While previewing this week’s data void in the US, I jokingly noted that traders concerned about boredom amid a dearth of top-tier releases from the world’s largest economy could look forward to pulse-pounding policy decisions from the Bank of Canada and the RBA.

Although I long ago gave up on the idea I could leverage my penmanship in the service of convincing readers to care about monetary policy not involving the Big 4 central banks, I’d be completely remiss not to mention Tuesday’s RBA hike.

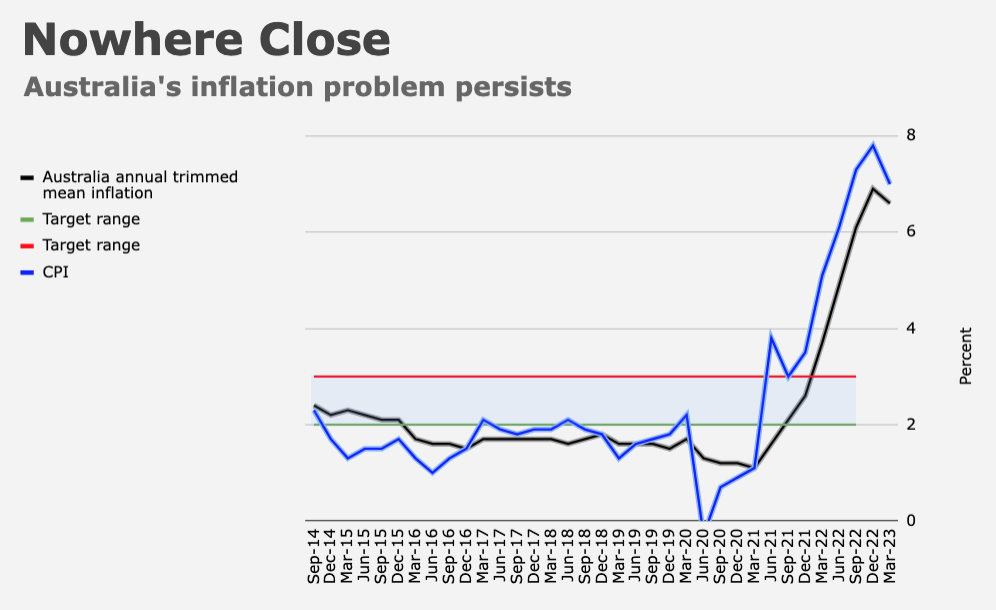

There’s a lot going on at the RBA, where policymakers have been scrutinized for a range of alleged shortcomings, including 2021’s embarrassing retreat from a short-lived experiment in yield-curve control and Philip Lowe’s less-than-stellar communications track record around the bank’s forward guidance. Right up until the onset of rate hikes, Lowe was reluctant to countenance the idea of any tightening last year. For a time, he insisted rates would stay at rock-bottom levels until 2024.

Although he wasn’t alone among central bankers in denying the reality of inflation, he was pretty adamant. And he held onto the dovish rhetoric for what certainly seemed like an inordinate amount of time even in the context of policymakers who were almost universally behind the curve. An independent review of the bank’s operating procedures commissioned by the government recommended a hodgepodge of changes, which Lowe suggested will “strengthen the bank’s governance and decision-making processes.”

In any event, Tuesday’s 25bps move was the second consecutive. Last month’s hike came after Lowe skipped a meeting in April. The RBA’s pause was an example of why some continue to view Lowe’s messaging as lamentably clumsy. It’s worth a brief trip down memory lane.

In December, in the color accompanying the bank’s eighth hike of the cycle, Lowe included language that the RBA wasn’t on a “pre-set course,” a nod to optionality. That language vanished from the February statement, only to be effectively reinstated a month later in the service of tipping April’s pause.

So, in just three meetings (the RBA didn’t hold a policy meeting in January), the bank went from dovish hike to hawkish hike to hike with intent to pause. We’re now two meetings on from that pause and the RBA has hiked two additional times.

As I put it in March, the RBA’s tightening campaign continues to be a confusing, messy affair, with allowances for the unprecedented nature of the circumstances.

Australian households are among the most indebted in the world and rate hikes have obviously pressured the nation’s notoriously frothy housing market. Lowe, for all the derision, is toeing a very precarious line. Inflation is still far too high, wage increases aren’t being offset by productivity gains and, worryingly, home prices are rising again. And yet, every incremental rate hike increases the risk of a catastrophic hard landing tied to the nation’s household debt burden.

“Housing prices are rising again and some households have substantial savings buffers, although others are experiencing a painful squeeze on their finances,” Lowe remarked, in the new statement.

The forward guidance was characteristically ambiguous. “Some further tightening may be required, but that will depend upon how the economy and inflation evolve,” Lowe said. Ominously, the phrase “well anchored” was removed.

For central bank watchers, it’s impossible (or very difficult) to separate the mini-soap opera that is the RBA’s quest to recapture lost credibility from the broader tale of central banks confronting an inflation impulse unseen in decades. But for casual observers, the important point is this: If the Fed does indeed pause at the June FOMC, no one should assume that’s the end of the hiking cycle. The RBA’s experience shows how a “pause” can be just that — a pause.

{kind=link}