Jerome Powell needs to balance three considerations at the November FOMC meeting.

Most obviously, there’s very little, if any, evidence in the incoming data to suggest inflation has receded. The last CPI report boasted another uncomfortably hot monthly core print and a new 40-year high on the 12-month reading, while updates on the PCE price gauges offered no relief. Compensation and wage costs rose rapidly in the third quarter, and headed into October payrolls, there was no indication that the labor market was on the verge of rolling over in earnest.

At the same time, though, you could argue that some forward-looking indicators suggest there’s disinflation in the pipeline, even if literal pipeline inflation (as measured by producer prices) is still pervasive. As one astute reader pointed out over the weekend, the Fed may be keen to get ahead of the curve for once, as opposed to persisting in a penchant for fighting the last war. Speaking of the curve, the three-month/10-year inverted meaningfully last week, a development that won’t be lost on policymakers.

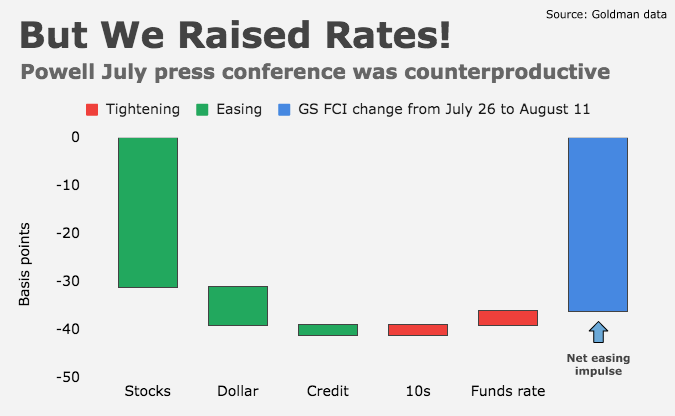

Finally, Powell is acutely aware of the potential for a dovish hike (or the perception thereof) to catalyze a counterproductive market reaction. Following the July FOMC meeting, financial conditions eased materially as markets judged Powell’s press conference to be insufficiently committal. He atoned for that a month later with a deliberately terse address at Jackson Hole.

It’s obvious that the Committee is pondering the best way to telegraph a potential “step-down” to 50bps hike increments. The Nick Timiraos nod and wink which kicked off a sharp drop in US real rates and a ~15bps decline in market-implied terminal rate pricing was indicative of those inclinations.

As I attempted to convey at the time (so, on October 21), a Timiraos article of that sort released just ahead of the Fed’s pre-meeting quiet period was almost surely a smoke signal. Mary Daly’s remarks, delivered just hours later, reinforced that assessment. The figure (above) underscores the point.

“We expect Powell to indicate that the FOMC will most likely slow the pace to 50bps in December, echoing a hint in the Wall Street Journal,” Goldman’s David Mericle said over the weekend, adding that the bank doesn’t expect Powell “to tie a slowdown to 50bps to meaningfully better inflation data, which is not a realistic expectation at such a short horizon.” Instead, Goldman said, “Powell will likely note that the FOMC aims to move deliberately but more cautiously now that the funds rate is in restrictive territory, and that the full impact on the economy of the very large tightening in financial conditions to date is not yet clear.”

That’s a nod to two of the three conditions mentioned here at the outset. There’s no chance that inflation decelerates enough between now and the December policy meeting to warrant any kind of overt dovish lean. So, Powell will have to explain any inclination to slow the pace of hikes by reference to “long and variable” lags and the notion that, following November’s 75bps move and an assumed 50bps increment the following monthly, policy will be restrictive, which warrants vigilance, if not yet an outright pause.

For what it’s worth, Goldman added a hike to their Fed forecast. The bank now sees hikes of 75bps in November, 50bps in December, 25bps in February and 25bps in March, for a funds rate peak of 4.75-5% (figures above).

Note that with the exception of the ECB, the Fed was last to the hawkish pivot party, which began in earnest a year ago, when the Norges Bank, RBNZ, the Bank of England and the Bank of Canada either hiked or started to make noise about tightening. Around the same time, the RBA was forced out of a short-lived experiment with yield-curve control. Fast forward a year and it’s a mirror image: Deescalations from the RBA, the BoC and the removal of key statement language by the ECB, all made the case for a burgeoning, coordinated step-down.

As documented here over the weekend in “Bad Pivot Optics” and “Pivot Buzz Looses Dangerous Animal Spirits,” any such step-down isn’t without risks. Inflation accelerated across most locales in September and October, according to the most recent data, so any deescalation is a leap of faith. It’s possible Powell doesn’t play along or, more likely, that his communications skills are found wanting.

One risk is a “rug pull,” inadvertent or intentional. “I really think there is potential for another rug pull coming down the road, either from the Fed acknowledging [inflation] realities again as early as [the November] meeting or worse, from inflation data remaining problematic and stay[ing] ‘sticky higher’ in Q1 2023,” Nomura’s Charlie McElligott said.

To be sure, it won’t be possible for Powell to duck questions about the December meeting. Timiraos will be the elephant in the room (figuratively in that everyone will want to know what the balance is on the Committee in terms of support for dialing back the pace and literally, in that I assume Nick will be at the press conference). Reporters will press Powell again and again on the step-down narrative, and given his spotty communications record, the odds of a faux pas are elevated.

