The Fed on Wednesday hiked rates by 75bps, as expected.

It marked the fourth consecutive three-quarter point move, and brought the total amount of tightening in 2022 to 375bps, excluding the impact of balance sheet rundown.

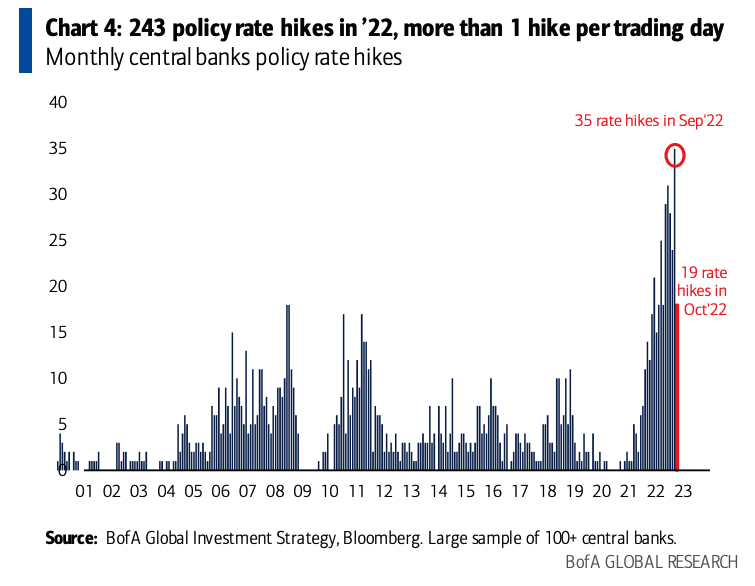

To restate the (painfully) obvious, there’s no recent precedent for this year’s rate hikes (figure below).

Whenever I observe that visual, I’m struck by the notion that, as cruel as 2022 was to equities and particularly to bonds, you could pretty easily argue it could’ve been worse. The Fed’s actions appear wholly anomalous on a “modern,” three-decade lookback.

That’s not to downplay the scope of the cross-asset malaise. There’s never been a worse year for a “simple,” balanced stock-bond portfolio, nor can I personally remember anything like a 21% rout for global high-grade credit. It’s just to say that considering how accustomed the world was to ZIRP, NIRP and LSAP, and the extent to which modern market structure optimized around those acronyms and “solved” for the associated dearth of yield by way of leverage, one might’ve suggested a year during which central banks delivered, on average, one rate hike per trading day, would be a year during which the world stopped spinning.

In any event, the November Fed statement came with notable tweaks. Specifically, the key third paragraph contained crucial additions. “The Committee anticipates that ongoing increases in the target range will be appropriate in order to attain a stance of monetary policy that is sufficiently restrictive to return inflation to 2% over time,” the Fed said, adding that,

In determining the pace of future increases in the target range, the Committee will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments.

At the least, that’s broadly consistent with the “step-down” narrative, which is predicated on the idea that policy will need to be more careful going forward given the possibility that the tightening already delivered will begin to manifest on a lag.

Headed into Wednesday, market speculation for policymakers to telegraph a potential reduction in the pace of rate hikes starting next month was running at a fever pitch. Based purely on the statement, those expectations were met. In September, there was no such language about how the Fed would approach “ongoing increases.”

The odds of another 75bps hike in December should be downgraded materially. The Committee is inclined to hike in smaller increments going forward.

At the same time, though, there was also no mention in September of the word “restrictive.” In all likelihood (and almost by definition) the new statement represented a compromise between the hawks and the doves. There were no dissents.

Terminal rate pricing came off by ~15bps late last month, after Wall Street Journal “Fed whisperer” Nick Timiraos tipped the Committee’s inclination to consider communicating the prospect for a dialed-back hike cadence. By Wednesday, pricing for peak Fed funds had retraced back to 5% following further evidence that the US labor market remains stubbornly resilient.

The statement language around the economy was unchanged. Inflation, the Fed reiterated, is “elevated, reflecting supply and demand imbalances related to the pandemic, higher food and energy prices and broader price pressures.”

All eyes turned to Jerome Powell, who made it through Wednesday’s press conference mostly unscathed, save a kind of “long way from neutral”-esque moment. Suffice to say the step-down nod was overwhelmed by the prospect of a higher terminal rate. Stocks were sharply lower, but that was probably just fine with this Fed.

{kind=link}