On Friday, Michael Barr released the Fed’s internal review of its supervision and regulation of Silicon Valley Bank which, as you might’ve heard, failed recently.

His findings weren’t flattering. For anyone.

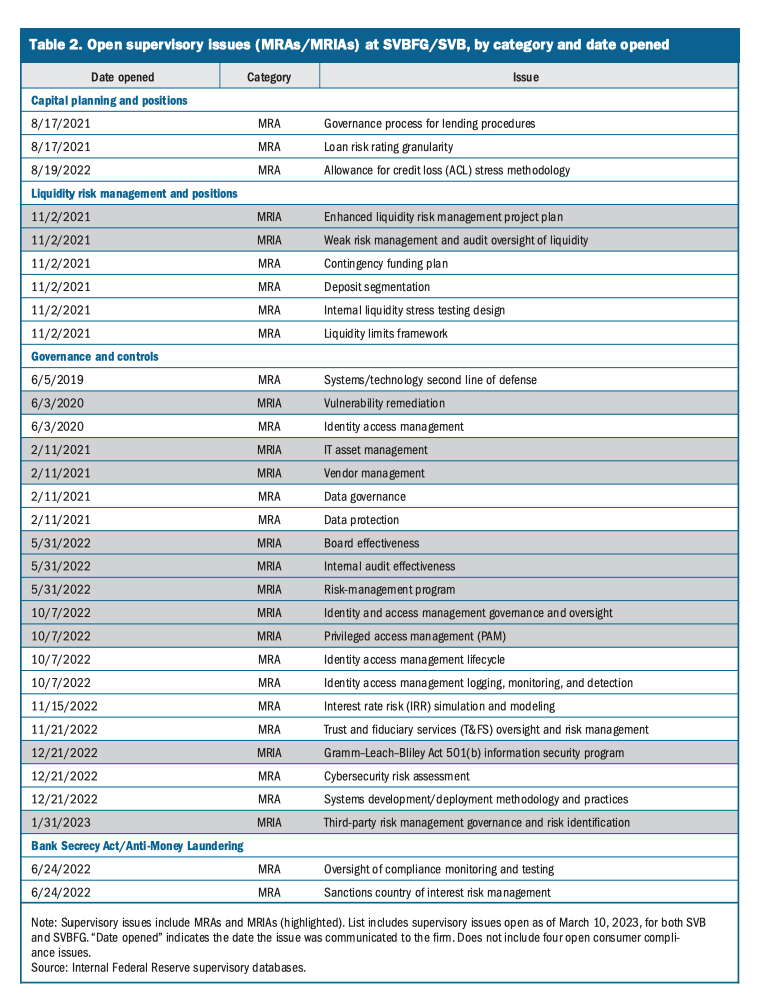

Although Barr reiterated his criticism of bank management, he also said supervisors didn’t do enough to ensure SVB fixed myriad problems flagged in the lead-up to the lender’s spectacular implosion in March. The Fed board, he suggested, promoted a less assertive supervisory approach, and its shift in stance served to impede supervision. SVB had 31 outstanding warnings, triple the average for its peers.

In the days leading up to the Friday release of Barr’s review, media reports suggested the Fed, swaying with shifting political winds, took a hands-off approach to the supervision of some small and midsized lenders on the (sometimes tacit, sometimes explicit) assumption they couldn’t pose a systemic risk. That assumption proved erroneous. When SVB blew up last month, Jerome Powell was compelled to vote with Janet Yellen to use a systemic risk exception to shield SVB’s uninsured depositors in the interest of preventing contagion to the wider banking sector.

Earlier this week, Bloomberg cited multiple sources who said the Fed’s “supervisory culture” led to “a shift in how some institutions were supervised on the ground.” Specifically, regional Fed bank examiners apparently faced skepticism when they were judged to be spending an inordinate amount of time on small lenders assumed to pose no risk to the system. The bar, Bloomberg wrote, “was raised for escalating concerns via formal supervisory actions [and] attempts by regional staff to flag novel kinds of risk… didn’t result in supervisory direction from the Washington board.” Barr effectively confirmed that reporting on Friday.

