I wouldn’t call this week’s US data docket inconsequential, but it’d certainly be fair to say there’s nothing due that’ll be decisive for the policy narrative as the Fed enters its pre-meeting quiet period.

If there’s a headliner, it’s retail sales, which probably rose 0.5% in June, economists suspect.

The update on nominal spending is germane, but absent a big surprise (in either direction) which isn’t tempered or otherwise “offset” by divergent reads on the underlying aggregates (i.e., ex-autos, control, etc.), the print will probably come and go with little in the way of fanfare.

That’s not to suggest it’s irrelevant. Far from it. The US economy is enjoying what looks like a “Goldilocks” moment. The labor market is softening around the edges, job vacancies are trending lower with no concurrent rise in the unemployment rate, job cuts are abating, inflation is cooling, wholesale prices are on the brink of deflation, a resilient services sector still suggests the economy’s growth driver is intact and a dearth of resale housing inventory suggests demand for new construction will be robust even in the face of 7% mortgage rates (and record-high mortgage payments+).

It’s a delicate balance. Some would call it unstable. At the end of the day, the world’s largest economy lives and dies by consumption, so the fresh read on nominal spending will help policymakers and market participants confirm (or not) their suspicions that the US is nowhere near succumbing to any kind of recession.

The figures are, of course, for June, the last month of Q2. We know consumers were feeling pretty good about things in early July. As of the last refresh, the Atlanta Fed’s GDPNow tracker for the second quarter stood at 2.3%.

In addition to the spending figures, housing updates including builder sentiment for July as well as new construction figures and existing home sales for June are due.

As noted above, the shortage of resale properties is herding Americans into new construction. That pushed up builder sentiment and bolstered shares of homebuilders during the first half. The NAHB gauge is seen posting a seventh straight increase in July, existing home sales probably fell again in June and housing starts likely dropped nearly 10% last month.

Recall that starts surged nearly 22% in May. New single-family construction jumped 19%, nearly reclaiming the one million SAAR mark for the first time since prices peaked early last summer.

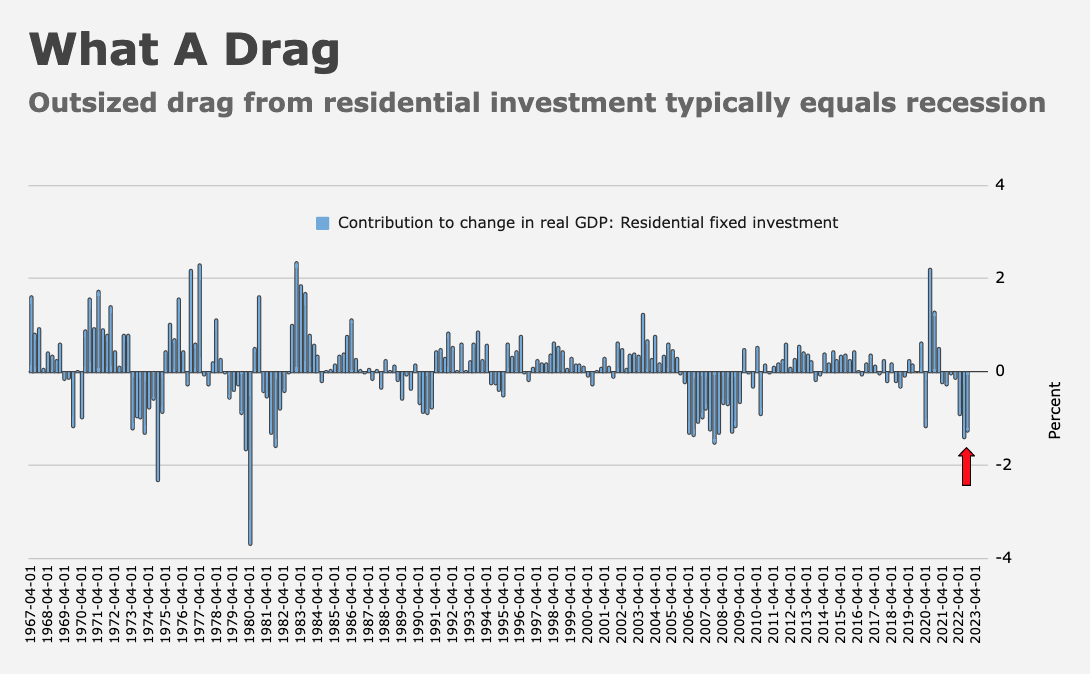

Residential investment was a drag on US GDP for seven consecutive quarters, a streak which, in the past, might’ve accompanied a broader economic downturn. Flying hammers are a sight for sore eyes in that context.

Also on deck in the US: The Empire and Philly Fed surveys, IP and Cap U and, of course, weekly claims.

Elsewhere, market participants will cringe at an update on UK CPI. The UK is, without exaggeration, mired in a full-on inflation crisis and unlike its developed market peers, the country is seeing little in the way of relief.

The last CPI report was a disaster, and pay growth figures plainly show inflation is embedded in wage-setting.

The BoE may raise rates by another 50bps next month (~43bps priced with another ~35bps priced for September). Terminal pricing is north of 6%.

Finally, activity data and Q2 GDP are due out of Beijing. The GDP figures will be distorted, so markets will focus on industrial output and retail sales figures for June, which may well suggest the world’s second-largest economy continues to struggle.

{kind=link}

See? What I just said. Confusion to all.