Not surprisingly, US mortgage rates dropped over the last week alongside falling US yields.

The 13bps decline wasn’t especially pronounced, but it was notable for being the first drop in six weeks.

After receding sharply from last year’s highs, financing costs rose anew as a string of hot US economic data (ironically including housing figures) compelled traders to reassess the adequacy of Fed terminal rate expectations as they stood prior to January’s blistering payrolls report.

Bets on higher peak rates crescendoed during Jerome Powell’s congressional testimony, then unwound in dramatic fashion in the wake of last week’s bank failures. The dovish repricing helped push mortgage rates lower.

At 6.6%, you could argue rates are still prohibitively high, but I do think there’s something to the notion that would-be homebuyers with the wherewithal to accept the situation are resigned to it.

That is, yes the combination of elevated prices and financing costs has absolutely put homeownership out of reach for countless American families, but for those still in the market, fatalism might’ve set in. We aren’t going back to a two-handle 30-year fixed, and a three-handle might be a stretch too.

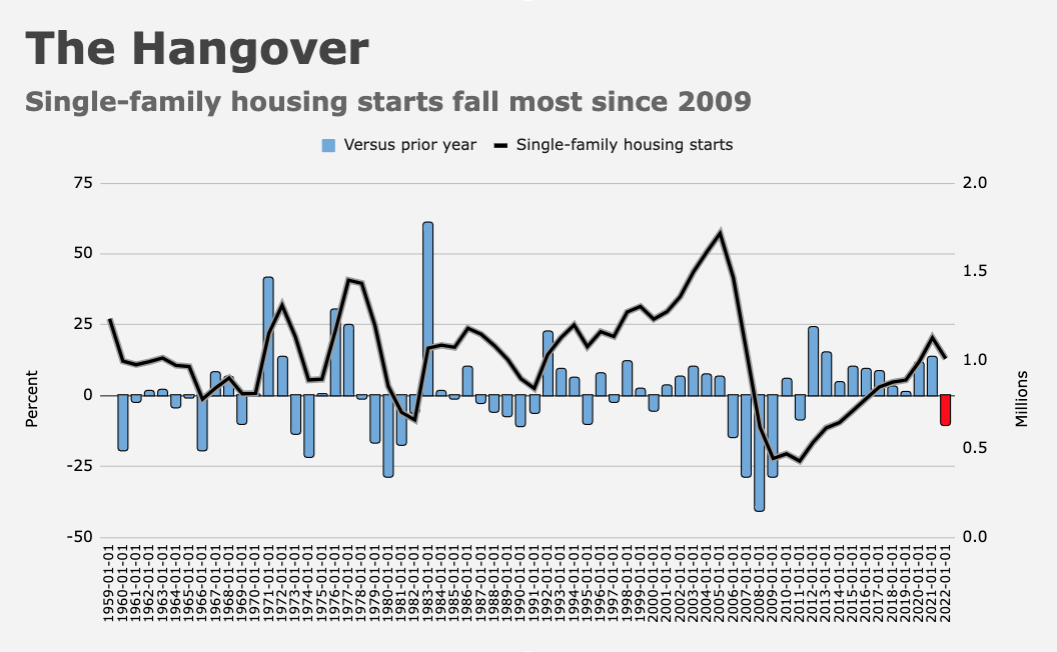

Earlier Thursday, government data showed housing starts rose at a 1.45 million annual rate in February, far above the highest estimate from five-dozen economists. The range was 1.25 million to 1.367 million.

The near 10% MoM jump was the largest since March of 2021, and the first increase since August.

As a reminder that no one needs, starts fell in 2022 for the first time since 2009.

Multifamily construction surged 24% from January, while single-family starts rose a modest 1.1%.

Notably, single-family permits posted their first increase in a year. If you exclude the pandemic volatility in 2020, the 7.6% increase was the largest since September of 2012.

Overall, permits rose to a 1.524 million annual rate, ahead of every estimate.

This all comes at a time when builder sentiment is recovering from a historic slump in 2022. The NAHB’s gauge rose a third month in March, even as an index of forward-looking single-family buyer sentiment ticked lower from February.

“Even as builders continue to deal with stubbornly high construction costs and material supply chain disruptions, they continue to report strong pent-up demand as buyers are waiting for interest rates to drop and turning more to the new home market due to a shortage of existing inventory,” NAHB Chair Alicia Huey said this week.

The rebound in builder sentiment likely means starts have bottomed. However, it’s possible that regional and community bank stress could impact the market.

Commenting Thursday on the starts data, Huey described the uptick in single-family activity as “anemic.” She cited “tightening credit conditions that threaten to be exacerbated by recent turmoil in the banking system.”

Earlier this week, Lennar’s guidance came in ahead of the Street for FYQ2 and the builder raised its full year outlook. Q1 results easily topped estimates. Asked on the company’s call about the outsized role regional banks play in financing the industry beyond large, publicly-traded builders, Executive Chairman Stuart Miller essentially said there’s no visibility.

“We’ve seen over just the past few days [that] the unexpected has happened,” Miller told Alan Ratner, from Zelman & Associates. “There are these things out there that are going to have some ripple effects, and we’ll all just have to sit and see how we deal with them.”

Indeed. I couldn’t have said it better myself.

The NAHB called the outlook tenuous in light of recent events. “Given instability concerns in the banking system and volatility in interest rates, builders are highly uncertain about the near- and medium-term outlook,” Huey remarked.

{kind=link}

I know 6.5% for a mortgage is nasty but I’ve owned five houses and that’s the lowest rate I was ever offered. Bought my first house in 1970 at 8.5%, the second in 1972 and the third in 1975, both at over 9%. The only good rate I ever had was 0%, on my current house I bought for cash. In my view the largest single cause of the GFC was too many people buying houses they couldn’t afford so they could use them as banks. Around 2006 I noticed some data in an out-of-the-way spot in the WSJ showing various metrics of risk in the mortgage market. One piece that caught my eye was the percentage of new mortgages on which no payment had ever been made. By mid to late 2007 that number was well into double digits and the six-month default rates were getting positively scary. I wasn’t really paying attention to CMOs at that point, although my largest single asset holding was in Vanguard’s Ginnie Mae fund, a great earner at the time. With a large minority of folks in the housing market unable to pay for what they bought back then, maybe looking at those default trends might be in order once again.

My regional is talking 8% on a commercial industrial balloon renew this year. They are also quite-literally advising I seek out alternate funding sources despite having a multi year lease tenant and ~1/4ish mortgage to market value on the property. Meanwhile at the day job (architecture) we had a recent bid package come in 15% over with highly credible estimators on the team. No end in sight on the ground for this tightening multiplied by inflation cycle. Meanwhile we turn away jobs via talent supply issues.. Go figure.