“Different day, same concerns.” That was the vibe on Tuesday as traders and investors (two distinct classes of market participants without much overlap) anxiously awaited a bevy of key data and earnings out of the US.

Maybe it’s just me, but every, single day seems like an “out of the frying pan, into the fire” day. That’s probably a consequence of the manic, 24-7 news cycle. There’s always a story. And bad news sells. If there’s no overtly bad news, media outlets will settle for something potentially ominous.

News that Beijing is formally launching a new anti-graft probe into the financial sector didn’t help sentiment, although a new round of checks at regulators and state banks is probably low on the list when it comes to market concerns around China.

German investor confidence appeared to take a hit from ongoing supply chain problems and associated shortages and price pressures. ZEW expectations dropped to 22.3 in October, the worst print since the onset of the pandemic (figure below).

“The economic outlook for the German economy has dimmed noticeably,” ZEW President Achim Wambach said, in a press release, attributing another monthly decline to “the persisting supply bottlenecks for raw materials and intermediate products.”

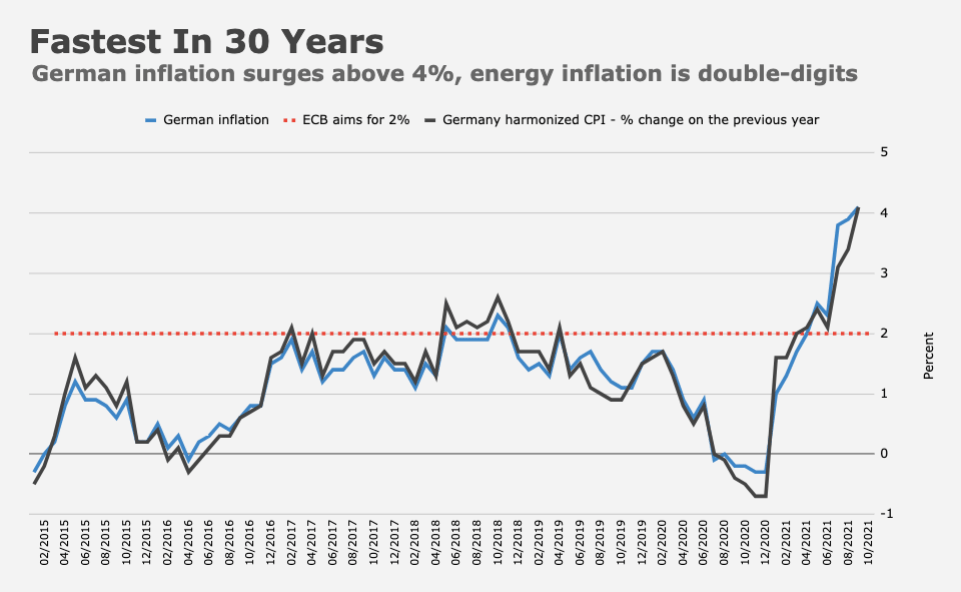

I suppose I’m compelled to mention the surge in German inflation and associated wheelbarrow jokes.

Price pressures are the most acute in three decades (figure above). We’re a long way from Weimar, though.

Speaking of inflation, the five-year, five-year forward rate in the US is near 250bps again (figure below). It’s been a while since the gauge has moved above that level and stayed there.

“Like everything else — and this is not a mere coincidence — current inflation numbers are at the point of maximum ambiguity,” Deutsche Bank’s Aleksandar Kocic wrote late last week, noting that history “can be divided into roughly two regimes, conditionally labeled as high and low inflation, with boundary around 2.50%, precisely where we are now.”

Pressure on the Fed to act has grown over the past several weeks as surveys of consumer sentiment (including the New York Fed’s own poll) show expectations becoming slightly unmoored, even over longer horizons.

Meanwhile, the energy crunch which sent gas prices spiraling higher in Europe with knock-on effects for crude, only adds to concerns. Of course, the prospect of demand destruction and so-called “fiscal failure” in Washington make the case that inflation worries will eventually ebb, even as labor market imbalances and acute supply chain frictions put upward pressure on wages and keep input prices sticky.

All of this presents central banks with a quandary: Tighten to preempt inflation pressures at the risk of exacerbating a burgeoning slowdown or remain accommodative at the risk of seeing prices spiral, aided and abetted by easy money.

“The global economy is on a collision course with stagflation [which] is threatening to upend central banks’ transitory inflation narrative,” PVM’s Stephen Brennock said. “Rising inflationary pressures could pose headwinds to growth and as a result oil demand,” he went on to write, adding that “it presents a key downside risk for the global economy and must be managed to prevent it from becoming permanently embedded.”

There’s a narrative out there that says central banks are “rushing” to tighten. It’s overblown, to say the least. It’s certainly true that policymakers are aware of the cat calls, and the BOE has been keen to project its own consternation, which is in turn emboldening traders to price in tighter policy. The Norges Bank hiked, so did RBNZ and some QE programs are being wound down.

Read more: Fly Hawks, Fly

But let’s not overstate the case. Norway has always been a hawkish outlier. The RBNZ hike this month was just August’s aborted hike on a delay (the bank was poised to hike two months ago, but didn’t due to a snap lockdown). And the BOE faces a set of unique circumstances.

“If 2020 will be remembered for all the wrong reasons surrounding global health, 2021 may go down as a year where select central banks rolled up their sleeves and showed that trading rates can be a two-way street,” Bloomberg’s Ven Ram wrote Tuesday.

