Markets are awake to the idea that the Fed may be on the brink of tightening into a slowdown.

Growth concerns are proliferating, and some strategists are openly cautious about the outlook for US equities as economic momentum wanes at a time when the Fed has all but pre-committed to waging a two-pronged assault on inflation through multiple rate hikes and simultaneous balance sheet rundown.

The question is: What happens to the Fed’s battle plan in the event the economy rolls over?

“Tightening cycles are usually funded by growth — there has to be enough growth to allow rate hikes that would not derail the economy, just prevent it from overheating,” Deutsche Bank’s Aleksandar Kocic wrote, in his latest missive.

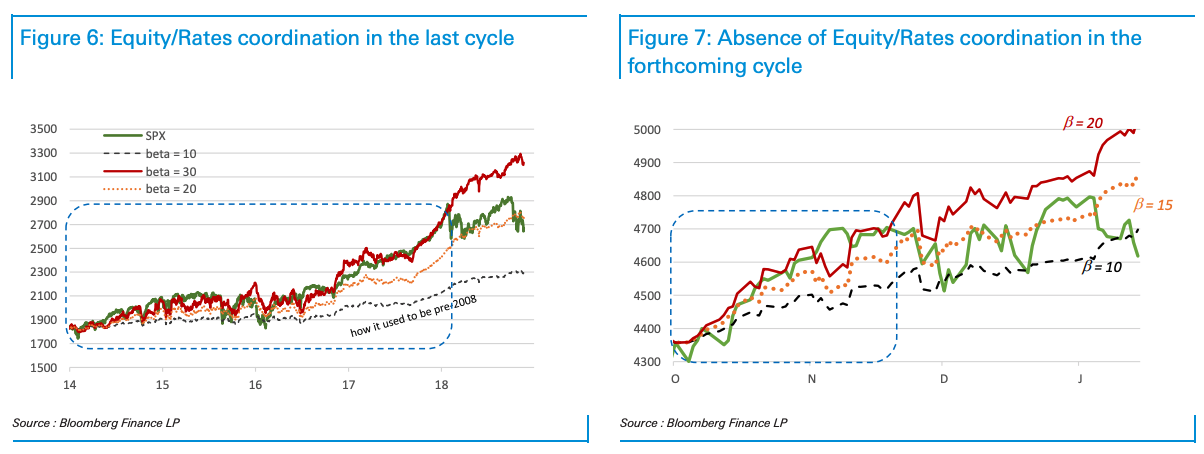

Consensus has coalesced around the idea that the vaunted Fed put is now struck much lower thanks to bipartisan support for tighter monetary policy in the face of the hottest inflation in 40 years. The last time the Fed put was re-struck, in 2018, Kocic suggested on multiple occasions throughout the year that the S&P would likely end up somewhere between 2,300 and 2,400, which is precisely what happened thanks to the worst December for the US benchmark since the Great Depression.

The red line in the figures (below) corresponds to the most protective Fed policy, a path stocks largely followed until 2018. The figure on the right uses the same parameters to illustrate how things have developed over the past several months.

“There is noticeably higher dispersion between equities and rates paths,” Kocic wrote. “While the S&P started along the highly protective (beta = 20) path, it quickly declined to the lower beta trajectories and is currently meandering around the pre-2008 path.”

The idea of a Fed put certainly existed prior to Lehman, but as Kocic noted, its “significance figured much less prominently.”

From the financial crisis through 2016, fiscal policy was relatively tight and inflation subdued, which gave the Fed wide latitude to cater to markets while gradually stepping away from accommodation. Now, things are different. The US fired a fiscal bazooka at the pandemic in 2020, and although the fiscal impulse is set to wane this year, the effects on demand will linger at least for a few months. At the same time, the supply side is still hopelessly distorted.

And yet, for all the hand-wringing over inflation, and notwithstanding the dramatic rebound in the economy, questions abound. “Despite seemingly encouraging economic numbers, there are strong headwinds against a complete rebound of demand with declines in immigration, early retirements, different migration patterns and declines in labor participation all contributing to a somewhat incomplete, or at least uncertain, growth recovery path,” Kocic went on to say.

In short, it’s impossible to have anything like a “base case” for the US economy. We’re all compelled to say we have a base case. But really, everyone is (still) flying blind.

