Most citizens in advanced economies aren’t accustomed to economic suffering.

That’s a generalization, of course. Every nation has some poverty, and there’s a case to be made that America has far too much of it considering the US is the richest nation in the history of the world.

A testament to that: America ranks inexcusably low on various lists of societal achievement including, unfortunately, childhood poverty (figure below).

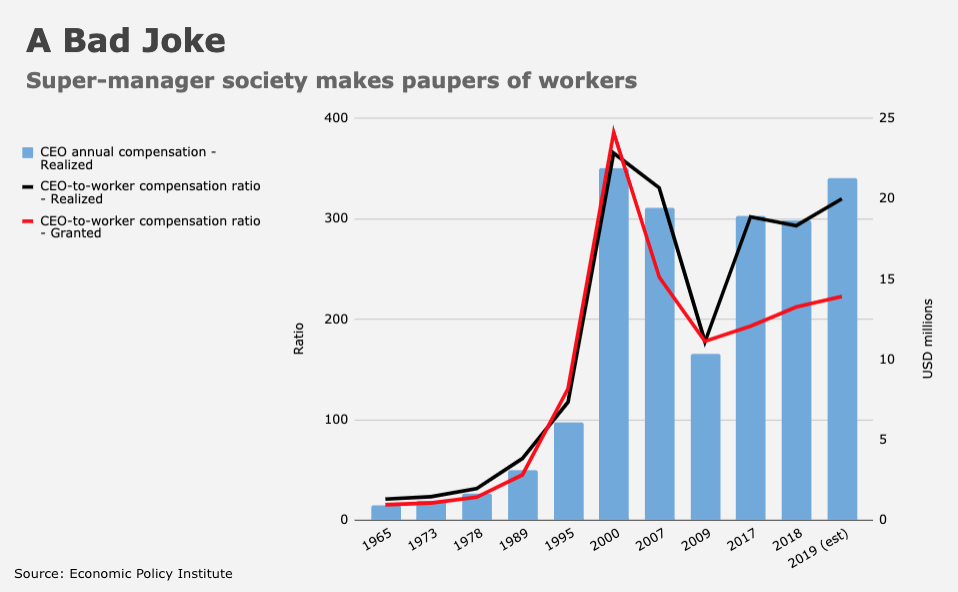

While it’s obvious that everyone can’t be rich (if everyone’s rich, no one’s rich), it’s equally obvious that American-style capitalism often produces suboptimal outcomes defined by egregious inequality that now borders on Belle Époque extremes, only instead of rentiers, America has super-managers.

The point is just that there’s a middle ground between a “welfare state” (in the derisive sense of the term) that disincentives work and thereby economic vibrancy, and a cartoonish hierarchy where nearly everyone is “poor” relative to a fraction of a fraction of the populace. The US has drifted further and further away from that middle ground over the past four decades, with increasingly dangerous consequences. Even the top 0.1% aren’t immune (figure below).

Spiraling inequality works until it doesn’t. People will tolerate being relatively poor, but if an exogenous shock comes along and renders too many people literally poor, the government is compelled to respond, lest a majority come to the conclusion that the social contract has been irreconcilably breached, freeing citizens from their obligation to respect the government’s monopoly on the use of coercive force.

In 2020, the US came very close to a tipping point. The majority of people were aggrieved, even if they couldn’t agree on what it was they were aggrieved about. The social fabric began to tear and that summer, the nation teetered on the brink of upheaval. Blinded by political, religious and racial divisions, Americans were unable to discern the tie that bound them together: Economic precarity.

Little wonder both political parties were keen to perpetuate the culture clash. If the shared nature of economic disadvantage ever dawns on Americans, the “swamp” will well and truly be “drained,” Wall Street won’t just be “occupied” and the super-managers won’t be making 300 times what the average worker makes for very much longer.

Steve Mnuchin, well acquainted with public reprobation associated with cartoonish displays of wealth, realized the imminent peril associated with the pandemic lockdowns. It was, according to some accounts anyway, Mnuchin who pushed hardest for a no-questions-asked, multi-trillion dollar rescue for the American public. He wasn’t a humanitarian. And he wasn’t just looking out for Donald Trump’s re-election bid. He was a realist. He could read the writing on the wall, and he didn’t like what it said. In mid-March of 2020, he warned Republicans of a 1930s-style meltdown if they refused to go all-in. One shudders to imagine what 2020 would’ve been like in the absence of the initial fiscal response to the first US COVID wave.

Why bring all of this up? Well, because developed economies are now poised to deploy new stimulus in an effort to blunt the impact of surging inflation as the war drives up the cost of food and fuel.

On Thursday, Germany’s ruling coalition decided on a €15 billion package aimed at ameliorating the impact of higher energy costs on households and businesses. In addition to cutting the fuel tax, Germany will also give taxpayers a one-time €300 payment and a €100 child support subsidy. In a bid to increase the appeal of public transportation, a €9 monthly ticket will be introduced.

