The global tightening impulse accelerated on Wednesday, as New Zealand and South Korea stepped up their respective campaigns to bring down elevated domestic inflation.

New Zealand, a pathbreaker this cycle among countries whose monetary policy is generally subsumed under the developed market banner, delivered another 50bps rate increase, the sixth consecutive and third straight upsized increment (figure below).

The Committee described itself as “resolute” in the fight to bring inflation back into the target range which, in New Zealand, is between 1% and 3%. “It remains appropriate to continue to tighten monetary conditions at pace,” the bank said.

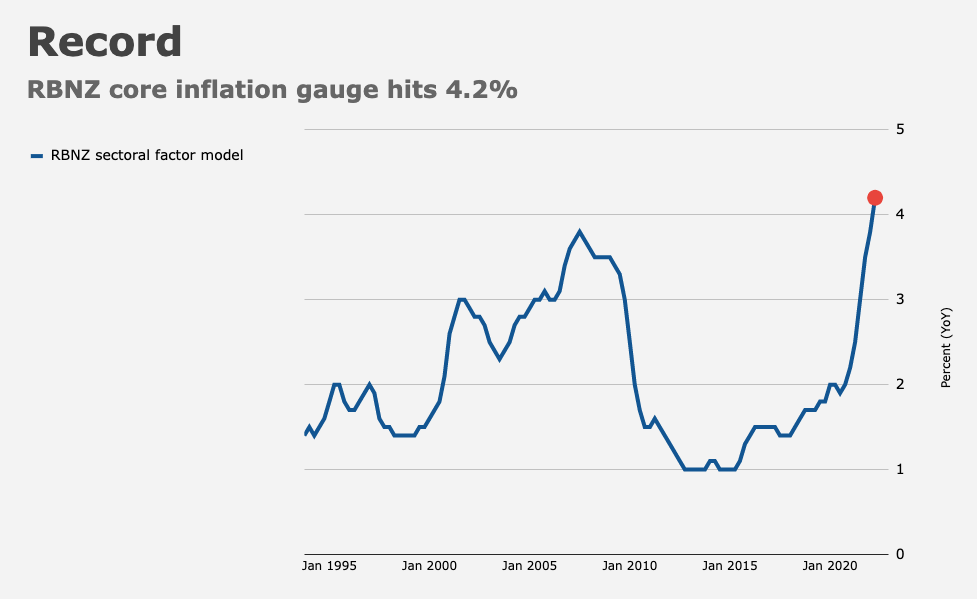

Currently, headline inflation is nowhere near the target in New Zealand, and even the bank’s own measures of core prices are at least one full percentage point above the top-end of the range. In a sign of the times, even the most proactive central banks are chasing inflation.

RBNZ’s “path of least regret,” as the bank called its aggressive approach, has succeeded in bringing the cash rate above neutral (figure below). Again: New Zealand is ahead of the game, but not ahead of the curve. Inflation is still very hot, but with rates now in restrictive territory, the bank is actively braking growth — in theory, anyway.

“GDP contracted modestly in the March 2022 quarter [but] these data remain volatile, with a catch-up in government spending and exports expected,” the bank remarked, adding that more tourism should buoy the hospitality sector. Household spending, RBNZ said, “has remained resilient despite a decline in consumer confidence.”

By the time RBNZ is done, the bank expects to get OCR all the way up to 4%, two full percentage points into restrictive territory and the highest of the post-financial crisis era. Whether that’s feasible (or not) is an open question.

“Despite the bank reiterating its hawkish message about more aggressive rate hikes, we see rising risks of a recalibration in the hawkish tone before the end of the year due to a falling housing market and worsening economic outlook,” ING said Wednesday.

The bank cited “near-term upside risk” to inflation and “emerging medium-term downside risks” to the economy. As ING alluded to, one of those downside risks is New Zealand’s property market. I talked a bit about the juxtaposition between RBNZ’s hiking campaign and the country’s housing bubble in May.

Housing accounts for around half of the assets of New Zealand households. Policymakers are walking a tightrope. There were no new forecasts (it wasn’t a quarterly meeting), but the statement contained the following passage:

Financial conditions have continued to tighten with mortgage rates rising in response to, and in anticipation of, increases to the Official Cash Rate. Asset prices, including house prices, continue to decline. Members agreed that the increase in mortgage interest rates will assist to bring house prices more in line with sustainable levels. The Committee also agreed that both high food and energy costs and rising mortgage interest rates will lead to more subdued household discretionary spending in coming quarters.

Central banks in all developed economies will watch New Zealand like a hawk (pun intended). It’s a lab experiment of sorts — a test case in aggressive monetary tightening juxtaposed with at least one potential domestic systemic imbalance (the housing market). A bad outcome wouldn’t spill over. It’s a tiny economy and it’s an island.

RBNZ expects to start cutting rates in Q2 of 2024. The plan is to free up around 200bps of countercyclical breathing room and begin easing from 4% in two year’s time. That’s probably optimistic. House prices fell 2.3% in the second quarter, data out earlier this month showed. It was the largest drop since February of 2009.

“As the downturn sets in, and with interest rates set to rise further, greater consideration is now being given to ‘how long and how far will this go,'” CoreLogic NZ Head of Research, Nick Goodall, said. He called housing affordability “thinly stretched” and noted that “with interest rates rising, not falling like in the late 2000s, it is difficult to foresee any respite for falling house prices in the near term.”

“How long and how far will this go,” is probably a good description of the global tightening impulse itself. Apropos, South Korea delivered its first 50bps hike since rates became the country’s primary policy tool decades ago. I’m not sure I’d call the pace “panicked,” but as the simple figure (below) shows, it’s brisk.

The BOK got an early start, but for an emerging market, they’re probably not moving fast enough considering the urgency with which DM policymakers are now tightening.

“There’s greater damage if the upward inflationary pressure grows further,” Governor Rhee Chang-yong said Wednesday, explaining the large move.

The risks are myriad. The percentage of household loans tied to market rates is the highest since 2014, for example. Nearly 80% of credit extended to households will be affected by rising rates.

And yet, the bank sees inflation running above 6% “for some time.” Given that, a step back down to 25bps increments on the way to a 3% terminal rate (at the high-end) could be wishful thinking. One analyst called the idea of 25bps hikes from Korea at a time when the Fed is moving in increments triple that size “naive.”

{kind=link}