“Be careful what you wish for,” Morgan Stanley’s Mike Wilson warned, “way” back in August. He reiterated that warning this week.

It’s a reference to slower inflation, which most investors view as a kind of cure-all tonic for everything that’s ailed markets for the past 12 or so months.

While it’s certainly true that decelerating consumer price growth is a prerequisite for a return to the kind of benign macro-policy conjuncture that lulled (too) many market participants to sleep over the past two decades, receding inflation could be bad news for corporate bottom lines in the very near-term.

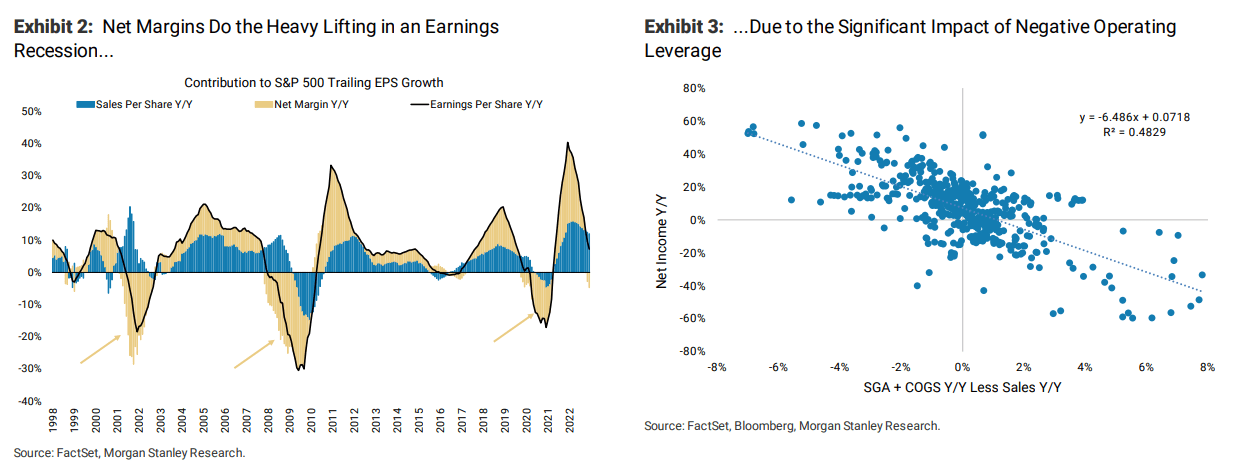

“The main driver of our concern is falling inflation. Yes, falling inflation,” Wilson said. Although higher nominal GDP can sustain corporate top-lines even as real GDP decelerates, margin compression looms. “The reason is negative operating leverage, as the rate of change on costs exceeds the rate of change on sales,” Wilson went on to write.

For Mike, this dynamic is likely to get “much worse before it gets better,” and he seems to doubt seriously the idea that consensus, let alone the average investor, understands why.

Although the prices gauge in the ISM services survey remains elevated versus its own history and particularly against the readily apparent deflation on the manufacturing side of the economy, it’s nevertheless well off the highs.

December’s print, 67.6, was the lowest since January of 2021.

That portends slower consumer price growth which, as Wilson wrote, is “just another reason to believe inflation is likely to come down faster than most are expecting, including the Fed.”

Great, right? Yes. But also no.

“That’s good news on the surface [but] the issue for equity investors is that the fall in the CPI is lagged, meaning the Fed will likely be unable or unwilling to cut rates anytime soon,” Wilson warned, before elaborating:

In other words, falling inflation is going to be a significant headwind for profit margins given the sequencing of costs falling later than end price. There is also the timing issue of cost accrual on the balance sheet over the last 12 months that will now flow through to the income statement in 2023. With the CPI and other popular measures of inflation falling even later, the Fed will not be in a position to offset falling earnings.

Note that the big downside miss on the headline ISM services print was greeted warmly by markets, as it reinforced the message from December payrolls, which showed that although hiring remains robust, wage growth is decelerating. Cooler is better, and inflation is concentrated on the services side of the economy now, so a recessionary ISM services print on the heels of a downshift in the pace of average hourly earnings growth was a textbook example of the “bad news is good news” market regime.

But as more than a few commentators pointed out on Friday, that ISM services print was very ominous for the economy, even at a time when ominous news is generally welcome to the extent it portends less aggressive monetary policy.

None of that was lost on Wilson. “Historically speaking, a breach of 50 [on the ISM services] measure is quite rare and almost always means a more significant decline is coming,” he said, before spelling it out. “In other words, we caution against interpreting this data print in a ‘bad is good’ context beyond very short-term price action… we think we’re quickly approaching the point where ‘bad is bad.'”

The bottom line for Morgan Stanley is that consensus, and market participants more generally, are blissfully unaware of the implications of falling prices for margins, which Wilson suggested may “outweigh any benefit from the perceived Fed dovishness equity investors are dreaming about later this year.”

In Wilson’s view, earnings forecasts for 2023 “remain materially too high.” Recession or no recession.

Mike Wilson, one of the few who understands the power of operating leverage. Thanks for this great post.

With all the high fixed cost industries in our economy, including all hospitality, health care, utilities, manufacturing and more, small changes in volume/revenue will result in large changes in profits. Downward is magnified with operating leverage. Doesn’t seem all the rose-colored glasses forecasters get that problem.

Good point by Wilson.

Could offset some of this by tilting toward US companies w/ FX exposure.

Thanks for highlighting this Walt!

The cure? Higher labor and capital productivity. That translates to fading employment, lower capital spending and lower interest rates. It’s coming, but not right away.

With regard to “higher labor productivity”, all “at home” workers should be prepared for the call to return to the office!