Market participants will digest top-tier US data this week, with April payrolls headlining.

Consensus expects to hear that nearly 1 million new jobs were added last month. A blockbuster of that magnitude would take up a sizable amount of remaining labor market slack, even as it would still leave the economy more than 7 million jobs short of pre-pandemic levels.

Economists see the unemployment rate falling to 5.7%. Assuming consensus (which sat at 978,000 headed into the week) is somewhere in the ballpark, the economy will have added 2.59 million jobs in 2021 (figure below).

The jobs data will be considered in the context of last week’s first read on Q1 GDP which, notably, showed that not only has output nearly recovered, but growth may actually be on a more aggressive trajectory than if the pandemic had never occurred. A Pyrrhic victory if ever there was one. Jobless claims fell to a pandemic-era low for a third straight week in the last read.

“There are two schools of thought as it relates to the second quarter data,” BMO’s Ian Lyngen and Ben Jeffery wrote, in their weekly. The first, they said, is that Q2’s data “will set the tone and reveal the trajectory for growth throughout the balance of the year.” What they called “the alternative interpretation” is simply that blockbuster performance in the first half “will largely be a function of pulling forward reopening timelines and the associated economic upside.” Lyngen and Jeffery are “leaning toward the latter camp,” but noted they’re “all too cognizant that the recovery is in uncharted territory and as such the magnitude of the swings in the data simply lacks… context or anchoring.” (I’ll say.)

Also on deck: ISM manufacturing and services. Market participants will been keen to get a fresh read on supply chain bottlenecks, price pressures and the extent to which surging input costs are poised to be passed along to consumers. The alternative is crimped margins and profits. In March, ISM manufacturing printed the hottest since 1983. The non-manufacturing gauge registered a record.

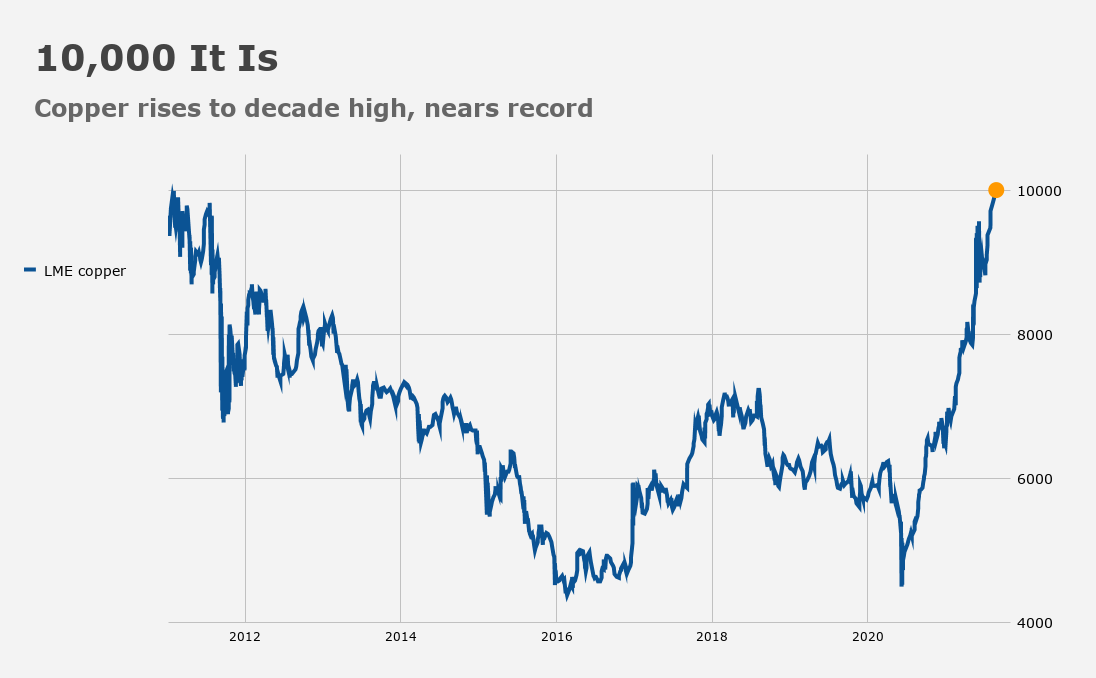

Commodities on are on an absolute tear. As Bloomberg put it in an amusingly colloquial headline, “The Price of the Stuff That Makes Everything Is Surging.” Copper and lumber are probably the most high profile examples, with the former set for a record above $10,000 and the latter screaming higher like Bitcoin on speed. But crop prices are rising swiftly too (figure below).

