Most of the focus this week will be on the US CPI report, what it means for next month’s rate hike and the extent to which it does or doesn’t help make the case for the market’s view that the Fed will ultimately cut rates by the end of 2023.

The Fed vociferously denies that rate cuts are likely this year. But it’ll take more than the protestations of technocrats whose forecasting track record suffered a series of grievous blows over the past two years to convince traders. Market participants understandably suspect policymakers will blink in the event a real recession appears imminent, irrespective of where inflation is by then.

While an economy-wide recession may still be a few quarters away (and may not occur this year at all, according to some), the long-rumored earnings recession is upon us. Or so we’re told. We’ve heard that before, but decelerating corporate profit growth is now all but a foregone conclusion. I suppose the proverbial can could be kicked by one more quarter, but that’d be it. And even if that ends up being the case, the deluge of results due over the next three weeks won’t suggest earnings growth was robust in Q4.

For the full year, many top-down strategists suspect that corporate profits will be flat, at best. You don’t have to be an incorrigible bear to predict margin compression and, as detailed here over the weekend, the C-suite is probably reaching the limits when it comes to pricing power. There’s only so much Americans are going to pay for a Pepsi. After all, you can achieve obesity just as easily with the store brands.

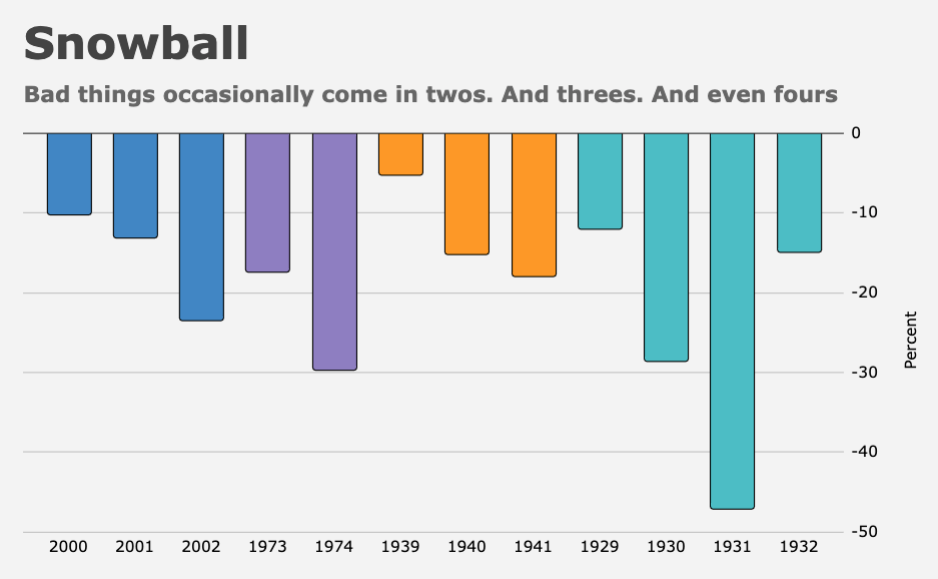

Revision sentiment is now the most negative in decades if you don’t count the GFC and the pandemic collapse. Indeed, we’re not too far from plumbing those depths on a three-move moving average basis.

Based purely on revision sentiment, we’re in a recession.

If you ask Goldman, there are three downside risks to 2023 EPS. None of this is “new,” obviously, but as the focus shifts to corporate results over the next three weeks, it’s important to keep the context fresh in your mind.

According to the bank’s David Kostin, three identifiable downside risks more than outweigh the prospective boon from China’s re-opening. “Weak consumer demand would limit firms’ pricing power and pressure profit margins,” he wrote, noting that “store traffic for the 2022 holiday season remained muted relative to 2019 levels and early sales results point to soft consumer spending.” In addition, Goldman’s internet analysts see more promotional activity, which may crimp gross margins.

Although tax policy in 2023 should only have a minimal effect in the aggregate, it’ll disproportionately impact sectors with the lowest effective tax rates, including tech, which has enough to worry about as it is. Between a 15% minimum tax on corporate book income, a 1% excise tax on buybacks and the phasing out of capex deductions included in previous legislation, tax provisions might lower EPS by 3%, Kostin went on to say.

Of course, the most pressing concern for corporate America is a recession. Goldman’s recession probability for the US economy is well below consensus, but at ~35%, it stands well above the unconditional historical average.

“The biggest risk in 2023 is a potential recession, in which case S&P 500 EPS could fall by 11% to $200 and the index could trough at 3150,” Kostin reiterated, on the way to again cautioning that “concentrated sector weakness could lead to larger EPS declines than our forecast.”

SPX 3,150 would entail the index falling sharply for a second year. Recall that it’s exceptionally rare for the S&P 500 to log consecutive years of negative returns, but when it does happen, the second year is typically worse than the first.

In remarks to Bloomberg’s Vildana Hajric and Michael Regan, Fidelity’s director of global macro, Jurrien Timmer, reminded market participants that although the multiple compression stage of the bear market is mostly behind us, “the PE is only as good as the E. The E is what the question is for 2023.”

{kind=link}

I’m expecting a kitchen sink and guide down earnings window. Corporate financial reporting has grey areas and management has the ability to massage results with electing to take items with negative financial impact when they choose. The current market narrative means the opportunity to take these negatives is now. Then management will guide down to lower the bar for 2023 as much as possible.

Excepting a soft landing to materialize and be the accepted narrative for most of 2023, earnings will beat these lowered expectations and possibly by a lot.

I’m expecting this all to play out as a near term peak in equities this week, a general down trend through March, then a strong bounce through Aug/Sept.

“The Big Bath” it’s called. It’s especially popular during leadership transitions. Pull forward every expense you can, post a disastrous quarter, and then future quarters come out smelling like roses.

One of the many things which majorly irk me is when I hear someone say “earnings were pretty good” just because they managed to exceed some much-reduced estimates. Often they have no clue when you ask what the change was from a year earlier.

But, that’s what we trade on.