Germany isn’t alone. On Wednesday, the UK announced a mini-budget aimed at tackling a “cost of living crisis,” but the pushback was telling. Rishi Sunak’s plan seemed opportunistic — designed to restore whatever’s left of his credibility as a proponent of lower taxes, as opposed to someone who’s concerned about the plight of the poor.

Missing from the plan was an increase in welfare payments commensurate with the surge in inflation. Specifically, benefits will increase by 3.1%, less than half of the 7.4% inflation is expected to average over the next year. In its March economic and fiscal outlook, the Office for Budget Responsibility said real household disposable income per person will drop by 2.2% in 2022-23, the biggest decline in any single financial year since ONS records began in 1956-57 (figure below).

“Higher energy prices and inflation as a result of a longer war in Ukraine or tougher international sanctions” could pile pressure on Sunak, OBR said, noting that the inflation-adjusted value of welfare benefits this year is expected to fall by 5%.

Meanwhile, back at the ranch, some US states are rushing to take action to offset the impact of higher prices. California, for example, is floating $400 debit cards to all car owners as gas prices rocket higher. You can expect many more such state- and local-level initiatives and no one should be surprised if Congress decides to deliver new stimulus too.

The pushback is predictable and it does have some merit, couched as it is in old adages and axioms: The cure for higher prices is higher prices, after all. There’s only so much consumers can take, so if prices rise too far, too fast, demand will disappear leading to lower prices. Problem solved!

Failing to observe that simple concept by, for example, sending people free money, will only forestall the inevitable by keeping demand artificially high, thereby driving prices higher still. Or so goes the pushback. We should just let the market work its “magic.”

This debate will be front and center going forward, and while I won’t pretend to settle it, what I’d suggest is that reality rarely cooperates with theory, even when the theory is sound. Perhaps the most poignant example is America’s $1.3 trillion student debt mountain. It’s probably not good policy to cancel all of it. It’s a slap in the face to everyone who paid their debt, it discourages personal responsibility and, most importantly, it lets everyone off the hook for perpetuating a system of perverse incentives that allowed the price of a college education to spiral inexorably higher in the first place.

But the reality is this: The vast majority of that debt will never be paid back. We can badger borrowers, threaten them, sue them, ruin their credit and even force them into bankruptcy, but it won’t change the fact that we simply saddled too many people with too much debt, and because that debt isn’t linked to something “current” or “necessary” (like, say, a mortgage or a car), it’s highly unlikely that most people are going to service it, especially if it would force them to divert money from something they have to have (again, like a house or a car).

When the collective decides it isn’t going to do something, or won’t tolerate a given scenario, discussions about what is or isn’t “good” policy become wholly irrelevant. Take mask mandates, for example. It’s unquestionably good public policy to require masks in crowded, indoor environments during a pandemic. But many Americans, in their infinite wisdom, decided that wearing a small face covering was somehow akin to desecrating Thomas Paine’s tombstone, so eventually, businesses just gave up on it — local, state and federal guidelines be damned.

Currently, Americans are staring at an inflation crisis akin to that witnessed nearly a half-century ago, but importantly, these aren’t the same Americans. These are Americans who won’t suffer even the slightest inconvenience in the interest of securing long run prosperity for the polity. The same can be said of other advanced economies, albeit to a lesser extent.

I personally don’t believe $7 gas or $8 bread or $10 milk or $9 packages of sliced turkey are things most people in advanced economies are prepared to accept. It’s all too easy to make the demand destruction argument when you can afford to pay $75 for a tank of gas on the way to Starbucks for a $15 custom latte which you’ll need to give you the energy necessary to navigate a short-staffed Kroger on a $250 grocery trip.

If that’s you, great. You’re fine, and you can wait it out, insisting all along the way that we need to let demand destruction run its course.

What you may want to consider, though, is the distinct possibility that middle-income families want gas, lattes and turkey too. They’ve been driving, caffeinating and feasting just like you have for the last 30 years, and they may not accept “No soup for you!” as an answer. Politicians are terrified of that possibility and are thus predisposed to obliging the masses.

It may well be that demand destruction is no longer a concept that’s politically viable in advanced economies. As we saw in 2020, the proverbial huddled masses are restless. They’ll accept a status quo that systematically oppresses them as long as you don’t require additional sacrifices of them, and as long as you subsidize the things they need when circumstances conspire to make everyday life too onerous for too many people.

The Saudi monarchy understands that concept all too well. Mnuchin understood it too. And anyone keen on keeping their place at (or near) the top of the social hierarchy in advanced economies would do well to learn it.

{kind=link}

Great piece. What does this mean for markets though!?

Markets won’t work when they don’t work. And they really won’t work in a revolution.

Agree w/Lucky. Well filed by H under Economy, not Markets or Politics.

