Wall Street’s most outspoken bear and the sell-side’s most famous bull agree on one thing at least: Central bank tightening has probably peaked.

“While the Fed has hawkishly surprised most investors this year, we’ve now reached a point where both bond and stock markets may be pricing in too much hawkishness,” Morgan Stanley’s Mike Wilson, who correctly predicted 2022’s bear market, wrote Monday. Wilson turned tactically bullish two weeks ago, and stocks have rallied smartly since.

Meanwhile, analysts led by JPMorgan’s Marko Kolanovic on Monday flagged “signals that the pace of central bank tightening has peaked” as an “important support for risk markets.” Kolanovic, the closest thing the sell-side has to a household name, has generally stuck to a bullish call on equities in 2022, although he recently cautioned that increases in “geopolitical and monetary policy risks” put the bank’s 2022 targets in jeopardy.

Both Wilson and Kolanovic cited (or alluded to) smaller-than-expected hikes from the RBA and the Bank of Canada, as well as the removal of key hawkish language from the ECB statement last week.

“Further rate hikes from here will likely be smaller in size,” JPMorgan said. “Other central banks are starting to slow their rate of tightening,” Wilson wrote.

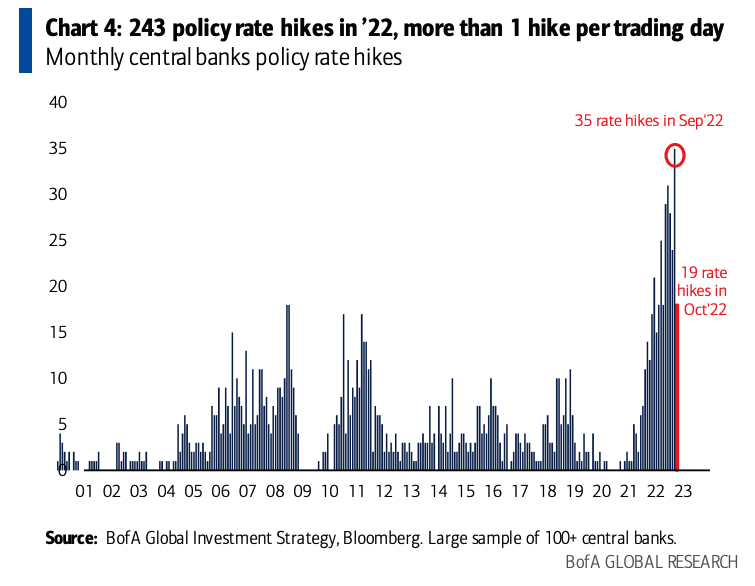

If there is a coordinated deescalation afoot, it’s mostly about “long and variable lags” or, more to the point, the distinct possibility that this year’s frantic pace of tightening has already delivered a latent recession in most developed economies. As a reminder, there’s been, on average, at least one rate hike per trading day in 2022, according to Bank of America. There were 35 in September alone, according to Michael Hartnett.

“Recent comments by FOMC officials (Vice Chair Brainard and SF Fed President Daly) emphasized the lags in the monetary transmission mechanism and the need at some point ‘to slow the pace of increases’ while the central bank assesses how hikes are affecting the economy,” this week’s installment of “JPMorgan View” reads. The bank’s analysts went on to note that “the RBA minutes from the October meeting, where officials opted to slow the pace of rate hikes to 25bps, find that the prior rapid rate of change in the cash rate level and long lags associated with tightening already delivered outweighed the risks to inflation expectations.”

For his part, Wilson flagged rising recession risks, as telegraphed by the three-month/10-year curve and other leading indicators (figures below).

Wilson editorialized around those a bit. “An inverted 10-year-3-month curve has a perfect track record of calling a recession within 12 months (with no false positives), so there is good reason the Fed should be pausing at this point,” he wrote, adding that the Duncan Leading Indicator has “just moved into negative territory” and likewise has a flawless track record.

“To the extent the Fed is data dependent, these are hard ones to ignore,” Wilson remarked.

“If our forecast is right, the most synchronized and aggressive global hiking cycle in 40 years will end by early next year,” analysts led by Kolanovic said. JPMorgan sees the Fed dialing down to 50bps at the December meeting and pausing “after one more 25bps hike” early next year.

{kind=link}

They should ask nick from wsj what he thinks!!!

Yeah, no. Every month since June analysts claim inflation has peaked and every month since June core has been flat or has risen, both in the U.S. and Europe. Real people in the real economy don’t really care about the second derivative.

True, but we aren’t real people in the real economy – at least not when our investor hats are on. Markets often bottom before the economy does. This bear market is very unusual, also.

So the market is pricing in 75 bp this meeting and 50 bp at the next, a mere 6 weeks later, and the market response may hinge unassuredly on the shoulders of Powell’s messaging and tone, despite the otherwise pretty solid underlying consensus on the rate path (if not in rationale, then at least on the point estimates). And while the Fed’s communication function is a key one, as a thought exercise imagine the market insanity if Powell announced no hike on Weds and gave no presser, then raised 125 bp six weeks from now without tipping it first. We get to the exact same place, in the exact same short amount of time, but would not all hell break loose in the process? Seems as dysphoric as many other things these days, and equally unhealthy.

For sure. Sound and fury signifying nothing? Maybe not for the folks manning the trading desks at big financial institutions. Bring back Glass-Steagall. (Which would do nothing to address leveraged speculative finance in the shadow banking system.)

I am one who believes we never should have repealed G-S in the first place. However, I also believe if we tried to return to it, the big banks would find many ways to get around it. Can’t put that toothpaste back in the tube.

H-Man, a couple of very smart guys agreeing on the same thing from different camps is something to behold. While I agree about the peak being reached, it is a treacherous descent.

So how do you play it ? That would mean deploying cash reserves soon since the market reacts 6 months or so ahead?

The CME Group Fed Watch tool has us at about 5% in March.

https://www.cmegroup.com/markets/interest-rates/cme-fedwatch-tool.html

I think that gives us about five quarter point hikes between now and march. (If I am counting right.)

So that’s either 2-2-1 in December February and March, or 3-1-1.

I suppose 2-1-1 is possible, as are higher and lower sequences, but the baseline case is five in total.