One impetus for this year’s equity gains is obviously falling headline inflation, and not just in the US.

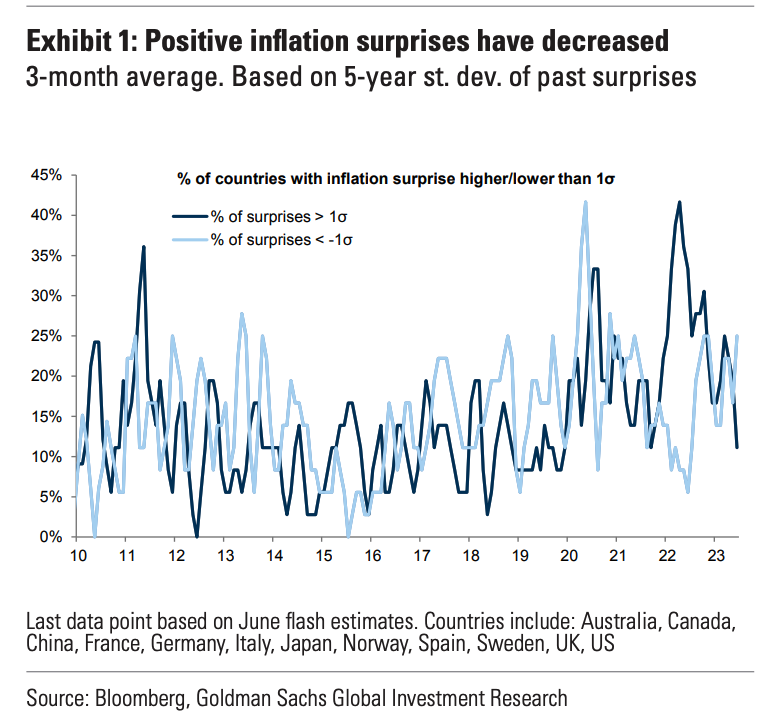

Core inflation remains vexing across locales, but upside inflation surprises have receded and headline prints convey a message of hope. False hope, perhaps.

On hot data days, one can’t help but suspect that inflation progress, even on the headline numbers, is tenuous. Services sector activity is too robust and labor markets too tight for comfort. Housing might’ve troughed, and if commodities were to find their footing… well, suffice to say it wouldn’t be terribly surprising to see headline CPI inflect for the worse again, particularly where base effects are less of a help moving into the back half of the year.

“On current monthly [US] CPI trends, the June print will be the trough for 2023 and H2 sees a rise back to 4% unless monthly prints gap lower to <0.2% very soon,” BofA’s Michael Hartnett cautioned, in his latest.

The updated (and familiar) figure on the left above shows you how easily this could begin to go wrong. There’s not a lot of margin for error on the monthly readings when it comes to keeping the YoY headline CPI prints below 4%. And core has shown little, if any, inclination to cool, although we’re told to expect a more favorable trend in underlying price growth very soon as shelter disinflation begins to show up on a lag.

Hartnett added what he called “an important side note.” I’ve been over the “bad side” of falling inflation on too many occasions to count: As price growth cools, pricing power wanes and absent a drop in costs, margins shrink. There’s a very strong relationship between YoY PPI and YoY EPS growth. “Inflation has been positive for EPS,” Hartnett remarked. “[That’s] why the Q1 EPS recession call was so off — over the past 18 months US core CPI was up 9%, S&P 500 EPS up 12.5% thus real EPS growth +3-4% since January of 2022,” he went on, referencing the figure on the right above.

Of course, that relationship is unlikely to be “efficient” in the event inflation were to turn higher again. That is: An inflection in headline CPI wouldn’t be a real-time cure-all for margin erosion, particularly not if there’s any truth to the idea that pandemic savings buffers are finally close to being exhausted.

The good news is that the ratio of new orders to inventories in the ISM manufacturing survey suggests the headline ISM prints could turn up soon after eight months (and counting) in contraction, but Hartnett gently noted that semis, industrials and homebuilders “have discounted the outcome” and as such look “very vulnerable” if the ISM leading indicator is a headfake.

He also warned on a new rates shock. The yield on a Bloomberg index of global government bonds hit a 15-year high this week, as US 10s were back above 4% following Thursday’s run of hot macro data. On Friday, in the hours ahead of the June jobs report in the US, yields Down Under were the highest in a decade.

Hartnett pointed to liquidity. “Central banks have drained $170 billion in liquidity over the past two weeks,” he said, noting that BofA expects another $1 trillion in Q3. “That’s why bond yields are up.”

The bank also sees financial conditions tightening from here driven by “inflation, deficits and strong labor market data.” The “higher-for-longer/hard landing” view is “entrenched,” Hartnett said.

{kind=link}

I every time I read another of your posts I appreciate you and the other smart folks you integrate in these pieces. Just terrific stuff.