“Despite the bank being in sound financial condition prior to March 9, investors and depositors… initiat[ed] withdrawals of $42 billion in deposits, causing a run on the bank,” California’s Department of Financial Protection and Innovation explained, in a filing describing the circumstances behind Silicon Valley Bank’s overnight insolvency.

The regulator cited SVB’s “mid-quarter update” — which announced a capital raise and detailed the fire sale of $21 billion in Treasurys and MBS at a large loss — as the proximate cause of the panic.

To be sure, it’s never a good sign when you have to raise capital on short notice, particularly if you’re a bank. And fire sales are especially inauspicious. But bank runs are, at heart, crises of confidence. Banking is a confidence game, after all, so it’s reasonable to assess that a major catalyst behind the avalanche of withdrawals was the simultaneous exhortation from a who’s who of VCs to their portfolio companies, who were advised to get their money out of SVB.

“As of the close of business on March 9, the bank had a negative cash balance of approximately $958 million,” California Commissioner Clothilde Hewlett went on, noting that SVB tried to “transfer collateral from various sources,” but ultimately couldn’t meet its cash letter with the Fed. “The precipitous deposit withdrawal caused the bank to be incapable of paying its obligations as they came due,” Hewlett remarked.

Although the FDIC said the amount of deposits in excess of insurance limits at the time SVB was shuttered was “undetermined,” the bank’s annual report showed that out of $173.1 billion in deposits held on December 31, 2022, $151.5 billion exceeded the FDIC insurance limit.

I won’t pretend to conduct any sort of industry-wide assessment for comparison purposes, but suffice to say a lot of depositors weren’t protected. Among them: Circle, which runs USD Coin, the fully-reserved stablecoin that functions as a linchpin of the crypto ecosystem. It’s fair to call USDC the gold standard of stablecoins. But it broke the peg on Friday evening in New York, and Coinbase “paused” conversion to real USDs (“coins,” bills and otherwise).

“Following the confirmation… that the wires initiated on Thursday to remove balances were not yet processed, $3.3 billion of the ~$40 billion of USDC reserves remain at SVB,” Circle said Friday. “Like other customers and depositors who relied on SVB for banking services, Circle joins calls for continuity of this important bank in the US economy and will follow guidance provided by state and Federal regulators.”

Dante Disparte, Circle’s “Chief Strategy Officer,” sounds like he wants a bailout for SVB. “Circle is currently protecting USDC from a black swan failure in the US banking system,” he said on social media. “SVB is a critical bank in the US economy and its failure — without a Federal rescue plan — will have broader implications for business, banking and entrepreneurs.” As FT quipped in the hollowed-out remains of what used to be its star-studded “Alphaville” column, Disparte “was presumably consulted on the group’s strategy of harvesting interest on uninsured deposits at a specialist regional bank,” given that he’s head of strategy.

Bill Holdings, which provides cloud-based services to small and midsize businesses, said $300 million of its $2.6 billion in corporate cash and equivalents was stuck at SVB. “These corporate deposits are largely uninsured, and it is unclear how much of this cash will be unrecoverable,” Bill said. In addition, $370 million of cash held in trust on behalf of customers was at SVB, although the company said “a significant portion” of that sum will probably be recovered through various mechanisms. Bill said it “strongly believes” it can meet working capital and capex needs “regardless of the amount of funds recovered from SVB and FDIC.” Bill’s position is tragically ironic. The company “simplifies, digitizes and automates back-office financial processes” for small firms. Now, 10% of its corporate cash and FBO funds are tied up in a bank failure.

And it just goes on. And on. And on. Sonder Holdings, a short-term rental management company whose lofty ambitions include a plan to “become the most admired hospitality brand in the world,” has a couple of million in operating cash at SVB, and $20 million stranded in deposit accounts. The company also had a $60 million line of credit with the bank.

The US media (both financial and general interest) was awash with stories on Saturday about the ramifications of SVB’s failure for companies trying to make payroll. At the risk of overstating the case, it’s possible, albeit unlikely, that this could tip the dominoes on a recession for the US economy if it’s not handled properly.

There’s not enough time to map this out if you’re the government. If you don’t act preemptively to provide clarity, you’re gambling on a chain reaction. Employees may not be paid on time, vendors likewise, the vendors have employees too, and everyone involved participates in the broader economy. And that’s just the near-term fallout from the ambiguity around the uninsured deposits.

In the medium-term, there are obviously all kinds of questions about regional banks’ risk profile, and if you start getting runs on banks that don’t have anything to do with “flashy” sectors of the economy, then you’ve got an honest-to-god Main Street problem. That’s really bad. Although it’s difficult to imagine that “regular” banks have such a high ratio of uninsured deposits to total deposits, the fact that this is even a discussion speaks to the risk that lending decisions could be impacted by the fear factor. Less lending means less income for banks, but it also means choking off credit to average people and businesses. That could increase demand for cash, setting up withdrawals. And SVB isn’t the only bank with unrealized losses on a bond portfolio.

