I’d call it a testament to rampant uncertainty, but it’s probably more accurate to say markets are more noise than signal currently.

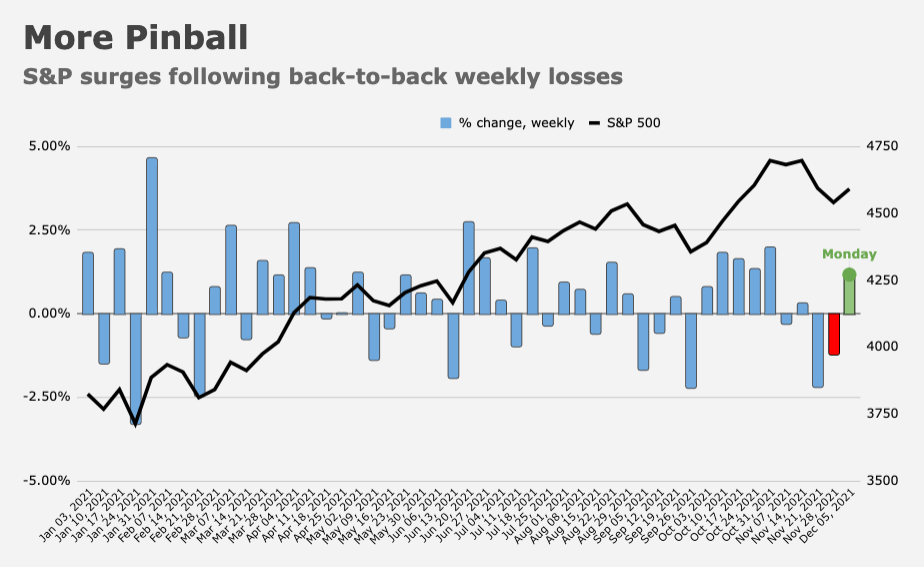

US equities kicked off the new week by erasing last week’s losses (figure below), while Treasurys sold off enough to negate Friday’s rally. Monday was, in a word, absurd.

There was nothing in the way of clarity around Omicron and China’s RRR cut doesn’t move any needles. Divination from the price action is very difficult given the proximity of year-end, to say nothing of the myriad ambiguities around the new variant. US inflation data is on deck, but not until week’s end.

Daily market wraps were full of “we expect volatility to continue” soundbites.

It’s worth noting, though, that on the heels of the latest Fed-inspired vol expansion, it likely won’t be long before the same Pavlovian response function that prompted retail investors to buy recent dips compels vol-sellers to reengage. And that matters.

“The fact is, with VIX spot ref 30, the S&P really needs to sustainably move more than 1.5% a day (frankly, closer to 1.8ish%), or else VIX is going to collapse under its own weight and mean-revert lower as it always does, thanks to reflexive vol-sellers shorting ‘rich’ vol as a buy-the-dip expression and downside hedge monetizers taking profits as a selloff realizes, both of which create Delta to buy,” Nomura’s Charlie McElligott said Monday, adding that the market is “really hedged.”

The read-through is that assuming spot doesn’t careen lower through systematic sell triggers, those hedges could end up being rally fuel. At the same time, vol control has already shed nearly $57 billion in exposure in just two weeks. If equities can go a few days without logging outsized moves, realized can calm down, dictating mechanical re-allocation on a lag. However, as McElligott went on to say Monday, “if we keep realizing this 1.5%-2.0% area being implied, there’s still hell to rain down — read, lots more $ selling.”

Rates, meanwhile, are still a rollercoaster. As noted above, yields were cheaper by some 9bps Monday, wiping away Friday’s rally in a bout of bear steepening at odds with the entrenched (and, some would say, impossible-to-fade) flattener.

Admittedly, there was plenty of justification for the move. In addition to a heavy corporate slate and the voracious bid for risk, supply looms. “This week’s $112 billion in Treasury coupon[s] has seen a mild set up but that doesn’t ensure a smooth auction process,” Bloomberg’s Alyce Andres wrote. “Recent auctions have been sloppy given Street risk limits and pain among the hedge fund community [which] bodes well for more of a price concession.”

Plausible rationales notwithstanding, it all feels a bit haphazard — like markets still haven’t quite settled on a narrative following last week’s fireworks. More near-term pinball seems inevitable.

“The adverse effects of excessive hawkishness and the mode of policy mistake that’s causing the current twisting of the curve, if it persists and becomes a consensus, are likely to propagate into risk assets,” Deutsche Bank’s Aleksandar Kocic said. “We believe a further selloff of the front end is likely to trigger a stock market correction.”

H-Man, I agree the herd is running in circles waiting for that guiding light.