It’s been a rough stretch for hedge funds’ most popular positions.

If you’re inexplicably inclined to help someone else buy fine art and bespoke Bentleys in exchange for putting your money into tech stocks, you may be feeling at least at little bit aggrieved.

Bloomberg obliquely picked on Amazon this week, as though it’s their fault that hedge funds are predisposed to a herd mentality in a world where beating benchmarks is exceptionally difficult thanks to low-cost indexing and a Fed determined to protect the indexers from any “drawdown” larger than 3%.

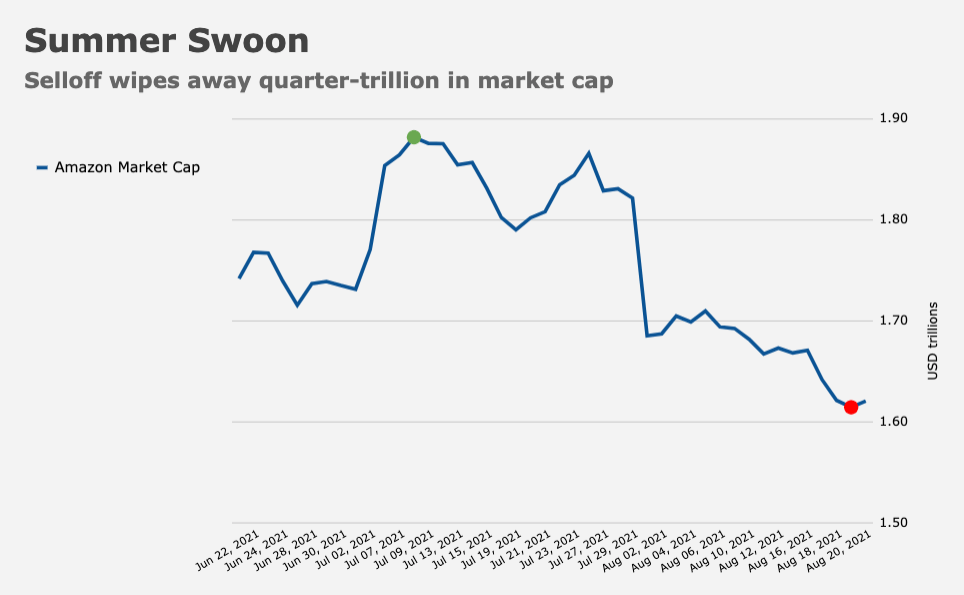

The linked article cited RBC’s list of top hedge fund holdings, which showed Amazon overtaking Microsoft for the top spot in the second quarter, setting some funds up to suffer from Amazon’s ~15% decline from July’s peak (figure below).

“Amazon Investors Are Panicky,” a separate piece announced. Still another touted “Amazon’s $267 Billion Summer Wipeout.”

Some of that seemed a bit overwrought, to put it nicely. Amazon is still up 90% from the pandemic lows.

