Markets may feel lackadaisical in the new week. It’s the middle of August, after all.

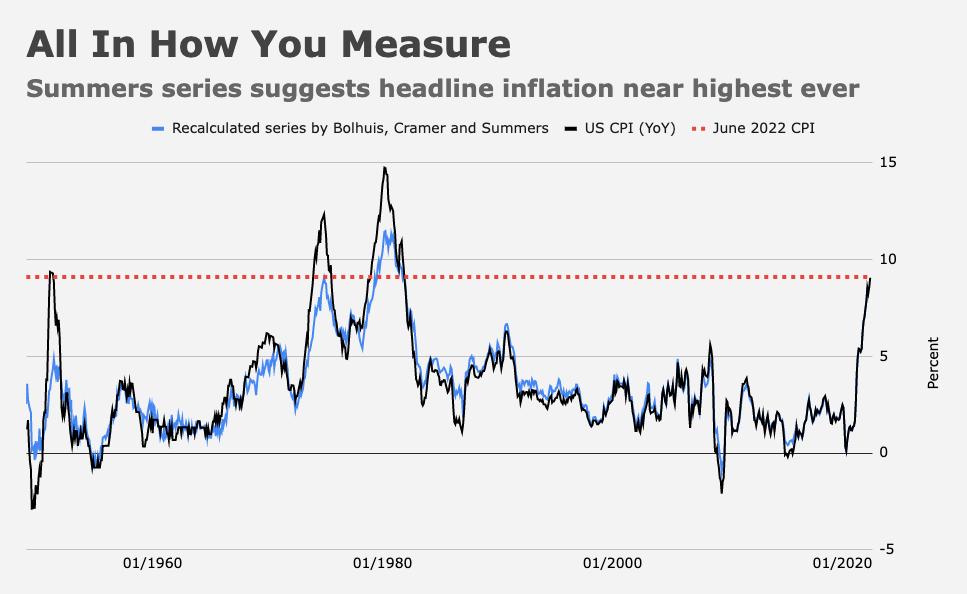

The data docket isn’t totally devoid of notables. In the US, retail sales figures for July will get top billing, as market participants continue to assess the health of the American consumer in the face of what, if you go by Larry Summers’s reconstituted series, may as well be the hottest inflation in the nation’s history.

Consensus expects a small gain from the retail sales print (figure below). Markets have focused more intently on monthly personal consumption data and particularly real personal spending figures, an update on which isn’t due until August 26, alongside PCE price gauge readings for July.

In the meantime, an update on nominal spending for goods (that’s all retail sales really are outside of restaurant receipts) will have to suffice. The decline in US gas prices over the past nine weeks could bolster discretionary spending, which suffered as pump prices soared alongside the cost of groceries.

At the margins, a robust read on retail sales could reinvigorate expectations for a 75bps hike from the Fed at next month’s meeting. A lackluster read on spending would favor 50bps. Absent a big upside or downside surprise, the numbers aren’t likely to move the needle either way, though. Last week’s cooler-than-anticipated CPI and PPI data took the edge off July’s red-hot jobs report. Put differently, the inflation figures offset the labor market data, leaving traders split on the size of September’s rate hike. Retail sales won’t be the tie breaker.

Earnings reports from a bevy of big name retailers are perhaps more germane for investors seeking clarity on the state of the consumer. Walmart, which delivered a high profile guide down late last month, reports this week, as does Target, whose struggles are well-documented. Results from Home Depot and Lowe’s will be scrutinized as well given the rapidly cooling housing market.

Speaking of America’s property bubble, this month’s round of housing data kicks off this week, starting with NAHB on Monday. Homebuilder sentiment dropped the second most on record in July and housing starts figures (due Tuesday) are expected to show a third straight monthly decline.

The figure (above) gives you some context for the interplay between sentiment and activity. Mortgage rates have pulled back from this year’s highs, but affordability remains challenging for many (most) would-be buyers. An update on existing home sales (Thursday) could show a sixth consecutive monthly decline.

A few hours after Wednesday’s spending update, the Fed will release minutes from last month’s meeting. The focus will be on the Committee’s shift to strict data dependence and the abandonment of forward guidance. “Ideally [the minutes] will assist investors with a more comprehensive understanding of the Committee’s current reaction function to realized inflation data,” BMO’s Ian Lyngen and Ben Jeffery said. “It goes without saying (although the Fed has) that a single data print such as July’s CPI release won’t be sufficient to deter the FOMC from pushing policy rates into restrictive territory.”

Rates are caught between a hot labor market and cooler inflation. The best way to summarize the situation is just to say that when we use the word “hot” in the context of the jobs market, we mean it unequivocally. By contrast, when we use the word “cooler” vis-à-vis the incoming inflation figures, we mean it relatively and with a long list of caveats. That juxtaposition argues for higher rates for longer, regardless of whether next month’s move is 50bps or 75bps.

Also on deck: The Empire and Philly Fed gauges. Markets will hear from Barkin, George and Kashkari. Kashkari is a born-again hawk, while George, an erstwhile check on the Fed’s most dovish inclinations, dissented two months ago in favor a lighter touch, citing the virtues of predictability. 2022 would have it no other way: Up is down and down is up. Equities came into the new week up markedly so far in H2, after being down handily in H1.

{kind=link}