The Chinese economy decelerated in the third quarter, data out Monday confirmed, validating a chorus of analyst downgrades and underscoring the impact of multiple overlapping crises.

Although widely expected and well telegraphed, China’s slowdown casts a long shadow. The specter of “peak growth” haunts the global economy and is an obsession of sorts for market participants at a time when Western policymakers are keen to roll back emergency stimulus and otherwise tighten policy in the face of persistent price pressures.

The world’s second-largest economy expanded 4.9% YoY in Q3, short of consensus (figure below). On a sequential, seasonally adjusted basis, growth essentially flatlined.

The market may take the numbers in stride, perhaps comforted by a reasonably upbeat read on consumption.

Key activity data for September, released concurrently with Q3 GDP, showed retail sales rose 4.4% YoY last month (figure below). Consensus expected a 3.5% increase.

Domestic demand is a pressing concern. Data for August betrayed a steep decline in the pace of retail sales growth, an unwelcome development that spoke to a number of dynamics simultaneously.

Both the official and Caixin services PMIs fell below the 50 demarcation line for the first time since February 2020 in August, before rebounding in September, when the official manufacturing gauge dipped into contraction territory (figure below).

The deceleration in factory activity amid the energy crisis put the spotlight on industrial output, which rose 3.1% YoY in September, Monday’s data deluge showed. That was less than the 3.8% the market anticipated.

A 7.3% increase in fixed asset investment was also a miss. Consensus wanted 7.8%. The surveyed jobless rate moved lower to 4.9% from 5.1%. Home sales dove 17%.

Although exports are buoyed by robust global demand tied to re-openings and holiday pull-forward, factories can’t produce if they can’t operate. And property sales are likely to be depressed given poor sentiment engendered by Evergrande.

Officials in Beijing are adamant about their capacity to manage what it’s fair to characterize as an engineered slowdown. But ongoing efforts to squeeze the property sector (the world’s largest asset class) alongside the most aggressive regulatory crackdown in recent memory, suggest the risk of an accident is elevated.

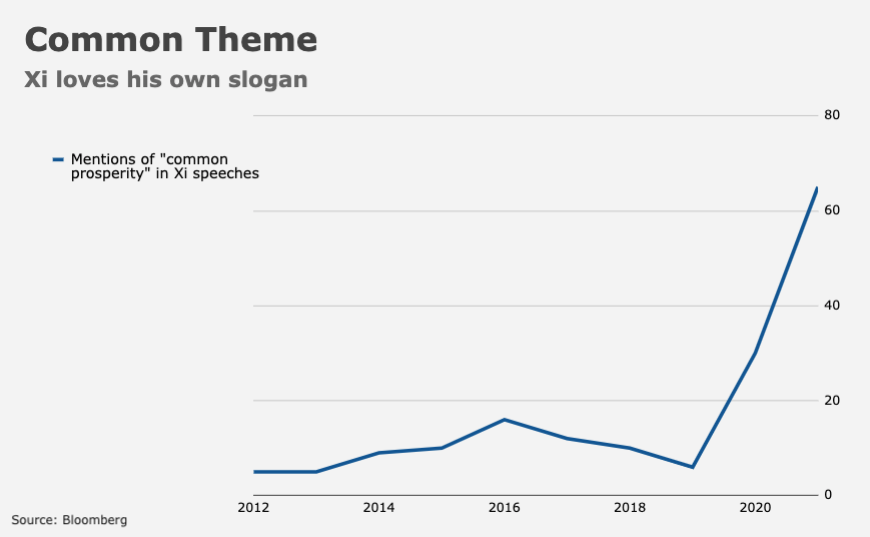

In addition to the property curbs, the regulatory crackdown, the power crunch and uncertainty created by the ambiguity inherent in Xi’s nebulous “common prosperity” catchphrase, the Chinese economy is at risk from new COVID outbreaks. Beijing hasn’t abandoned its “zero tolerance” policy towards the virus, which means any sizable flare-up (indeed, any single case) is treated with the kind of urgency one might expect around an Ebola outbreak. Maybe that’s the correct way to think about virus containment, maybe it’s not. But it’s certainly not conducive to economic activity.

Somehow, “mounting headwinds” seems woefully inadequate when it comes to conveying the scope of the challenge. Much of the damage is self-inflicted. Arguably, policies aimed at curbing excesses in the property sector, reining in tech monopolies, streamlining regulations, putting the brakes on spiraling inequality and pursuing environmental goals at the expense of near-term growth, are necessary and conducive to long run stability.

Still, one can’t help but wonder if there’s a threshold beyond which the combined drag becomes unmanageable. And not necessarily because the Party isn’t adept at precarious juggling acts. Rather, simply because it isn’t possible to map, let alone plan for, every contingency in a situation where the presence of multiple overlapping crises means the number of hypothetical macro permutations is virtually limitless.

{kind=link}

Or maybe they couldn’t keep the false growth trajectory going. We can’t really know how accurate data out of China is and official/state data should be considered more propaganda straight out of the Ministry of Plenty than actual information. We do know they have over built with estimates of empty buildings ranging from 20-40%. How good are those numbers? It is also believed that China’s population has peaked and is currently in decline. No country with a declining population has ever had 4%+ GDP growth. The caveat being for China, as an emerging economy, the real calculation needs to be growth of the consumer class with previous non-consumers (agrarian peasants) being converted to consumers means the consumer base can still be growing as the converts can offset the decline in overall population. But how long until the economy matures and runs out of peasants to convert? Has it already? There’s a 90% chance that the Chinese real estate bubble is the cause of the next GFC. It’s just a question of when, how bad, and for how long. 100 years ago, the US was the global supply of cheap labor. The faltering of this dominant emerging market economy’s stock market spun the whole world into economic crisis. For now though, there’s nothing to worry about so let’s all enjoy TINA while we can.

If China takes Taiwan (per capita GDP of $28,358 vs. China per capita GDP of $$10,511), China would get a one time boost to per capita GDP of 2.8%.

Ugh, yeah. Good point. But that would push us further down the road towards WWIII mapping very closely to the geo politics of early 20th century. We could equate it to the Japanese invasion of Manchuria.

Can you talk about how (in)accurate the data is and contrast with the economic data coming out of the US/developed economies? There is bad data “on both sides” but would really enjoy hearing your thoughts on the matter.