Again, it’s important to note that the shift came amid a concurrent change in attitudes on Capitol Hill and at the White House. As detailed here last month, the SVB fiasco was aided and abetted by poor policy, starting with legislation. To briefly recapitulate, the Economic Growth, Regulatory Relief and Consumer Protection Act of 2018 unshackled mid-sized lenders by “exempt[ing] some small and regional banks from the most stringent [Dodd-Frank] regulations,” as The Washington Post explained at the time. The following year, the Fed and the FDIC permitted some banks to avail themselves of an exemption to a rule that mandated the inclusion of unrealized gains and losses in regulatory capital.

Barr mentioned the Economic Growth, Regulatory Relief and Consumer Protection Act frequently in Friday’s review, which he described as “a self-assessment that takes an unflinching look at the conditions that led to [SVB’s] failure, including the role of Federal Reserve supervision and regulation.”

Crucially, he noted that in July of 2018, the Board “raised the threshold for heightened supervision by the large and foreign banking organizations portfolio from $50 billion to $100 billion” in light of new thresholds from the legislation. That, he said, “delayed application of heightened supervisory expectations to [SVB] by at least three years.”

“According to interviews, one reason supervisors did not increase supervisory intensity as [SVB] grew toward the $100 billion threshold is that there was concern from policymakers and senior leadership at the Board that supervisors would ‘pull forward'” enhanced prudential standards to which the largest institutions are subject prior to the bank actually meeting the threshold, Barr detailed.

He went on to note that the Board of Governors’ implementation of the legislation “created stark differences” between supervisory frameworks for regional banking organizations and large and foreign banking organizations, which SVB became in early 2021. Those differences “constrained the ability to prepare a firm for the transition between the two portfolios,” Barr explained, adding that “the accommodative supervisory stance and examination pause during COVID-19 amplified the impact of the transition, resulting in the cancellation of examinations during a period of rapid growth” for the bank.

On page 35 (49 pages into the actual document), Barr detailed the transition process. In short: It was piecemeal. It “lacked a defined plan and process,” as Barr put it.

As SVB crossed the $100 billion threshold, regional banking staff at the San Francisco Fed hadn’t yet completed their annual ratings cycle. A transition period was agreed, during which the regional banking organization staff would complete their review while the new large and foreign banking organization team was being formed. Nobody involved was truly prepared for the transition, or at least that’s what is sounds like. Barr, citing Fed staff, described a “cliff effect.”

He was very explicit about the extent to which there was indeed a change in the supervisory culture. In one particularly illuminating passage, he wrote that,

Over the same period, under the direction of the Vice Chair for Supervision, supervisory practices shifted. In the interviews for this report, staff repeatedly mentioned changes in expectations and practices, including pressure to reduce burden on firms, meet a higher burden of proof for a supervisory conclusion, and demonstrate due process when considering supervisory actions. There was no formal or specific policy that required this, but staff felt a shift in culture and expectations from internal discussions and observed behavior that changed how supervision was executed. As a result, staff approached supervisory messages, particularly supervisory findings and enforcement actions, with a need to accumulate more evidence than in the past, which contributed to delays and, in some cases, led staff not to take action.

Although Barr didn’t quite put it this way, the bottom line is that the Economic Growth, Regulatory Relief and Consumer Protection Act, and a subsequent behavioral shift at the Fed, absolutely played a key role in this debacle, and anyone who says different (including and especially politicians, lawmakers and Fed officials, former or current) is obfuscating, at best.

“In absence of EGRRCPA, the 2019 tailoring rule and related rulemakings [SVB] would have been subject to additional liquidity risk management, ILST and standardized liquidity requirements,” as well as the full LCR requirement and the full NSFR requirement, Barr said, on pages 87 and 88, noting that SVB “would not have met the full LCR requirement over the time periods shown” and had it been subject to the LCR, “may have adopted more proactive monitoring or managing of its liquidity position and mix of liquid assets.”

His conclusion was that legislation, the Fed tailoring rule and other, related, policy decisions, “combined to create a weaker regulatory framework for a firm like SVB.”

Moreover, the Fed just wasn’t agile enough, and didn’t comprehend the unique risks associated with the bank’s model. “Supervisors recognized a gradual increase in liquidity and market risks, but they did not fully appreciate the risks associated with the concentrated deposit base or [SVB’s] investment portfolio strategy,” Barr said. Both on the liquidity and market side, Barr repeatedly emphasized that Fed supervisors “identified some but not all” of the risks.