Even something as seemingly expendable as a stablecoin isn’t really expendable. If trust in USDC is eroded such that there’s a run on the coin, the assets that back it would need to be sold. They’re liquid, and they’re short-dated, so that’s not really the problem. The issue is that USDC operates in the crypto ecosystem as the equivalent of a federal money market fund. If it’s not 1:1, then… well, then it’s an issue. USDC is pledged, staked and rehypothecated all over the cryptoverse.

Do note: Not all companies who had deposits at SVB enjoyed a direct line to powerful VCs, which means not everybody got the memo in time. Ashley Tyrner, the CEO of FarmboxRx, spoke to Axios about that. “It seems that while the VC circle was publicly boasting their support for SVB in an attempt to stabilize the panic, they were calling their portfolio companies behind closed doors telling them to move funds immediately,” she said. “The businesses who were venture-backed were at an advantage of having a heads up, while those of us who were unable to secure venture funding were left in the dust during a total system collapse.”

Tyrner also gave an interview to Reuters. As it turns out, she was on vacation with her family in Costa Rica on Thursday. That sojourn was interrupted by panicked messages from FarmboxRx’s COO, who’d initiated what Reuters said was “an eight-figure wire transfer” in an ultimately futile attempt to get all of the company’s money out of SVB. “She’s just pinging me over and over and texting my kid,” Tyrner told Reuters. “My heart stopped. ‘My bank is going to go under’ had never crossed my mind,” she marveled, despairingly.

At heart, the problem at SVB was simple. I’ll briefly walk through it.

SVB’s deposit base was comprised disproportionately of money from cash-flush startups and would-be unicorns who didn’t need loans because… well, because “cash-flush.” Notwithstanding the self-evident notion that if you offer to lend money, somebody, somewhere will take you up on it, it’s reasonable to assess that SVB’s (ultimately fatal) exposure to interest rate risk was the result of insufficient loan demand relative to deposits, contextualized by the near complete absence of short-dated, risk-free securities offering any semblance of yield. SVB did what you’d do in that sort of conjuncture — they took on extra risk (not credit risk, but rate risk).

You could fault the Fed (for the dearth of viable cash alternatives and also for creating an environment where anything with a passable elevator pitch could score tens and hundreds of millions in funding) or you could fault SVB (for poor hedging and generally mis-managing their rate risk). But I’m not sure what good finger-pointing does now.

When the operating environment turned more challenging last year for companies which benefited most from the go-go, free-money regime, cash needs at startups (so, SVB’s depositors) increased. That sowed the seeds for a crisis.

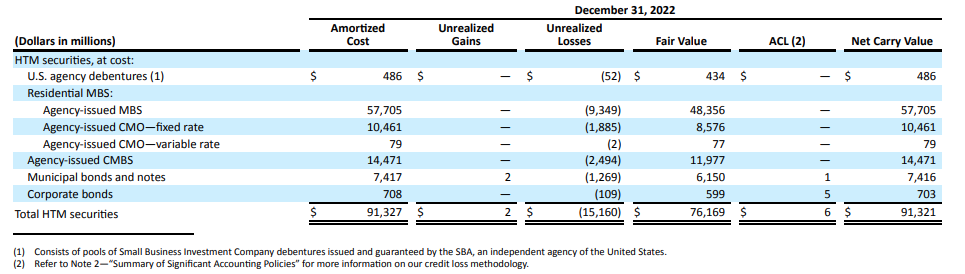

More than 90% of the bank’s domestic deposit base was uninsured. At the end of last year, it had $15 billion in unrealized losses in its HTM portfolio.

According to one retelling, based on the account of a source who spoke to Bloomberg, Moody’s told SVB last week that its unrealized losses put the bank at risk of a multi-level downgrade. At that point, a run on deposits was all but assured.

If you tell Moody’s to pound sand (i.e., “Do your worst, devilish fiends!”) then you’re rolling the dice on a several-notch downgrade and the accompanying rationale, which would call attention to the underlying issues.

If you tell Moody’s you’ll fix it, that means acknowledging the underlying issues by realizing a mark-to-market loss on some of your bonds, and in SVB’s case, it also meant a capital raise.

As Bloomberg dryly noted, it didn’t ultimately matter because SVB “was downgraded by Moody’s on Wednesday anyway.”

Shorts made $500 million in the collapse, assuming they can harvest the windfall. CEO Greg Becker sold $3.6 million of company stock on February 27.

{kind=link}

Would you classify svb as a ‘hub’, as described in ‘Tower in the Square’, by Liall Ferguson?