The surge in commodities means different things for different businesses, nations, income cohorts and investor types. Not all of those things are good.

For now, it still seems at least as likely as not that inflation pressures will, in fact, be “transitory,” as many eye rolls as that adjective will invariably elicit. One question we probably don’t ask enough is what “transitory” actually means. If I’m severely nauseous and I go to the emergency room, I’m ok with it if the doctor checks me out, tells me I seem fine and sends me home with a two-day supply of Zofran. That’s “transitory.” But if she writes me a prescription for six months of Zofran, I’m likely to protest to her that I can’t stomach (figuratively and literally) six months of severe nausea even if six months is still “transitory” in the grand scheme of things.

Anyway, the figure (below), shows breakevens and commodities. Ostensibly, the inversion (light blue shaded area) helps make the Fed’s “transitory” case, but that’s not going to be much solace in the near- to medium-term if some of the price pressures percolating across supply chains start showing up at cash registers like lumber prices are manifesting in new home costs.

![]()

In the same note cited above, BMO’s US rates team suggested that rising food costs could imperil the recovery, at least at the margins. People do have to eat, after all (figure below).

As one commenter reminded me several months back, absorbing, say, a 5% increase in the grocery bill isn’t easy for a family of four if the price increase persists in perpetuity. The Bloomberg Agriculture Index was up 14% in April.

“The acknowledgment by large food producers that some price boosts may be required leaves us somewhat concerned that higher food prices could come at the expense of broader consumption and ultimately the pace of the recovery,” BMO’s Lyngen remarked on Friday afternoon.

He went on to note that while “the Fed will look through increasing food costs… given the aspirations for 2021 to see 6.5% aggregate growth and the role consumption plays in the domestic recovery, any headwind is hardly a welcome development at this stage.”

On Sunday, Bloomberg reported that Joe Biden is “quietly laying the groundwork for a long-term increase in food aid for tens of millions of Americans, without going through the ordeal of a fight with congressional Republicans.”

The article said the administration’s review of the Thrifty Food Plan “could trigger an automatic increase in benefits as soon as October 1, a day after expiration of a temporary 15% boost in food stamp payments that Biden included” in the latest virus relief bill.

{kind=link}

I’m not for withholding food from hungry people but what is behind the rise in crop prices? If they are supply constraints, giving more money to shoppers won’t really do anything but push prices higher still… that’s the limit of MMT, from their general point to a specific market.

I’ll add that food doesn’t allow for many substitutes… 🙂

If the issue is supply disruptions, then addressing those would be the fix required. But that may be harder than sending money (however difficult that is, in the face of Republican opposition).

“What they called “the alternative interpretation” is simply that blockbuster performance in the first half “will largely be a function of pulling forward reopening timelines and the associated economic upside.”

This is almost certain. With only 25% of the US population fully vaccinated the pace is already slowing. As the radio news story this morning intoned, the slowing take-up rate is demand-driven. It’s not a widespread lack of supply. How can we assume that the Pollyanna forecasts of a sustained post-Covid boom will be proven correct when the likelihood of “post-Covid” looks less and less likely?

What am I missing here?

More than just ag commodities are on the rise. Also got to get that stuff to the store. Food products are among the most expensive to ship as the weight/value ratio with the shipping cost per mile is lousy. Plus pump prices are up and look to stay up for a while. A bumper crop this summer will knock down some of those prices, but a bad season could create a real mess. The crop price graph shows it hasn’t been all that long since ag prices were this high but that may not be much of a consolation for those still out of work. As for metals prices many folks don’t fully appreciate how those producers can quietly work with price elasticity to increase revenue by the use of accidentally/on purpose reductions in process volumes. Turn off some aluminum pot lines and cut back copper smelting a bit and revenues rise from prices rather than volume. This approach also allows firms to cut fixed costs and see operating profits climb. Lots of ways to skin the micro-economic cat, even when there is free(?) market competition.

I may have been the commenter from a few months back…

to throw gasoline on the fire (for my household anyway) 2 major manufacturers have forecast 5-9% increases on the price of diapers effective June (or September depending on which manufacturer). Wish there were “base effect” there to blunt the impact but diapers are already really pricey.

Anyone have experience with cloth diapers?

Fatmoose, as long as you have an energy-efficient washing machine and don’t mind an extra chore every 2-3 days, cloth diapers work great. I think we used BumGenius brand (?). Was 2014-2017, so was a recent experience.

Thanks for the response. how/where did you store them in between?