The US data calendar is sparse in what’ll be a holiday-shortened week dominated by Fed speculation.

At this point, a March hike is a foregone conclusion and market participants of all sorts (so, not just Bill Ackman) are beginning to seriously ponder the prospect of a surprise, either in the form of a 50bps move or even a hike at this month’s meeting.

The latter seems exceptionally unlikely, especially considering the pre-FOMC blackout period leaves officials with no opportunity to signal the market. A larger move in March is now conceivable, though.

“Demand for April eurodollar options — the first tenor to expire after the March FOMC meeting — has been seen over the US morning session, hedging a scenario that the Fed will hike 50bps [in] March,” Edward Bolingbroke noted Friday.

US equities are, of course, coming off a two-week losing streak (figure below).

The S&P is down 2% already in 2022. (Just 98% to go.)

With rates front and center, style-, factor- thematic- concerns will remain topical. “Our current recommended sector overweights reflect a barbell of Growth and Value,” Goldman’s David Kostin wrote.

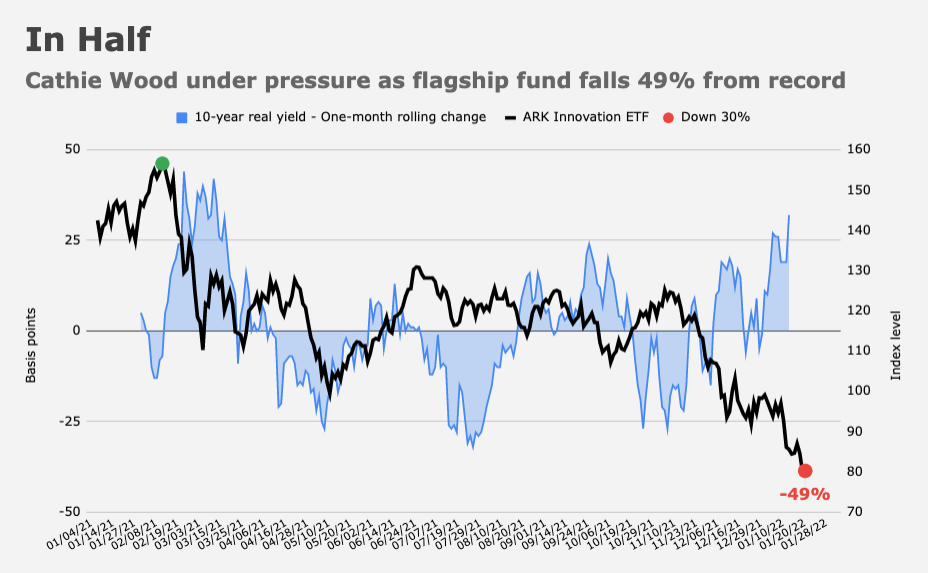

Info Tech is the bank’s “long-standing overweight due to its secular growth and strong profit margins,” Kostin went on to say, before cautioning that investors should “own highly profitable growth stocks relative to growth stocks with low or no profitability.” Profitless hyper-growth is the last place you want to be in an environment where yields are rising led by real rates. Just ask Cathie Wood.

“Financials should benefit from rising interest rates, while Health Care combines secular growth qualities with a deep relative valuation discount,” Kostin remarked.

Financials enjoyed their largest inflow since November of 2016 in the week leading up to reporting season (figure above).

The problem with bank shares, though, is that they’ve run pretty far, pretty fast. In fact, the KBW Bank Index was up nearly 12% YTD headed into earnings.

Judging by results from JPMorgan and Citi, Wall Street’s traders underwhelmed last quarter. And expenses are rising.

JPMorgan had its worst day since 2020 on Friday (figure above). Goldman, Morgan and Bank of America will all report in the days ahead.

Coming back to the Fed, Jerome Powell will need to confirm liftoff is a go for March later this month. And while excessive forward guidance is part and parcel of post-Lehman Fed policy, tied hands aren’t. “The Fed’s traditional reluctance to forward commit to any further monetary policy moves will be met by the practical constraints of needing to appropriately signal to the market that a quarter point hike will be in the offing at the end of Q1,” BMO’s Ian Lyngen and Ben Jeffery said.

Responding to Powell’s “it’s really time” soundbite from the Q&A portion of his confirmation hearing, TD pulled forward their expectations for liftoff and balance sheet runoff. “We now expect a first rate hike in March, instead of June,” the bank’s Jim O’Sullivan and Priya Misra said. “As before, we expect Fed tightening actions to continue on a quarterly basis after the first move through the end of 2023, with one of those actions being the start of QT rather than a rate hike, but we are also changing our QT call to make it the third move (after two rate hikes) rather than the fourth move (after three hikes).”

Again, a “shock” move this month isn’t anyone’s base case. And no one (that I’m aware of anyway) has 50bps penciled in for March either. But the rapidity of the policy pivot (and ceremonial adjustments to banks’ house Fed calls) is a reminder of how quickly things can change.

For stocks, the next move is anyone’s guess. “Lower bond yields and QE have been the argument for higher equity valuations for some time now, so the fact that a reversing of the process is having the opposite effect seems logical,” SocGen’s Andrew Lapthorne wrote, in his latest.

“While many argue that profit growth is supportive, the bulk of that growth recently has been from cyclicals and not growth sectors,” Lapthorne observed.

Everyone expects cyclical value to outperform. If you’re looking to fade the consensus view, that’s it.

The data docket in the US this week includes Empire and Philly Fed surveys and housing numbers. Oh, and ham prices rose 54% in a single day last week. As Bloomberg’s Michael Hirtzer put it, “Want to buy a ham? You better bring home the bacon.”

{kind=link}

H-Man, the Fed can signal in January when the black-out ends and they start talking with almost 45 days before the March meeting. If we get another hot print on inflation in February, they will be chattering. They have read the Kaufman/Ackman comments so don’t rule out a surprise. The signal will be the chatter.

Talking about bringing home the bacon: Here is the whole butcher shop – buy MLFNF

Hirtzer writes, “Higher ham prices are also boosting hog futures.” Pretty sure that’s not how the pigs would see it.

Scary movie afficionados will definitely want to be live on Powell’s next press conference…

The Fed Put is gone. Wile E. Coyote hasn’t seen the abyss yet. Goldman is out there pumping and offloading stocks as they are wont to do when they see the looming crash.

I’m keeping an eye on retail traders inflows. We’re usually the bag holders. Once inflows become outflows I’m loading up on Tesla puts.