Forgive me, but I kinda doubt it. Or at least as stated. In addition to my long-held contention that central banks (the largest of them anyway) will never truly be able to normalize policy, it won’t take markets long to internalize the potential ramifications of any overt hawkish turn in a world where it’s far from clear that the rebound in demand is durable/sustainable.

For evidence of that, look no further than sterling. Vassilis Karamanis, an FX and rates strategist who writes for Bloomberg, got it right. “The latest communication from [BOE] officials is quite hawkish and investors simply pencil in what’s asked from them,” he said, adding that “the thing with the pound is that the more rate hikes are priced in, the flatter cable volatility skew gets as longer-term bets look for pound weakness. Stagflation concerns anyone?”

{kind=link}

The second to last paragraph is key. I like it because… who doesn’t like confirmation bias?

Plus, the central bank is not completely aligned with our interests. Don’t they secretly desire some inflation to repay debt with relatively “cheaper” USD? Won’t they just let inflation go right up to the point (or maybe just passed it) they have to raise interest rates above inflation rates?

It certainly does feel like the economy is headed for stagnation and so keeping the easy money flowing is only delaying the inevitable. Why compound the problem by intentionally adding inflation to the mix?

Also, I am reminded of how you pointed out the lunacy of keeping monetary easing going during a red hot economy just to prop up GDP numbers. That feels prescient now.

I’ve been saying for 2+ years, “This feels like the 70’s is happening again.”

Inflation is necessary to pay old debts, Hamilton figured that one out.

And like the ’70’s, the growth is in technology, property and maybe TIPS.

The Fed is bound to repeat what happened during that period of (let’s keep it clean) disarray.

We are not in the 70s. Extrapolating now to be like the 70s will turn out to be an error. There are too many large differences in underlying conditions. Supply is disrupted and the Fed or other central bank policy is not going to solve this one way or the other. Time will be the market’s friend here. But we probably have to suffer for another 9-18 months first.

Spot on RIA. A big difference is that private sector unions were a lot more ubiquitous and powerful. That was a good inflationary transmission vector, along with COLAs in wages and benefits. Starting with Reagan, rightwing politicians put a stop to all of that nonsense!

I would add that population growth dynamics was much more favorable in the 70’s as well as lack of consumer indebtedness compared to today…

This environment has more flux, uncertainty, and silly chaos than I’ve seen in a while. Case in point: Jamie Dimon said today “the economy is great, the consumer is spending 20% more”. Well, that’s nonsense if it’s false and horrifying if it’s true. Consumers generally can’t just spend 20% more, suddenly, when their savings rate is under 10%, so it’s likely not real… but it if it is somehow true (stimulus, etc) then it means that vast chunks of GDP have already been unsustainably pulled forward and Jamie’s cheerleading just as we dive into the resultant air pocket.

At any rate, markets and the Fed seem to standing here with one foot on an inflection point and the other on a landmine. For the Fed, consider that it is quite possible for all policy choices to be “erroneous”, meaning, that economic outcomes tomorrow are worse than today no matter what path they pursue. The probability of policy error can be 100% if you’ve picked your historical venue unwisely 😉 Bullard this evening identified where he thinks our next step should land (“things are so great we should get that taper done pronto”). Pretty sure that step puts us on one of the landmines. You can tell, because a fast taper is a violation of the Heisenberg Certainty Principle (to wit: “I am certain that central banks can Never normalize again. Like, ever!”). Cheers!

+1

Bullard is not a man set in his opinions. I jokeingly call him Mr. Weathervane, though in recent years the humor of it has faded.

When is he due to be a voting member again?

This theme / debate resonates with me. An article yesterday in the Globe & Mail references Morgan Stanley/Andrew Sheets’ take on the 1970’s inflation parallels:

Many people who lived through the Great Depression remained frugal and fearful about bank solvency for the remainder of their lives. The generation that experienced the inflation of the 1970s were similarly scarred, constantly on the lookout for sharply rising prices and spiking mortgage rates.

Inflation-related paranoia is common in financial media headlines at the moment as the combination of supply chain tensions and the rising demand from post-pandemic economic recoveries pushes prices higher. Thankfully, Morgan Stanley strategist Andrew Sheets argues convincingly that a 1970s-style upward wage-price spiral is highly unlikely.

Mr. Sheets pointed out in a note earlier this week that the 1970s was a period of rising wages but also high unemployment, whereas now unemployment rates are falling quickly around the globe. In terms of asset prices, the current market features high stock valuations and interest rates near all-time lows, the reverse of the ‘70s.

Morgan Stanley sees the market now as more analogous to the 2004-05 period when stagflation – low growth and rising prices – was also a widespread concern. Then, manufacturing activity had started to decline while energy prices pushed inflation data higher. By mid-2005, manufacturing activity was close to registering month over month contractions while the U.S. consumer price index was climbing at an annual rate of 3.5 per cent.

Equities were volatile in 2005 with price-to-earnings ratios falling generally, but economic growth eventually resumed (at least until the financial crisis) and stagflation fears proved unfounded.

Although a skeptic regarding stagflation, Mr. Sheets remains bullish on energy prices in the coming years. He cites the work of his colleague, commodity strategist Martijn Rats, who believes that futures prices are understating energy prices, which are likely to stay elevated for the foreseeable future.

In general, however, Mr. Sheets does not think the 1970s-style stagflation story is anything like a useful guide for investors. “The 1970s are a long way away from our expectations or market pricing,” he writes. “Scenarios of slowing growth and rising inflation clash with our global forecasts of the opposite. Recent moves in inflation expectations and [manufacturing data] don’t fit the story as nicely as one would like.”