I said this here previously. There will be contagion. It would be ideal if the regulators could arrange a merger over the weekend. For you monetary hawks out there, you can forget 50 BP hike now. If the fomc was smart, they would pause qt and reevaluate their pace of hiking short term targets. The safety and soundness of the banking system now takes precedence.

Maybe I’m missing something really obvious, but I have to ask, why would anyone leave such large uninsured balances in a bank when there short term Treasuries, money markets and such safer alternatives available (often providing, at least for the last year or so, not insignificant yields)?

H-Man, it appears the domino’s are just beginning to fall and it may be a rather long chain before it ends.

I may be too old to think, but I can’t see why there needs to be some long chain of failing banks from this situation. Its main assets will survive in tact when taken over. Losses marked to market will be picked up at their reduced value and losses written against the new bank’s earnings, creating nice non-cash tax losses and if recovered, they will create taxless capital gains. The biggest problem is the potential loss to the ventures with cash in the bank. FDIC doesn’t have to pay corporate depositors as far as I know. However, if the government finds a way to bail these guys out then there really aren’t and losing dominoes I can see.

I’m with ya. Famous last words and all, but this doesn’t strike me as anything resembling 2008. We could see a shakeout in some tech companies that likely weren’t long for this world anyway, but any company worth its salt will find the liquidity it needs until SVB deposits get sorted out and I honestly don’t think the Fed needs to do anything other than make it clear that they won’t allow this to become another Lehman Brothers moment. Worst case, I could see them providing the backstop to avoid contagion.

Frankly, if we can make it through Covid without a massive economic depression, it’s going to take a lot more than this to cause any major damage across the economy.

So, the CEO sold a bunch when he saw the writing on the wall???

Jeffries went out bidding companies with money stuck at SVB this morning, maybe even yesterday evening…I’m hearing SVB had no head of risk from April 2022 till early 2023

“Shorts made $500 million in the collapse…” Hmmm, i wonder how many of the shorts might also have been advising friends (or management of portfolio companies with deposits at SVB) to get their money out asap? [I’m not a conspiracy theorist, just cynical out of experience, about ways of the financial world.]

I don’t have a reasoned opinion on whether the banks will start to “zipper” (a rock-climbing term for a very bad thing), although my gut feeling is “no”.

The Fed should ideally stop tightening when it has carried out its inflation mandate, not based on poor risk management by a regional bank, so I think the federal govt should ideally facilitate a takeout of SIVB/DINB by a big bank. Alternatively, extend credit to address liquidity (how long it will take to sell SIVB’s loans and other less liquid assets) but not solvency (if SIVB’s recoverable assets are insufficient to make uninsured depositors entirely whole, then they get haircuts).

So what does an investor do while waiting to see what happens? Work on bank stocks? Banks are irritatingly “black box”-ish. Instead of trying to puzzle through FRC or PACB, I spent the day working on a broker that got hammered last week on pre-existing cash sorting concerns plus presumably heightened duration risk concerns. Brokers are less of a black box than full-on banks, even if they share some bank-like drivers, so I think one can reach some reasoned conclusions without having to be a “bank whisperer”.

H-Man, SVB has wiped out all shareholder equity, deposits are another problem. If I have $50M in deposits, it could be $250K depending on the what the assets get in this market. If the assets of SVB are a Treasury/swap portfolio, it is a declining asset as the long term rates compress the short term rates. Like who is going to buy a losing trade? I guess somebody who wants a very large discount. So what are those assets worth when the bank is burning. So when that problem is solved, what do you do with uninsured deposits? I guess you just tell them have a nice day and, by the way, you have no money. Meanwhile $66B of loan commitment goes up in smoke, so no new money for the VC’s and no new money for companies. Time to layoff people, not pay people or suppliers like Etsy. Not really good times for the tech world.

Problem was borrowing short and lending long. Not a good plan with an inverted curve. How do you make money on the spread when your money leg pays less than your borrowing leg? So who else was playing that game probably tells us how bad it can be. I guess it may be a function of the capital cushion which will tell us who makes it and who sinks. Right now it looks like there could be a lot of burning boats. Time will tell.

For SVB depositors with deposits in excess of the $250K FDIC insurance limit, this seems to boil down to two basic issues. The first is how long will it take to get access to their funds in excess of $250K (for example, to make payroll etc) and the second is how much of their deposits in excess of $250K will they lose? At worse, given the “collateral” behind the deposits is down 10% or so in value vs. cost, then each large depositor’s recovery shouldn’t be any worse than 80 to 90 cents on the dollar.

