“The risk of a credit crunch has increased materially, in our view,” Morgan Stanley’s Mike Wilson said Monday, in a note called “This Is Not QE.”

As discussed on several occasions here last week, the sharp increase in the Fed’s balance sheet was predictable. We knew banks needed liquidity and FHLB issuance to meet demand from lenders in their region was a good leading indicator for how acute those needs were.

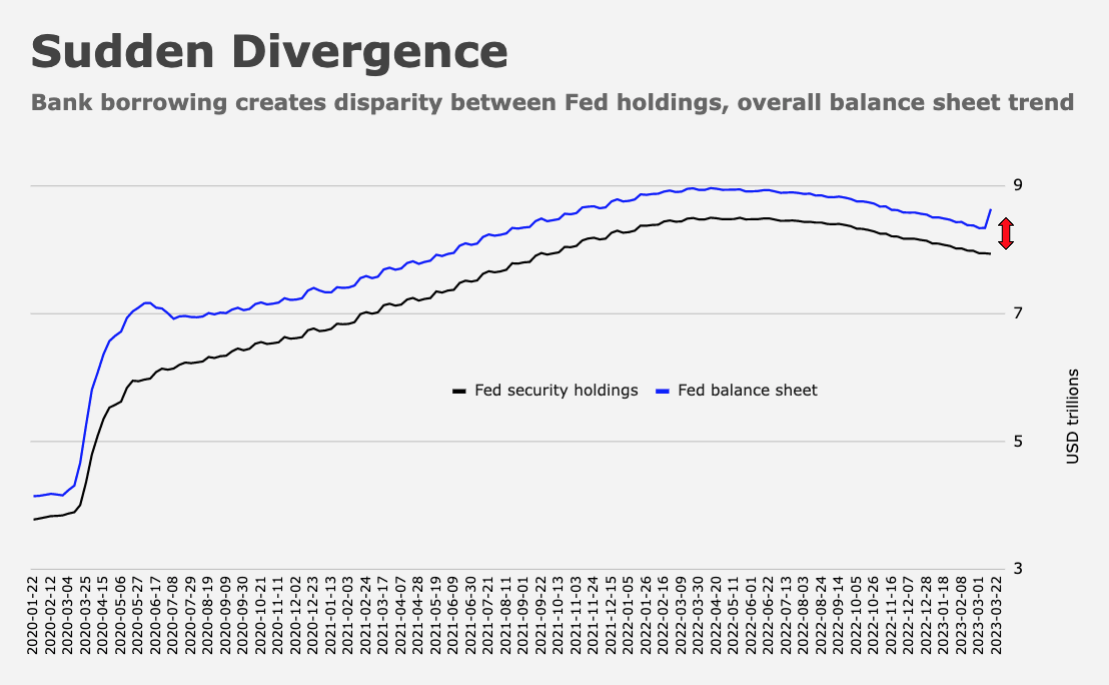

The scope of the discount window borrowing made a great chart, but there were bank runs going on, so it wasn’t “surprising,” per se. And the rest of the increase was attributable to the bridge banks for SVB and Signature.

So, as Wilson said, it’s not QE. The trend in the Fed’s securities portfolio remains lower, even as the overall balance sheet inflected dramatically higher (and on a near 90-degree angle).

Wilson pointed to yet another divergence between stocks and bonds. The latter are plainly saying something about a hard landing, what with short-end yields having plummeted ~120bps from the highs and the 2s10s having aggressively re-steepened, an even more ominous harbinger than the original inversions.

As I put it in the weekly+, “If we’re supposed to ‘fear the re-steepening’ as opposed to the original inversion, everyone should be terrified.”

“An inversion of the curve typically signals a recession within 12 months, but the real risk starts when it re-steepens from the trough, especially in cycles that exhibit high inflation where the Fed’s hands are tied — i.e., ’70s / ’80s,” Wilson wrote Monday.

The macro issue is credit contraction. 2023 may be “the year of the recession-causing credit crunch,” as I put it late last week+. Some of the discount window borrowing will surely migrate to the Fed’s new bank term lending facility, in which case it’s possible the Fed will succeed in supporting participating banks’ lending to the real economy. But, as Wilson pointed out, discount window borrowing in itself can be ephemeral, and may not help when it comes to new credit creation for consumers and businesses. It’s emergency lending, after all, and it comes with a stigma.

“None of these reserves will likely transmit to the economy as bank deposits normally do,” Wilson warned, before suggesting that “the overall velocity of money in the banking system is likely to fall sharply and more than offset any increase in reserves, especially given the temporary/emergency nature of these funds.”

This all comes back to the same overarching concern: Most of the nation’s banks are staring down a profitability crisis, and that assumes they make it through alive, which isn’t guaranteed. Lending will be curtailed going forward, and what credit does get created will be extended based on much stricter criterion. Absent a full FDIC backstop for smaller banks, their cost of capital will rise, crimping profitability, in a very non-virtuous loop.

What does this mean for the broader equity market? Well, if you ask Wilson, the prospect of decreased credit availability “for a wide swath of the economy” could very well be the “catalyst that finally convinces market participants that earnings estimates are too high.” That, in turn, is “another way of saying the equity risk premium is way too low.”

Of course, Wilson has been making this case for quite some time, but his warnings grew more urgent a few weeks ago, when the ERP effectively plumbed record lows in what he dubbed “the death zone.”

The good news is that if the reckoning is finally here, a buying opportunity may be just around the corner. “The S&P 500 ERP is currently 230bps [and] given the risk to the earnings outlook, the risk/reward in US equities remains unattractive until the ERP is at least 350-400bps, in our view,” Wilson wrote.

He assumes 10-year US yields can fall “a bit” more considering macro headwinds, but ultimately, the reset in the ERP Wilson expects would equate to a P/E multiple of 14-15x for the S&P.

“We think this is exactly how bear markets end — an unforeseen catalyst that is obvious in hindsight forces market participants to acknowledge what has been right in front of them the entire time,” he wrote, summing up. “In this case, it’s the fact that earnings growth expectations are much too high given the headwinds companies are facing, and the fact that the Fed is hiking rates during a period of contracting earnings.”

{kind=link}

I’m a little bit confused here. Back in the 1970s and early 80s when inflation was high, rates were high and Volcker pushed short rates to 18% your chart showing bank liabilities and M2 levels seems much flatter than the readings for the current period. What’s the difference?

So Wilson seems to be saying that the market will splat, and that will be a buying opportunity. I’d prefer he focus on getting the first leg of the trade right, before he wakes up in CandyLand.

Wilson was right at virtually every juncture for two straight years.

The bank crisis seems to have overshadowed the debt ceiling “negotiations” and I wonder if concerns about federal default are playing some role in the current liquidity and confidence “crisis.” Of course, the declining value of bonds due to rising interest rates seems sufficient to me to cause a crisis.

One more little wrinkle courtesy of your GOP:

https://finance.yahoo.com/news/us-lawmaker-divisions-over-fdic-174800404.html