As for SVB itself, I think it’s fair to assess that most market observers agree the bank didn’t adequately manage rate risk, and most of what Barr “uncovered” about management failures wasn’t new. He did say that “the incentive compensation arrangements and practices” at SVB “encouraged excessive risk taking to maximize short-term financial metrics.”

He summarized his 118-page tome in four bullet points:

- Silicon Valley Bank’s board of directors and management failed to manage their risks.

- Supervisors did not fully appreciate the extent of the vulnerabilities as Silicon Valley Bank grew in size and complexity.

- When supervisors did identify vulnerabilities, they did not take sufficient steps to ensure that Silicon Valley Bank fixed those problems quickly enough.

- The Board’s tailoring approach in response to the Economic Growth, Regulatory Relief, and Consumer Protection Act and a shift in the stance of supervisory policy impeded effective supervision by reducing standards, increasing complexity and promoting a less assertive supervisory approach.

Barr also emphasized the role that social media and digital banking play in raising the risk of runs, something I discussed earlier this week. “The combination of social media, a highly networked and concentrated depositor base and technology may have fundamentally changed the speed of bank runs,” he warned. “Social media enabled depositors to instantly spread concerns about a bank run, and technology enabled immediate withdrawals of funding.”

The review made a number of suggestions for prospective bank rule changes, including, but not necessarily limited to, additional capital or liquidity requirements for firms “with inadequate capital planning, liquidity risk management, or governance and controls”; modifications to the tailoring framework, including a re-evaluation of rules for banks with $100 billion or more in assets; new supervision and regulation of bank protocols for managing rate, liquidity and uninsured deposit risks; and requirements for more firms to account for unrealized losses on AFS books. Any changes “would not be effective for several years because of the standard notice and comment rulemaking process and would be accompanied by an appropriate phase-in,” Barr remarked.

You can peruse the full document for yourself below, but I think one passage, found on page 97 (page 111 if you’re using the full document) is both exceptionally apt and broadly applicable.

“The supervisory record on SVB shows a focus on consensus-building and a perceived need to form ironclad assessments about what had already gone wrong and less on judgments with a more open mind about what could go wrong,” Barr said (emphasis mine), adding that,

This hesitancy to move decisively is particularly difficult to overcome during periods of strong economic growth and business performance. To complement the more structured stress testing program, supervisors could also engage in narrative-based “pre-mortem” exercises or reverse stress testing to think critically about idiosyncratic scenarios and tail events.

Words to live by. Hopefully, Powell and other senior Fed officials made it 100 pages in to read that passage, because it could also apply to monetary policymaking, and perhaps lead to better outcomes if considered.

“I welcome this thorough and self-critical report on Federal Reserve supervision from Vice Chair Barr,” Powell said Friday. “I agree with and support his recommendations to address our rules and supervisory practices, and I am confident they will lead to a stronger and more resilient banking system.”

{kind=link}

Thanks much for including this document. Very enlightening. For more than 20 years I helped several banks create strategic plans that could be used to guide their actions and to meet the demands of regulators. One observation I would make is that bank regulation is an expensive and onerous process (for the banks, many people needed for many weeks) and for smaller institutions in complex markets, the more of a struggle it can be. The biggest bank I worked with had two billion in assets and annually faced a regular financial audit by its public accountant, an annual audit from the COC, and a Fed checkup, at the least. These guys, and their auditors get tired of all this and while I won’t say these folks get sloppy, they can get somewhat numb to critical risk factors. I dealt with dozens of these things over the years and I can’t even begin to understand what it must be like for JPM, and other large banks.

I don’t generally mess with individual banks in my investments, but I clearly recall at least a couple regionals that were sitting just below the old $50 billion threshold and doing everything they could not to grow their assets or deposit bases to stay below that threshold, sacrificing then-current performance to do so, as they eagerly awaited for the threshold to be raised. I understood the implications, but frankly was a little surprised (and turned off) that the increased regulatory burdens were considered THAT onerous that the better approach was to hunker down and hope for legislative relief even if that meant years of waiting.