“What if the curve has been right all along?” Deutsche Bank’s Aleksandar Kocic wondered, in a new note.

He was referring to front-end pricing for resolute Fed tightening and evidence to suggest the long-end is at least as worried about a policy-induced recession as it is spiraling inflation.

All too often in 2022, stocks have exhibited signs of being trapped in a “damned if you do, damned if you don’t” predicament.

Good economic news is bad news for risk assets because it suggests the amount of delivered tightening (measured either by reference to rate hikes or financial conditions) isn’t yet sufficient to cool the economy, and thus the Fed needs to do more.

But bad economic news is bad news too. Evidence of slower spending (for example) supports the recession narrative, but with inflation destined to remain materially above target for the foreseeable future, there’s no hope of an outright policy pivot, only an incrementally less hawkish Fed. And even that’s viewed with consternation because softer rhetoric could be indicative of higher downturn odds.

“[It’s] as if the market is always embracing the worst possible scenario, suggesting that a less hawkish Fed is synonymous with an incoming recession, rather than an adjustment to a more benign inflation,” Kocic wrote, in the same note.

The figure (below) speaks to the “more benign inflation” point. It shows the “other side,” as Kocic put it, of the recent spike in a neutral rate proxy. The decline in domestic equities occurred against a 160bps selloff in 2Y1Y reals since March. Over the same period, nominals were (basically) flat, which, as Kocic noted, entails “a pure compression of breakevens.”

Recent Fed rhetoric has stabilized (if you will) even if it hasn’t really softened (per se). The idea of a “Bostic pause” was news this week, and one of the more adventurous Fed calls on the Street was adjusted to reflect the same amount of overall tightening, but less aggressive front-loading. All of that’s consistent with the idea that lower stock prices, wider credit spreads, tentative evidence of a cooler housing market and deteriorating PMIs add up to diminished incentive for policymakers to deliver incremental hawkish escalations.

Between breakevens compression and the perception that the Fed is “getting what it wants” from markets and thereby feels less near-term pressure to keep dialing up the rhetoric, you’d expect stocks to stage a meaningful, sustained rally.

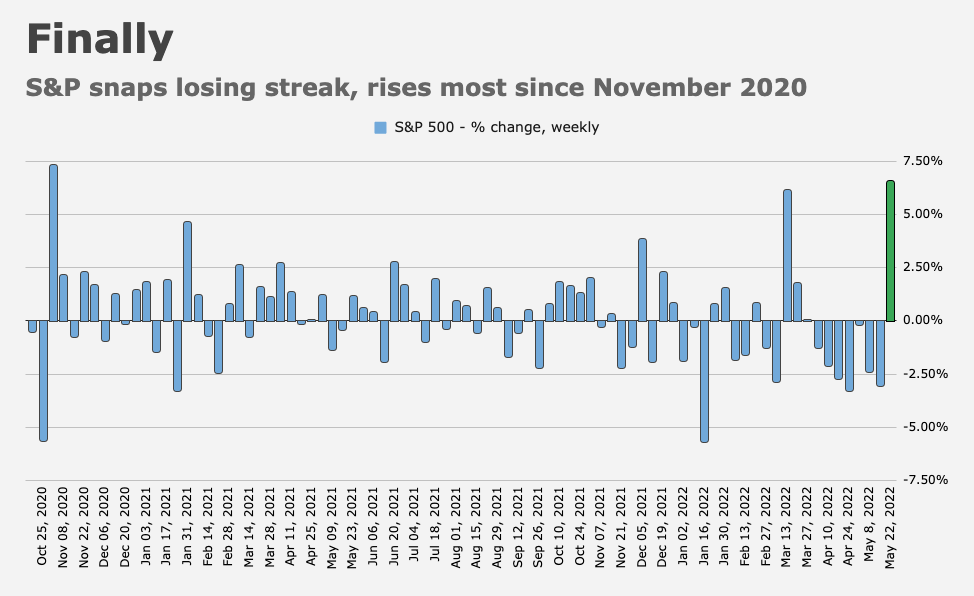

This week’s surge (the largest since November of 2020) was meaningful, but whether it’ll be sustained is another matter entirely. If it is, that’ll only incentivize the Fed to re-escalate, in an effort to avoid surrendering the progress they’ve made on the road to tighter financial conditions.

This is a circular dynamic, something Kocic underscored. “The problem is that real rates just became barely positive, and the market is already complaining — as if [they’ve] lost any tolerance for positive real rates,” he said. “Now that there are signs that aggressive hikes are less likely, the market is embracing the other extreme, the recession story, hoping to extort assurances about the Fed’s preparedness for further accommodation or at least some kind of guarantee of dovishness.”

{kind=link}

The “real world” is looking at food (e.g. wheat) shortages, energy disruptions, shutdowns in China, war, political divisions in many nations, climate change, mass shootings, etc. I have no idea how this will affect stocks but it is difficult for me to see inflation substantially decreasing over the next 12 months.