Jeff Gundlach says a recession may be right around the corner.

That isn’t news. If I had a nickel for every time Jeff Gundlach said something bad was about to happen to the economy, markets or both, I’d be Jeff Gundlach.

A couple of days after telling a few hundred thousand social media followers that Fed cuts were likely at some point in the relatively near future, Gundlach told his friends at CNBC that “headwinds are building.” “I think the recession is here in a few months,” he said, suggesting the Fed may cut rates a couple of times in 2023.

Markets obviously agree, or at least about the likelihood of rate cuts. Plainly, and as discussed here ad nauseam, the odds of recession have increased following recent tumult in the banking system.

More narrowly, it’s worth noting that small-caps are sending a potentially ominous signal. The recent blast of underperformance that accompanied the banking crisis sticks out as acute.

“The equity market has not ignored this new incremental risk,” Morgan Stanley’s Mike Wilson said, of stocks’ ostensible resilience in the face of disconcerting headlines out of the banking sector. “The market has re-priced internally.”

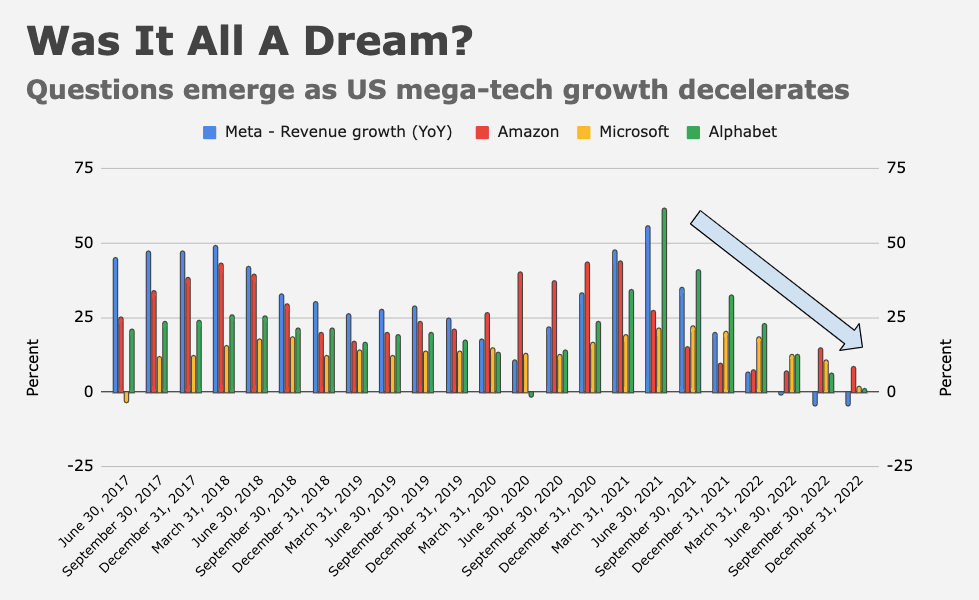

Of course, part of what you’re seeing in small-cap underperformance is the tech heavyweights. Once again, markets appear to be assigning a safety premium to America’s favorite mega-caps, despite a dramatic slowdown in top-line growth which (belatedly) validated some critics’ contention that the world’s best-known “growth” stocks are actually cyclicals.

If you ask Wilson, assuming tech is a haven could be a mistake. “Breadth has been exceptionally weak as large-cap growth stocks hold up the major averages, suggest[ing] the S&P 500 and NDX are unlikely to hold up under this classic migration to higher ground if a flood arrives,” he wrote, before reiterating his “long-standing view that technology companies are pro-cyclical and not as defensive as perhaps many market participants believe.”

Whatever the case, the underperformance from small-caps doesn’t look especially fortuitous. The figure above is simple, but perhaps instructive.

Wilson continues to caution investors that the bottom can fall out abruptly. “Be aware that the market can price [growth] concerns quickly even before company guidance is lowered,” he warned. “Just like the bond market, the equity market may reprice rapidly and without warning.”

Coming back to Gundlach, asked by CNBC’s Scott Wapner if he (Gundlach) disagrees with Christine Lagarde’s contention that central banks can fight inflation and guard against financial stability risks simultaneously, Gundlach said, “You can’t have it both ways. You can’t have your cake and eat it too.”

{kind=link}

Gundlach is entertaining, but I do not pay much attention to his market calls. That said, tighter C&I loan standards cannot be overlooked. Considering the trauma banks are experiencing, it seems likely that C&I loan tightening will only continue in the months ahead, which probably feeds into a hardish landing at some point. I don’t know if it occurs in 2H23 or bleeds into Q124. All I know is markets appear to be range-bound for the foreseeable future.

Every 3-4 months or so my conviction that markets may finally capitulate, after a year or so plus of orderliness, gets triggered and heightened, only for more orderliness to result…now mix in nontrivial new banking and lending stressors, another FOMC hike, looming debt limit standoff, persistent inflation, +++, … it sure seems like something’s gonna give over next 6 months or so…

Looking at the date of the initial yield curve inversion and the peak inversion, relative to the ensuing recession, suggests that peak inversion – which we may have just seen – can still be as much as 2-3 qtrs ahead of the NBER-designated recession start.

Nowcast GDP for 1Q is above 3%. It is difficult for me to imagine GDP going negative before mid year. Maybe I should be more imaginative.

But the market doesn’t need the recession to formally start to price it in.