But of course, there will likely be a fed gov’t decision to protect the full principal of all depositors if only domestic depositors (to prevent any near term runs on any other banks). I spent some time on the internet trying to find any examples of uninsured depositors in failed FDIC-insured banks getting less than 100% of their deposits, and since early 1990s I couldn’t find any such situations. The FDIC charges insurance premiums to its covered financial institutions based on a reasonably complicated formula that does not appear to exclude deposits in excess of $250K per account. Maybe going forward we can just drop the charade that FDIC insurance is limited to $250K per account (or $500K for a married couple with both names on the account)…

Yep, I’m not an expert on bank balance sheets, but was very curious to dive in. If you look at their most recent 10-k and investor presentation and add up all the assets, apply some generous discounting on their MBS holdings (they even have a fair value listed as of Dec 31), and loan portfolio, they are very close to being able to cover all deposits. The FDIC will distribute the $250k Monday, another dividend by the end of the week at the latest (based on FDIC press release), and likely release another large chunk after offloading the MBS holdings. The FDIC has done this before and will likely be able to move quickly to get money back in the hands of depositors.

To me, the only real question is how quickly can startups find new sources for credit facilities. Again, I think it’ll be the companies that were likely headed for extinction anyway that will be the only ones impacted beyond a short-term inconvenience. Investors won’t let companies go bust unless they think the companies were headed in that direction anyway knowing that depositors will be mostly made whole in a relatively short timeframe.

“It’s reasonable to assess that SVB’s (ultimately fatal) exposure to interest rate risk was the result of insufficient loan demand relative to deposits”

Mr. H – Can you explain why insufficient loan demand would have prevented the liquidity issue? If bank is lending out money, doesn’t that still tie up capital?

My 2 c

Bank loans would have had higher interest rates (4-5%), often floating, and shorter amortization (3-5 year maturity), thus substantially higher cash flowing back into SIVB, compared to the MBS that SIVB bought, which had fixed and low yields (I think I read 1.8% ish on SIVB’s portfolio), long maturities, and negative convexity.

With more bank loans and less MBS in its portfolio, SIVB might have had a better chance of meeting the deposit outflow from startup cash burn, and would have had lower unrealized losses from rising rates, thus less chance of accelerated outflow from investors/VCs getting worried.

Negative convexity of MBS:

https://www.capitaliq.spglobal.com/interactive/lookandfeel/4017464/3.pdf

I think that to one degree or another, during 2020-22 most US banks faced the problem of absorbing more deposits (liabilities) than they could sensibly deploy into adequately-yielding loans and securities (assets). Money market funds faced similar problems. SIVB had the problem in a big way, because its deposits grew so fast (VC bubble and SIVB strategy) and its customers had so little need for loans.

SIVB management also seems to have not done a great job controlling risk.

The fortune link I found from hacker news

https://fortune.com/2023/03/10/silicon-valley-bank-chief-risk-officer/

What can the bank sell to get liquidity for depositors who want their money right now?

The leadership at SVB (maybe minus a critical piece Chief Revenue Officer) bought ($80B?) MBS of 10 year duration with 1.8% yield, and nobody now would buy those (or would only pay very little) when right now you can buy a TBill for 4.7%

Like JohnLiu suggests, it takes work to make loans (at a higher rate of return and shorter duration) to reputable businesses… and those loans are more valuable such that they could easily re-sell them to other banks.

Similarly they didn’t unwind their position during 2022 as inflation became glaringly high and the Fed obviously raised interest rates a lot. If they want to truly clean up banking I’ll be interested if they search all the SVB emails and personal financial transactions from 2022 to see who there was shorting their own downfall.

Forbes: “Thanks to Barron’s, most of us learned only yesterday that on February 27, SVB’s President and CEO Greg Becker sold 12,451 shares at an average price of $287.42 for $3.6 million. That day he also acquired the same number of shares using stock options priced at $105.18 each, a price much lower than the sale price. This was the first time that Becker had sold his company’s share in over a year.”

https://www.forbes.com/sites/mayrarodriguezvalladares/2023/03/11/warning-signals-about-silicon-valley-bank-were-all-around-us/

To finish this mini-essay: FDIC probably ought to find some buyer of last resort that’s willing to hold MBS at 1.8% for 10 years and try to make most of the businesses whole (ironically the majority of startups are doomed anyways and VC, as Softbank taught us, is meant to burn money)…

If all the paperwork (digital) is in order then a quick orderly return of cash (which the Fed has plenty of) should prevent further bank runs this week.

(Unless more CEOs are dumb enough to burn $1.8B and announce they’ve sold all their AFS hope no one notices).

By selling shares and exercising options, he was just doing his part to help recapitalize the bank 😉

I’m going to finish my bottle of Columbia River valley pilot noir (damn autocorrect) and watch The Big Short again. I am really enjoying this since I increased my cash position greatly on Friday, especially selling California biotechs. Great article, great comments. Maybe the domino chain will fail but I bet otherwise.

This guy seems to have the Midas touch in reverse, everything he touches turn to s**T

Joseph Gentile is the Chief Administrative Officer at SVB Securities.

Prior to joining the firm in 2007, Mr. Gentile served as the CFO for Lehman Brothers’