I’ve mentioned this on several occasions of late, but it’s worth repeating: Career risk is a thing that matters.

If stocks are running away to the upside, the “Why?” isn’t especially relevant depending on who you are. Hence the “chase” dynamic that (too) often leads to overshoots during rallies not built on a solid fundamentals-based foundation.

2023 is an example of just such a rally. Earnings are imperiled as the margin outlook darkens, and although the US economy looks like it may yet avert a recession, the downside is a Fed with carte blanche to achieve a higher terminal rate and hold it for what’ll seem like a long time.

To a very large degree, what drove the rally early this year was — wait for it — the rally itself. “We would contend once again that price is dictating opinions more than objective analysis,” Morgan Stanley’s Mike Wilson said. “Stocks and bonds rallied initially on the FOMC event so it must have been dovish!” he exclaimed, quoting many an unnamed market observer and journalist, whose Fed takes were dictated by the price action instead of the actual policy statement or press conference. After January payrolls, such dovish interpretations looked misguided.

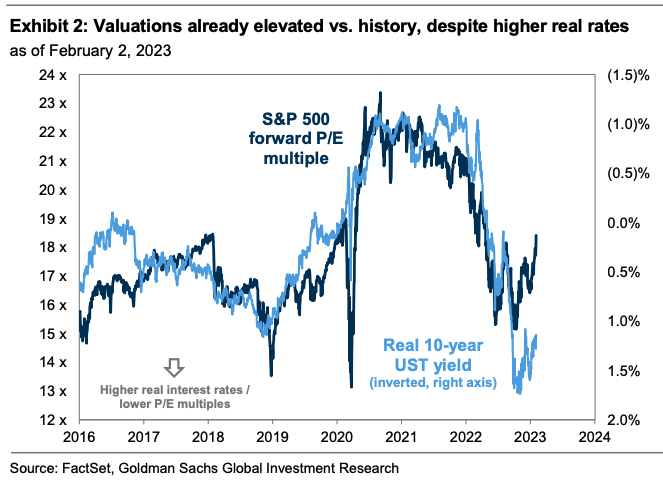

Wilson, like Goldman’s David Kostin, pointed to a glaring disconnect between the re-rating in US equities and real yields. The latter simply haven’t come down enough to justify the stock rebound. The figure on the right illustrates the (familiar) point.

“The S&P’s forward multiple is several turns rich based on the current real rate backdrop,” Wilson remarked.

The figure on the left above illustrates the chase from institutional investors, which Morgan Stanley described as “even more aggressive than the prior two bear market rallies last year.”

“We argued that supportive seasonals at the start of the year and light positioning will still be helping as we move through Q1, but positioning is quickly normalizing, and the question is whether there will be fundamental confirmation for the next leg of the rally,” JPMorgan analysts led by Marko Kolanovic wrote Monday, while retaining a cautious tone amid rampant macro uncertainty. “We think it might end up lacking,” they added, reiterating expectations for “an air pocket during Q2 and Q3,” when activity data and earnings could be weaker. JPMorgan suggested investors might “use the current strength to reduce exposure.”

For his part, Morgan’s Wilson said the huge US jobs beat, distorted or not, was another indicator that the labor market remains quite strong. That, he went on, “means there really is no reason for equity investors to get excited about a cut in rates and/or further relief from the back-end of the Treasury market.”

{kind=link}