maximum size and maturity of credit lines, loan covenants and collateralization requirements.

The tightening was broad-based across large and small banks, who all generally cited macro uncertainty, lower risk tolerance, deteriorating liquidity positions (that’s surely concentrated in smaller lenders), industry-specific problems and “increased concerns about the effects of legislative changes [and] supervisory actions.”

CRE standards remained very tight for obvious reasons, although it does look as though we might’ve reached “peak tight,” at least in terms of prevalence. The CRE apocalypse hasn’t played out in earnest just yet, but it’s a slow-motion train wreck. Parts of that thesis are a foregone conclusion, even if the fallout doesn’t ultimately result in any sort of panic.

As I’ve said previously, the CRE doomsday story is so well socialized by now that it’s difficult to imagine how it could become systemic. Everyone with even a passing interest in markets has probably read a half-dozen articles about it and listened to a podcast or three. It’s rare that well-socialized risks trigger crises.

I’m sure some readers would be inclined to play “gotcha” with me on that latter point — you might name a few well-known risks that did, in fact, manifest in acute bouts of turmoil historically. But you get the point: There isn’t a serious market participant in America who’s oblivious to the CRE story, let alone a bank CEO. All else equal, that mitigates the risk of a total disaster.

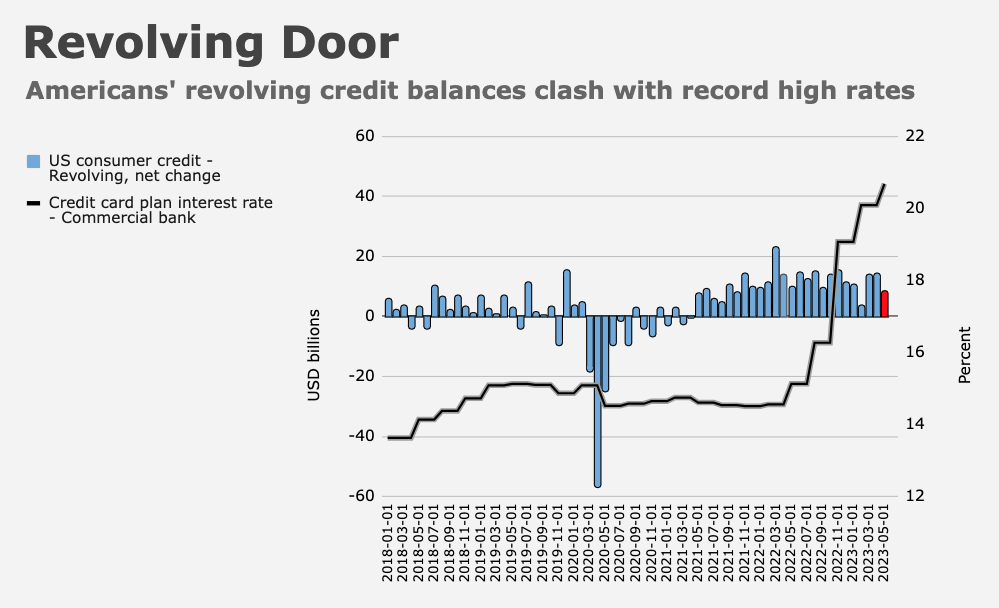

On the consumer side of the SLOOS, the picture was mixed. A bigger net share of banks tightened standards for credit cards, but a smaller share tightened standards for auto and other consumer loans.

Average card rates, you’re reminded, are perched at record highs. “Significant net shares of banks reported having tightened the extent to which loans are granted to some customers who do not meet credit scoring requirements, increasing the minimum required credit scores and decreasing credit limits,” Monday’s release said.

The extent of tightening in residential real estate and HELOC terms varied by loan type. Only a “moderate” share of banks reported tightening standards on GSE-eligible loans, for example.

Turning to demand, it was weak. As noted. It does appear to have bottomed, though. The net percentage of banks reporting stronger demand for various types of loans was less negative in this vintage of the survey than last. If you squint, you can see the bounce in the visual below.

“Significant net shares of both domestic and foreign banks reported that the number of inquiries from potential borrowers regarding the availability and terms of credit lines decreased,” the Fed said.

If anything, I’d suggest the survey showed the situation has stabilized, or even improved. Yes, the environment is challenging both for lenders and borrowers, but it looks like the net share of banks tightening standards for C&I and CRE loans maxed out last quarter, and demand may be rebounding slightly.

As far as I could tell, there were no immediate implications for markets. Not much got worse, and there were cautious signs of improvement throughout, even as the overarching message for lending remained rather dour.

“Although borrowing costs are relatively high, it isn’t the last 25bps rate hike that turns struggling businesses into failing businesses. It’s when a company has a couple of orders cancel on them and the business goes to its local bank and asks for a line of credit to see them through, but the bank says ‘No,'” ING’s James Knightley remarked. “We run a much higher risk of this happening when lending conditions are as tight as signaled by the SLOOS.”

Of course, that’s the sort of bad news that’s “good” for inflation, something Knightley was quick to point out. “This report makes it all the more likely that the Fed will not need to hike rates further since tighter lending conditions and reduced loan demand point to further credit contraction that will naturally take heat out of the economy,” he said.

Banks intend to further tighten standards on all loan categories in the back half of the year. They cited economic ambiguity and expectations for collateral deterioration. No one was surprised Monday to learn that lenders will likely retain a cautious bias for the remainder of 2023.

As Jerome Powell put it last week, in what now seems like a fittingly bland preview of the survey, “It’s broadly consistent with what you would expect.”

{kind=link}