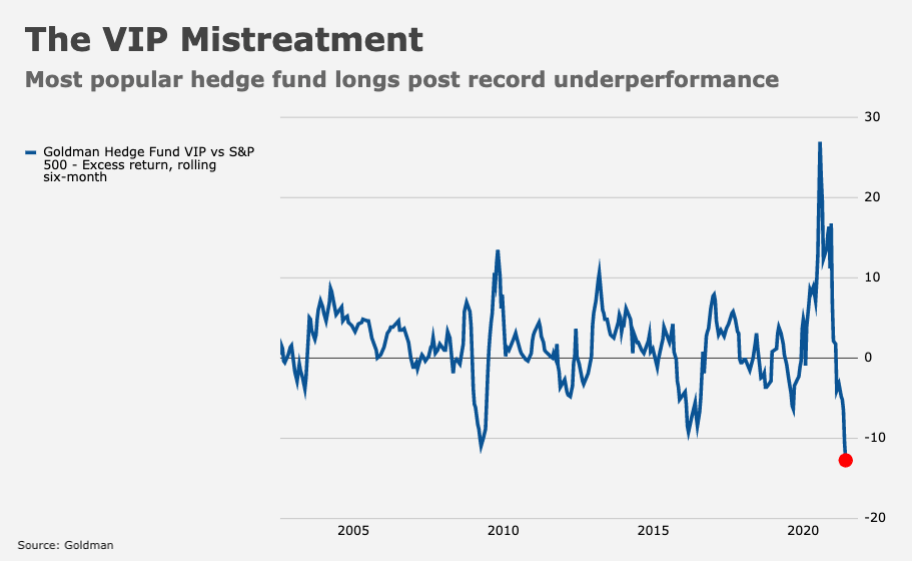

But this isn’t about Amazon, it’s about hedge funds. And on that score, Goldman’s Hedge Fund VIP basket has trailed the S&P by 13 percentage points over the past six months. That’s a record, and as the bank’s Ben Snider noted, the drag “has outweighed the positive alpha from concentrated short positions.” The figure (below) gives you a sense of things.

As a reminder (and I doubt anyone needs it), the bank’s VIP list is comprised of the 50 stocks which show up most in the top 10 holdings of fundamental hedge funds. Since 2001, the VIP basket has outperformed the S&P in 60% of quarters, with an average quarterly excess return of 63bps.

One problem is the rout in Chinese tech, which reached a staggering 50% this week. At the beginning of the third quarter, a third of hedge funds in Goldman’s sample had long exposure to Chinese ADRs. That means the wild declines instigated by Beijing’s regulatory crackdown likely presented a significant challenge for funds.

There are myriad caveats (Goldman went into extensive detail on hedge fund trends vis-à-vis Chinese shares), but the bank’s Snider noted that “the overall popularity of China ADRs registered as the highest in our data history, making clear that hedge funds were generally not prepared for the regulatory shift and its impact on share prices.” To be fair, I’m not sure anyone was — “prepared,” that is.

Among Chinese shares, BABA was the most popular hedge fund holding. The shares have been in the top 10 on the overall VIP list for 17 straight quarters. That said (and this is one of the caveats), it fell out of the top five for the first time in three years last quarter, replaced by Apple.

As the simple figure (above) shows, it’s been a rough year. The stock fell an eighth straight session on Friday. It’s had just three winning sessions in August. The company’s Hong Kong-listed shares hit a record low last week.

The table (below, from Goldman) is self-explanatory, but just in case, it shows which China ADRs had the largest number of hedge fund owners at the start of Q3 and which ones saw the largest increases and decreases in hedge fund ownership over the course of Q2.

Out of all the stocks in Goldman’s basket of Chinese ADRs, just one managed to generate a positive return since February.

In a testament to… well, to a lot of things really, the top five stocks in the VIP basket are just the FAAMG cohort (in order, the top 10 are Facebook, Amazon, Microsoft, Alphabet, Apple, Mastercard, Alibaba, Visa, PayPal and Sea Ltd).

So, the five stocks that matter most to hedge funds are the same five stocks that matter most to anyone who owns SPY (figure below).

Given that, you might fairly ask why you wouldn’t just own SPY for nine basis points or better yet, VOO for three.

The answer, in part, is that with hedge funds, you get the benefit of active mismanagement, 63% concentration in your top 10 longs and, as a bonus, short positions which may or may not end up being piranha food for the Reddit crowd (per Wikipedia, “piranhas typically do not represent a serious risk to humans [but] being in the water when already injured or otherwise incapacitated increases the risk”).

Coming full circle, Amazon ranked on Goldman’s “Rising Star” list last quarter.

The stock was among those which saw the largest increase in hedge fund popularity.

So, just as Amazon’s figurative star was rising among hedge funds, and just as Jeff Bezos was blasting himself into the literal stars, the company’s star was falling in markets.

Somehow, though, I imagine it’ll remain a favorite among buysiders, sellsiders and retail investors alike. (After all, what else are you gonna own? AMC?) BABA, on the other hand, may be another story.

I have been of the opinion that Chinese shares have been uninvestable for a long time, as I am not a high ranking official of the Communist Party. One has to wonder about what on earth possesed hedge fund managers!