When it comes to the interplay between monetary policy and stocks, the key question, Kocic wrote, is this: “Is there enough demand to fund aggressive rate hikes if high inflation persists?” And then, “At what price?”

Those questions will remain unanswered, at least in the near-term, which Deutsche Bank suggested may manifest in a bid for long-dated rates vol and equity puts.

“If the Fed’s hands are tied — if they cannot hike effectively against incoming inflation — then both bonds and risk assets could be forced to sell off,” Kocic said.

{kind=link}

Got Narcan?

“Tightening cycles are usually funded by growth — there has to be enough growth to allow rate hikes that would not derail the economy, just prevent it from overheating,”

Gosh it sure seems like LAST YEAR would a have been an ideal time to execute rate hikes. But I wonder if a certain former president’s twitter bully pulpit scared Powell out of doing what he should have done? Regardless he’s either gotta live with the fact he’s driving us towards stagflation or that he has to change course and accept permanent inflation. Not a great place to be in.

Inflation may be first and foremost a monetary issue (paraphrasing) but the response to inflation is first and foremost a political one. In this midterm election year, politics will dictate government action even more than usual.

For Republicans, inflation is a political weapon against Democrats, wealth redistribution, climate efforts, and anything else that can be fit into the PR sausage machine. The Democrats will be forced to “do something, do anything, do everything!” against inflation, even at the cost of slowing the economy. The Fed’s independence is at its lowest when members are being appointed, and it has its own institutional biases and credibility stakes.

Looking to the Fed for rescue anytime soon overlooks that the Fed considers very high inflation a greater threat to the economy and to itself than a bear market. Bear markets are not good but there have been many such in the last 50 years; there has been very high inflation once and no-one wants that on their CV.

In my view, it no longer matters what the root cause of the current inflation is, whether Fed tools can address it, or if inflation will recede naturally in 2H22 – none of that will determine Fed action in 1H22.

The psychoanalytic take then is: Powell hikes to solidify his self’s desired legacy as a inflationary dragon slayer of Volckerian stature?

Was couching the PR apparatus as a “sausage” machine one of those Freudian pratfalls?

There are two things many folks miss that has changed. Demographics and economic structure have changed in the US which leads to different short term and longer term results. Our population growth is slower and our population is older- leading to slower growth built in. Our economy overall has much higher leverage than even 5 years ago. That is in the corporate and public sector. This means that a relatively small increase in interest rates has an outsized effect. That coupled with challenging demographics means that the economy’s baseline growth rate is low. That, and the supply chain problems are why we have seen a yo yo in growth and inflation the last two years. The FOMC can project 3 or 4 hikes and a shrinking balance sheet with their (foolish) dot plots. But where the rubber meets the road, likely will see fewer moves to tighten. The economic backdrop is too fragile. Does that mean they do nothing? Of course not. Tapering purchases make sense, and so does lift off. But all the talk of many and quick hikes and shrinking the balance sheet- bad idea. A prudent course would be to taper, maybe hike once and then see what happens. If it works and things are still on a high growth plus inflation path- go ahead hike again. But if not slow down and wait. This is a great instance where a cautious approach makes sense. The balance sheet seems to be an obsession with some. Remember why it was increased. The US Treasury market ceased to function. The dealer community no longer provides a buffer of liquidity. The Fed now does and for good reason. If they don’t the market seizes up. So the excess liquidity is there for a reason. Leave it alone.

A sensible assessment. Not an opinion that would support a lot of “likes” or a rise in newsmedia ratings, but sensible nevertheless. Real economic growth of 2% is about as good as we can expect going forward when current birthrates won’t produce a population increase. If we want growth we will need a rise in immigration and a ten year GOP “quiet period.”

I expect near “read the riot act” jawboning tomorrow from statement and Powell with result of market selloff over 1-2 weeks, thereby emulating tightening conditions, maybe a liftoff next meeting and at most one more hike after that, then pause until 2023…

…agree also with previous commenters, would only add that “bazooka” does not do justice to the financial bombardment of markets since 2020…

oh … and if 10 year rates hit, approach, or exceed 2.25% … I’ll very likely allocate to TLT and EDV given debt and demographic circumstances…