A “mistake” could come in two forms. Powell could come across as too belligerent, hewing too closely to the strict “data dependent” script, risking a violent unwind of recent bullishness in equities and rates. Or he could go too far in the direction of acknowledging that, barring a worst-case scenario from the two CPI reports the Committee will see between now and the year’s final policy meeting, the odds are indeed skewed in favor of 50bps in December, risking a violent extension of the rally in equities, the proliferation of dovish rates bets and, perhaps most importantly, a sharp correction in the dollar, all of which could deliver a powerful (and counterproductive) financial conditions easing impulse, akin to that seen in the wake of the July meeting.

“We have penciled in 50bps [for December] and as such anticipate that Powell will begin setting the stage for a downshift to a less aggressive cadence of tightening,” BMO’s Ian Lyngen and Ben Jeffery wrote. “It remains to be seen whether the market reads this as a ‘soft pivot’ or simply an acknowledgement that as rates move into unquestionably restrictive territory, the bar is higher for each incremental increase.”

“The setup and signaling towards a steadier hike pace was always going to be challenging given the FOMC’s disregard for forward guidance and adherence to ‘data dependence,'” TD’s Priya Misra said. “We expect increased proactive communication from the Fed after the November FOMC meeting [but] given the unpleasant surprises in the inflation data over the past couple of months, we do not expect Chair Powell to signal an explicit commitment to a downshift at next week’s post-FOMC presser.”

I want to emphasize: That’s almost surely the plan. That is, the Committee would ideally like for Powell to thread the needle during the press conference by confirming a debate among officials about the appropriate pace of hikes beyond November’s 75bps move, while preserving the Fed’s optionality for a fifth straight three-quarter point hike in December in the event the inflation data comes in materially worse than expected.

In terms of market outcomes, the ideal follow-through from the Fed’s perspective would probably be market pricing for the December gathering stays at a coin toss after Powell’s remarks and, secondarily in terms of importance for policymakers, equities are a touch lower, with cash curves and the dollar mostly unmoved.

In my opinion, the odds of Powell threading the needle are about the same as they are with any post-FOMC press conference. You can interpret that as you see fit.

{kind=link}

Used to be political views were distributed along a spectrum before they becamse so hopelessly polarized and binary. Feel like the same thing is happening with financial conditions and interest rates. I look forward to the Fed re-exploring the vast unrecently charted space between the two poles of way to loose for way too long, and way too tight for way too short. My personal feeling is Powell’s approach should be to talk loudly but carry a soft stick next week. A knee-jerk anticipatory melt-up wouldn’t seem to serve his purposes, which is a lesson he’s already learned.

Yeah but the 75 bps hike is baked in. If they do only 50 bps, no amount of stern talking would stop a rally.

Agreed. So take the 75 bp this meeting, then stress inflation has not come down yet like they hoped and sugar coat it with a little long and variable lag topping of equivocation. No need to feed the animal spirits into December’s meeting until the December meeting.

Hello H.

I’d be curious to hear what you think of the data and calculations highlighted by Kevin Drum : https://jabberwocking.com/worker-comp-is-down-corporate-profits-are-up-imagine-that/

I haven’t heard anyone mention the possibility of an intermeeting hike. That is, if the FOMC goes 75bps next week, traders hear Chair Powell signaling 50bs in December, and equity markets explode to the upside, the FOMC, in theory, could come back with an additional 25bps/50bps increase before Thanksgiving. And it could signal that possibility at the meeting next week, just to keep everyone on their toes. Is that crazy? After the recent escalation in Ukraine (a halt to grain shipments) and paying $60 at the grocery store yesterday for the ingredients for one meal and a few staples, I’m thinking maybe not.

First, the US has to get through a “little thing” called Midterms and the resulting impacts.

@Emptynester Divided government (either literally or even if it’s just the out-of-power party picking up seats) is typically associated with bullish risk asset sentiment. Gridlock in Washington is, unfortunately, viewed by traders as the best possible outcome as it reduces the tail risks around fiscal policy.

The biggest risk around the midterms is obviously contested races and, down the road, Republican efforts to commandeer state legislatures in order to, among other things, change the process by which the president is chosen. I wish there were a more polite way to put that, and it’s not meant as a partisan statement. In fact, most GOP reps are openly enthusiastic about that evolving initiative, as are a lot of GOP voters.

The fireworks will be next spring, with the Republicans taking over Congress, an exploding budget deficit, persistent inflation, probably some kind of credit or EM event, god knows what in geopolitics and trade wars, and then the US hitting their debt ceiling. Worrying about whether they hike 50 or 75 in december seems so trivial compared to all the storm clouds gathering.

@mfn There’s no chance of that. Under any circumstances.

That’s too bad. After a decade-plus of being able to count on a Fed put, I feel like markets and Wall St, types have lost their fear of the Fed — which makes the Fed’s job harder than it needs to be.

H-Man, the market rally will continue on the (mistaken) belief the inflation tide has turned. Powell will find some kind of a silver lining on Wed. Toss in a not so warm to cool jobs report on Friday and the following week any modicum of an improved CPI print plus a Republican sweep in the House markets will rally until the sobering effects of the December data land. Inflation is not only sticky but stubborn. Just dealing with a bear market rally like late June to early August,

Market expects are 75, 50-75, 25, 25. Powell will have to convince market of a trajectory higher than that, to snuff out the pivot prattle. He could deliver 100 now, preview 100 next month, or preview repeated 50s next year. Any of those seems at odds with multiple governors’ statements in the past few weeks, almost everyone other than maybe Kashkari. I think more likely that his presser either leaves market expects unchanged or inadvertently lower them.