Traders will have plenty of data to digest in the new week.

A second consecutive lackluster read on hiring in the world’s largest economy was accompanied by further evidence of labor market friction and, relatedly, additional signs of wage pressure.

Leisure and hospitality hiring underwhelmed again. Apparently, workers want more money to reengage in pandemic-exposed sectors (figure below). Imagine that.

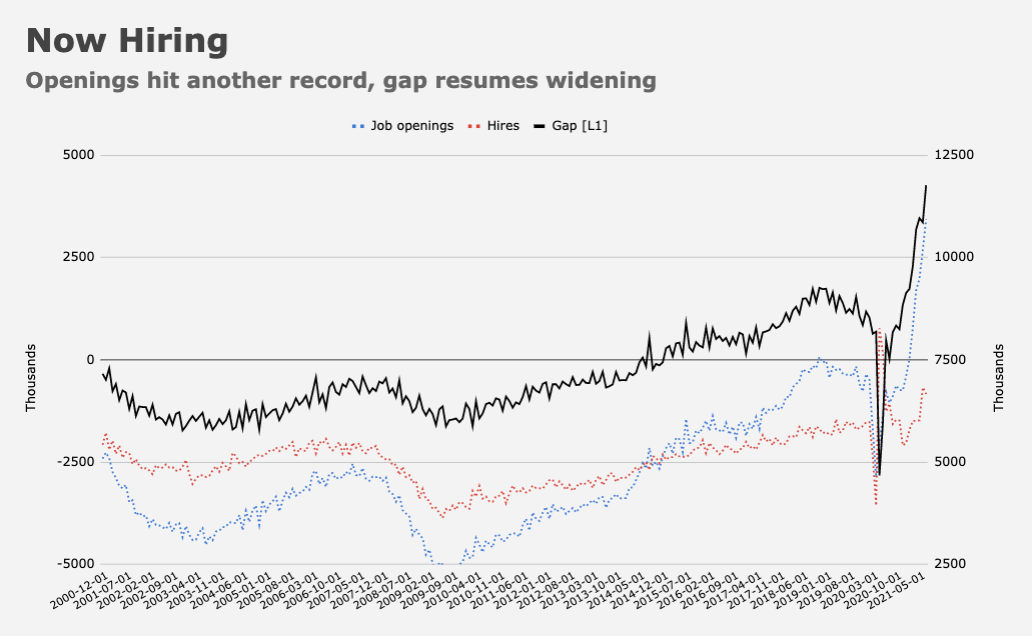

August JOLTS are due Tuesday. The numbers will doubtlessly show the acute mismatch between vacancies and hires persisted into summer’s end. The record disparity is expected to dissipate as pandemic unemployment programs roll off, but suffice to say employers are still struggling to fill open positions.

CPI data for September takes center stage on Wednesday. Team “transitory” scored a small victory last month, when August’s numbers showed core prices increased much slower than expected. Still, PCE prices ran the hottest in three decades for a third month in August, underscoring the extent to which “transitory” is becoming a relative term.

Consensus is looking for a 0.2% increase on core CPI and a 0.3% monthly gain on the headline gauge (figure below).

This comes as markets fret over stagflation and the prospect that the Fed could end up tightening into a slowdown.

“August’s lower-than-expected core CPI print offered the first evidence that the Fed’s transitory characterization might ultimately be more apt than many market participants have been assuming,” BMO’s Ian Lyngen and Ben Jeffery remarked. “This doesn’t imply that even a benign read on core inflation as the third quarter came to a close would completely settle the debate, rather, another check in the transitory column would simply prolong the period of inflation-linked uncertainty well into 2022,” they added.

“While it is too early to assess the persistence of inflation, recent comments by [Jerome] Powell at a panel discussion hosted by the ECB revealed his concerns over supply chain disruptions persisting well into next year,” SocGen’s Subadra Rajappa wrote, in her latest. “Alternative measures of inflation like the Dallas Fed Trimmed Mean PCE, which excludes extreme upside and downside price changes, and a similar metric from the Cleveland Fed are starting to show consistent increases in recent months, which could signal broader price pressures.” The figure (below) illustrates the point.

There are two ways to describe that visual. You could argue that core inflation (as reported) is moving lower to converge with the smoothed metric. Or you could say the alternative gauge is moving up to reflect broader-based price pressures. The yellow arrow shows the gap closing.

For their part, TD isn’t particularly concerned about a worst-case scenario. “‘Stagflation’ has become a hot topic on Wall Street, but we don’t anticipate anything that could accurately be described that way,” the bank’s Jim O’Sullivan, Oscar Munoz and Priya Misra said late last week. “Along with modest inflation, we expect moderation (not stagnation) in growth and relatively low unemployment,” they went on to write, adding that “inflation would likely slow more than we are forecasting if growth were to weaken sharply and unemployment started rising again [and] while inflation could stay relatively high initially if growth stagnated, stagflation requires persistently high inflation despite high unemployment and weakness in growth.”

You can write your own script and spin your own narrative. Nobody really knows. What we do know, though, is that consumers harbor the most unfavorable views towards buying conditions in decades (figure below, for example). The preliminary read on University of Michigan sentiment for October (due Friday) will likely suggest more of the same.

For now, consumers seem to believe some version of the transitory narrative. For how long, it’s hard to say.

Retail sales, due shortly before Michigan sentiment on Friday, will give market participants a fresh read on the consumer. Recall that while August’s numbers suggested Americans are still spending, there was evidence that the Delta wave kept would-be diners and drinkers away from restaurants and bars.

Also on deck in the new week, NFIB, PPI, Empire manufacturing and a bevy of Fed speakers.

Oh, and the minutes from the September FOMC meeting are due as well. Expect the usual tasseography. A truncated supply schedule (Monday is Columbus Day) will see Treasury sell $58 billion in 3s and $38 billion in 10s on Tuesday, followed by $24 billion in long bonds Wednesday.

{kind=link}

H-Man, nice job describing a hot market and anything goes depending on your bent. But goodness gracious, it appears there is littlle news to abate rising inflation or stop the march of rates going higher which seem to be joined at the hip.

I’m wondering how workers fired or furloughed for not getting vaccinated will show up in data. I think they are generally not eligible for UE benefits, but will they still show up in initial claims? I would think they will show up in (fewer) net new jobs. Granted this is likely to represent only a fraction of one percent of employees (based on some large hospital employers’ experiences to date) but could still meaningfully affect one or two months of jobs data.