America’s largest corporations are beating analysts’ profit estimates at a rate not seen in at least 22 years. But, perhaps unsurprisingly, that hasn’t translated into outperformance.

Nearly 70% of S&P 500 companies have bested consensus forecasts by at least one standard deviation so far this earnings season, according to Goldman, the best showing since 1998. And yet, as the bank’s David Kostin wrote Friday evening, this quarter’s impressive results have been met with a resounding “meh” from a market willing to reward beats with just 26bps of alpha the following day, far below the average of 110bps.

And it’s not just the bottom-line. 57% of reporting companies beat estimates on the top-line. That’s a record.

In 2021, the outlook is all that matters, and despite the inherently tautological (almost nonsensical) nature of management proclamations about the future being “exceptionally uncertain,” the market wants the C-Suite to pretend. It’s better to venture a guess than it is to take a page out of Apple’s playbook and admit that we can’t know what we don’t know.

In the same note, Goldman recounted some things we do know. Namely, that “several of the largest S&P 500 firms have recently announced substantial cash spending plans.”

For example, Apple is planning hundreds of billions in domestic investment and between the two of them, Apple and Google authorized $140 billion in buybacks, a figure that exceeds the market cap of 444 S&P 500 companies.

This sounds a bit dry, but it’s notable. Goldman upped its forecasts for cash spending this week. The bank now sees spending rising 19% versus 10% previously thanks to expectations for a robust economic recovery and better bottom-line growth. “S&P 500 cash to asset ratios are at record highs,” Kostin noted, adding that “investing for growth will continue to represent the largest share of wallet.”

While the bank expects buybacks to jump materially after 2020’s pandemic-inspired slump, Goldman sees capex outstripping repurchases (on an absolute basis) both this year and next. Spending on R&D is expected to be strong as well (figure below).

Capex is seen rising 15% this year, R&D 9%, cash M&A 45% and buybacks 35%.

If you’re wondering whether tax reform would impact these estimates, the answer is “yes.” Goldman’s house projection is for Democrats to eventually pass a watered down version of Joe Biden’s proposed tax overhaul. Even a more moderate rewrite of the tax code would affect spending plans, Kostin said, before noting that Goldman would “expect higher taxes [to] weigh on buybacks more than dividends, capex, and R&D” given that “repurchases have exhibited greater variability than nearly ever other use of cash.”

The implication is that this is just another area where Democrats’ proposed tax reform would favor labor over capital or, at the least, would compel corporates to put cash to some productive use rather than simply returning it to shareholders or otherwise using it to engineer earnings beats and drive up share prices. In effect, this is the opposite of the corporate behavior encouraged by the Trump tax cuts, which aren’t exactly hard to spot on charts showing buybacks (red bar above) and earnings (below).

You might fairly argue (as many folks do) that in an environment characterized by a dearth of attractive investment opportunities, companies ought to return cash to shareholders. Of course, it’s (almost) always possible to make that argument.

It may not even matter. As Kostin went on to say, “following the cash crunch of 2020, investors have been rewarding companies spending cash, regardless of the use.”

Although “investors have historically rewarded companies returning cash to shareholders… since early November, all three cash spending factors have outperformed the S&P 500,” he wrote, referencing factors for dividends + buybacks, capex + R&D and M&A.

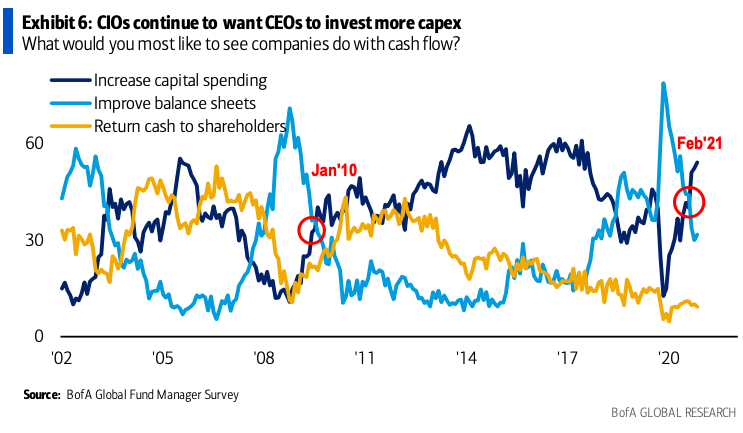

In the latest edition of BofA’s Global Fund Manager Survey, CIOs expressed a clear preference for capex (figure, below, from the survey).

In addition to preferring capex to (more) buybacks, fund managers in BofA’s survey appear to be rapidly losing interest in balance sheet improvement as pandemic concerns fade.

The bank’s Michael Hartnett called the crossing of light blue and navy blue lines “escape velocity.”

“… between the two of them, Apple and Google authorized $140 billion in buybacks, a figure that exceeds the market cap of 444 S&P 500 companies.”

Here’s an idea, why not these two take that lovely cash and divvy up the 400 lowest caps in the S&P and buy them all for the earnings (most earnings were beats, remember). While this might make next year’s comparisons a bit tougher, it would really boost the returns of the big two, at least compared to the results of the buybacks.

One thing that does my head in is this notion of unparelled uncertainty, which logically makes a whole lot of sense considering the unprecedented pandemic shock and unprecedented policy response, the speed of the asset recovery, the fact that 34% of income is coming from the US government, yet if you look at measures of uncertainty, they are crashing re-Baker, Bloom and Davis measure.