Read a little Peter Turchin

The same old story writ large. We just can’t stop digging our hole because, as H has described time and again, not enough of us are willing to sacrifice for the greater good. The climate disaster happening before our blind eyes is going to bury us in that hole before long. As a species we really haven’t learned anything since our ancient relatives cut down the last tree on Easter island.

Mr. H

I appreciate your patience in allowing me to comment and pontificate.

I was fairly early in internet adoption back about 1994, it fit my nature of exploring infinite rabbit holes, including your burrow, which I think of as a stable jumping off point, a worm hole that gets me to other places, faster.

Seeing the Mnuchin name as part of a story immediately triggered my ingrained sixth sense esp alarm, sending me off in search of danger, or a unique connection.

I quickly reviewed his pandemic activity and ran across a sentence about the CARES Act that briefly touch on municipal bonds, a rabbit hole I generally avoid.

However, in our post pandemic recovery period, connected to the Ukraine invasion, the stuff I just stumbled across is very unsettling and I want to share this puzzle.

“In March 2020, investors pulled a record $45 billion from muni funds. Municipal bond prices dropped, and the yield on muni bonds rose sharply above the yield on comparable U.S. Treasuries.

In March 2020, the Federal Reserve made municipal securities eligible for its Commercial Paper Funding Facility (CPFF) (meaning the Fed was willing to buy short-term muni debt directly from state and local governments) and for the Money Market Mutual Fund Liquidity Facility (MMLF) ”

That connected to this:

“Volatility Returns in Muni Market’s Worst Quarter Since 1994

Benchmark yields saw biggest jump since April 2020 on Tuesday

State and local debt has lost 5.5% in 2022: Bloomberg indexes”

Which connected to a review of 1994 history @ wikipedia

“Some financial observers argued that the plummet in bond prices was triggered by the Federal Reserve’s decision to raise rates by 25 basis points in February, in a move to counter inflation.[4] At about $1.5 trillion in lost market value across the globe, the crash has been described as the worst financial event for bond investors since 1927.[1][5]”

Which connected to this from today:

“The ICE BofA Treasury Index has recorded its worst start to the year in history, down 6%.

..portfolio manager with the Swarthmore Group, said he had seen a “pretty big disconnect” on the short end of the U.S. Treasury curve earlier this month – in a reminder of the lack of liquidity seen in the aftermath of the global financial crisis.

“Bonds and credit are the lubricant for the economy, and when you get the short end drying up, that’s a very big warning sign for us,” he said.”

https://graphics.reuters.com/USA-MARKETS/BONDS/klvykjgmovg/chart.png

This seems like a fairly dangerous rabbit hole!

Thanks for connecting these dots. I’ve always wondered what was going on behind the curtain, and the consequences promoted by those actions.

Roughly speaking, UST yields from are up YTD

1M 9bp

3M 45bp

6M 75bp

1Y 116bp

2Y 175bp

5Y 133bp

7Y 111bp

10Y 94bp

20Y 81bp

Seems to me that

– Bond market believes Fed will tighten more or less 200bp

– Bond market doesn’t believe outyear growth will stay good

– Bond market doesn’t believe outyear inflation will stay high

I guess we’ll get a better read on what the bond market believes in the interregnum between QE and QT.

Jyl,

I always was fascinated by bonds but never saw them as providing a decent return. I hate to be somewhat off topic but had a few more tidbits to toss out.

It seems like bonds are almost mirroring the early pandemic chaos with simultaneous supply and demand friction, with municipal stuff flooded with too much supply and no demand, while in other spaces it’s reversed. It’s like the normal inverse relationship functions are misbehaving. The issues of duration and convexity, which are usually complicated are now totally in new virgin territory.

Here’s an interesting inflation context:

“Derivatives-like instruments known as fixings imply that the headline, year-over-year consumer-price index gain for March and April will be 8.6%, up from a 40-year high of 7.9% in February. Only the March reading will be available to Fed officials by the time of their May 3-4 meeting; April’s data isn’t set to be released until the following week.”

H is making a good case for universal basic income. The smartest policy to help folks out in situations like this is to help on the broad income side. By not subsidizing scarce goods but helping people pay for expenses at least relative prices are not distorted too much. So your gasoline, heating and electric bills went up $250 a month? So here is a $250 subsidy per month directly- if you conserve energy you pocket the difference- or if you want spend it on the higher gasoline, heating and electricity. Other goods of course may go up in price because of transport costs. But you get the general idea. If you want to reduce excise taxes a little to help out energy intensive users a little more- that is ok to a limited extent I suppose. Arguably folks in Wyoming probably spend more on gasoline than oh say Manhattan, NY. Help folks out but do not distort relative prices as much as possible. And per the story, perhaps you put an income cap of 400 or 500k on the income aid. BSDs don’t need the subsidies anyway.

State and local systems and budgets probably can’t handle it, but in principle gas, electricity, and sales taxes (on food stamp eligible goods) could be flexed up and down to respond to episodes like this.

After everything Mnuch has seen and properly survived he is placing his bets on cyber security these days.