Allahu Akbar!

Inflation in Europe receded more than expected in December, data out Friday showed. At 9.2%, headline price growth was the slowest since August.

The flash estimate for last month came in well below the 9.5% consensus expected and marked the first single-digit print since September.

The data came on the heels of ostensibly encouraging figures out of Germany, France, Italy and Spain.

Unfortunately, that’s where the good news stopped. Core inflation ran at 5.2% across the euro-area last month, up from November’s annual rate and a new record. On a MoM basis, core rose 0.6%, compared to a 0.3% drop on the headline gauge.

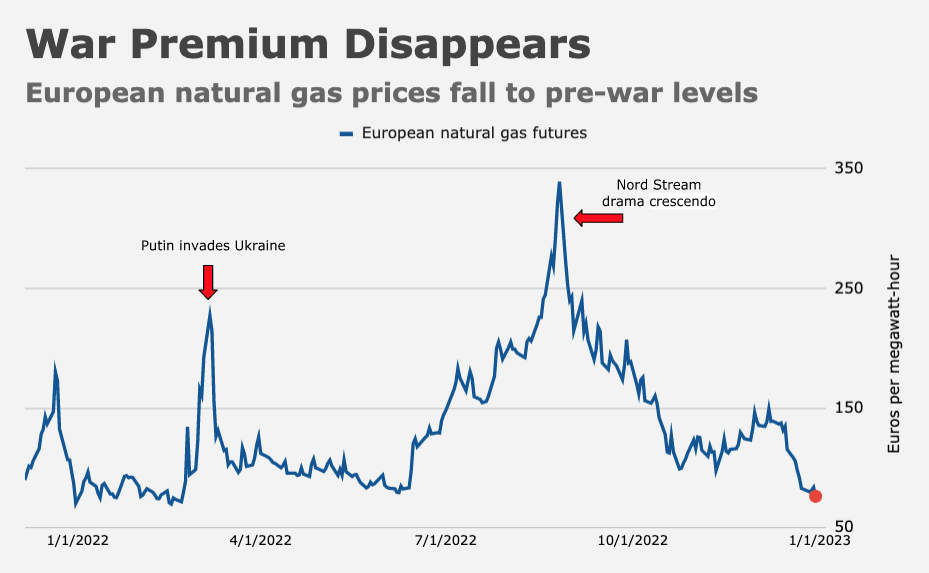

Energy price growth decelerated to “just” 25.7% annually, down 6.5% on a monthly basis. That was solely responsible for the favorable headline print.

The month-to-month drop in the headline gauge was quite large but, again, looks can be deceiving. “A combination of price caps and lower oil and natural gas prices have caused a significant dip in energy inflation, which was the main driver of the decline in headline inflation,” ING’s Bert Colijn remarked.

Recall that natural gas prices in Europe recently gave back the entirety of their war-driven gains, and oil prices have likewise fallen sharply. Between those declines and official efforts to cap prices and otherwise assist struggling households, Europeans are enjoying some measure of relief after months spent staring down an existential energy crisis.

Outside of that, there wasn’t much to celebrate. Price growth for processed food, alcohol and tobacco rose to 14.3% in December, up 0.9% MoM, while inflation in unprocessed foods ran at a 12% annual rate, down from harrowing levels in October and November, but still untenably hot.

Services inflation was 4.4% last month in the euro-area. That was higher than November’s 12-month rate. On a MoM basis, services inflation rose 0.7%.

Obviously, the ECB won’t find much solace in Friday’s inflation figures. Virtually everything was bad outside of energy. Last month, Christine Lagarde struck a decidedly hawkish tone at the bank’s final meeting of 2022, and indicated markets should anticipate a series of additional 50bps hikes.

“While supply-side shocks are fading — not just energy, but also think of container prices and various production inputs — core inflation is still adjusting with a lag,” ING’s Colijn went on to say Friday, adding that “the next two months will be critical as many businesses traditionally change prices at the start of the year.”

As ever, I’d remind readers that inflation in Europe is primarily a function of energy prices and, as such, will continue to be hostage to the war. December’s energy-driven drop in the headline figure underscored the point.

And yet, I’d be remiss not to note that it does look as though inflation is broadening out in Europe. Notwithstanding inevitable demand destruction from recessionary dynamics, it’s possible the genie is out of the bottle in the euro-area too, particularly given that the ongoing rise in core prices will almost surely find its way into wage-setting.

Ultimately, though, I suppose we have to be thankful for any reprieve, however illusory and however fleeting.

{kind=link}