Equities looked to close out the week on a high note, as traders and investors appeared to cheer Joe Biden’s new vaccination target for the world’s largest economy and the Fed’s decision to lift restrictions on bank dividends.

Or at least that was the generic narrative. Remember: You need a “why?” You can’t have unexplained buoyancy in equities. There’s usually a long list of readily identifiable culprits when shares are solidly lower. Sometimes, though, when the screens are green, you end up bereft when it comes to explanations. At that point, you just take whatever incremental news flow you have and put a positive spin on it. Or so I’m told.

I’m kidding. Not really, but it’s Friday, so levity is allowed.

“We expect, assuming they all have capital ratios above the required minimums, all of the top 20 banks to increase their dividends and in some situations increases in the dividend payout ratios, too,” RBC said.

Market participants will be fine with putting this week in the rearview. Vaccine drama in the EU, a botched lockdown announcement in Germany, the psychological overhang from five- and seven-year sales in the US, a bear market in Hong Kong Tech, volatility in oil and a critical shipping lane in need of the Heimlich maneuver, all made for a somewhat disquieting week.

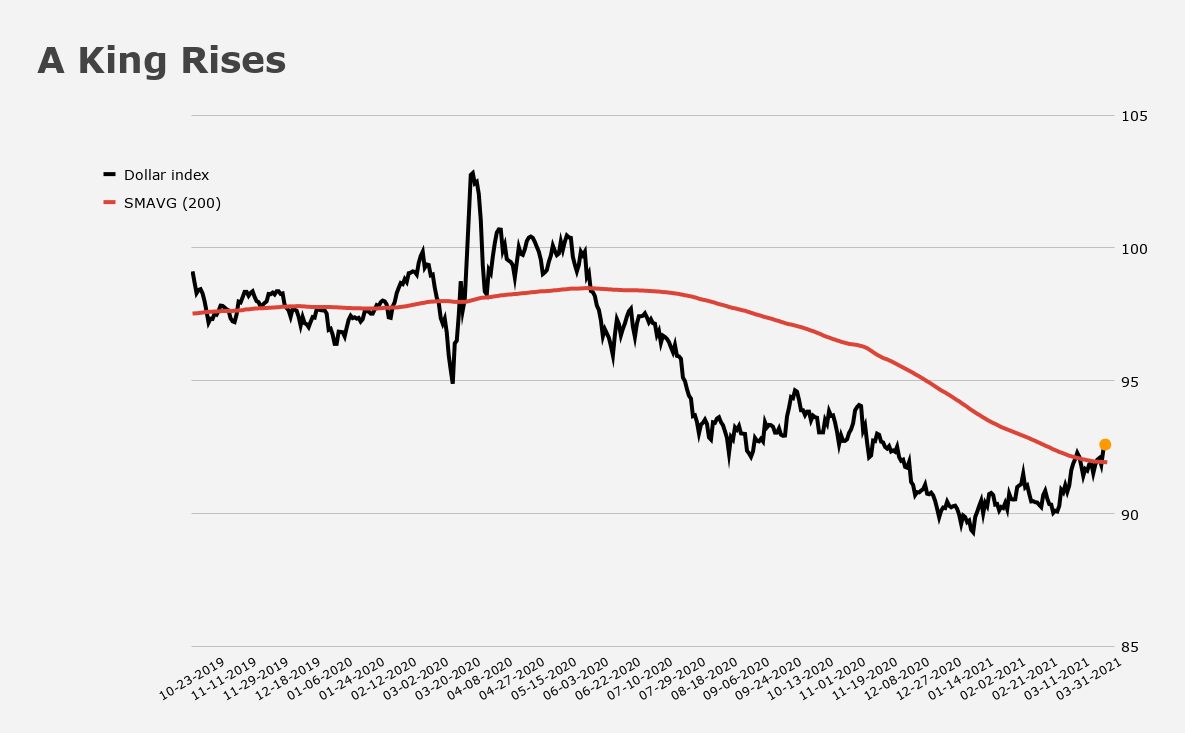

Speaking of disquieting, the dollar’s rally is poised to derail risk assets if it runs much further. That it came off a bit on Friday as risk sentiment improved was telling.

If Friday’s good vibes fade, expect the dollar to regain its footing. Indeed, as I wrote these very lines, the greenback was clawing back losses.

“The market trades as if factor models have significant sway as the volume slows down,” JonesTrading’s Mike O’Rourke said, describing what, to some, probably felt like a schizophrenic tape. “Value had underperformed growth by 3% for the week as of Tuesday’s close. Two days later, Value has recovered and is flat relative to Growth for the week,” he added, noting that “active investors continue to be tentative and are remaining patient as the quarter end rebalancing continues to play out.”

On Thursday, JPMorgan’s Marko Kolanovic said investors should be wary of the narrative that says month- and quarter-end will invariably be met with large net equity selling. That view, he suggested, lacks nuance and could be wrong.

While we’re on the subject of nuance, Rabobank’s Michael Every delivered a straightforward indictment (he didn’t use that word, but I will) of humanity’s generalized obliviousness. He put it in the context of Sino-US relations, a subject which, when it comes right down to it, is all that matters if you’re concerned about the future of species — all species, because if Washington and Beijing can’t get on the same page about at least some things, the world is going to become an even more dangerous place than it would have been anyway. Here’s Every:

Sadly but truthfully, very few Americans know anything about Chinese history. That includes Wall Street’s ‘China’ teams; DC think-tank ‘experts’; and politicians. Equally, a smaller but still overwhelming majority of Chinese people don’t know much about the shorter-but-nuanced history of the US. Most Americans also don’t know much about American history….and most Chinese people don’t know much about Chinese history either. I’ve been lucky enough to live in nine different countries (10 if you count the US via my father as proxy); and not one of them teaches an honest, no-holds-barred evaluation of its own national history.

On Thursday, Biden took a page out of the Trump playbook (the President surely wouldn’t admit to doing anything of the sort) in insisting that China won’t leapfrog the US on the list of global superpowers. That list isn’t long, by the way. There are only two countries on it.

Corporates are, of course, caught in the crossfire. Consider these short excerpts from Bloomberg:

China this week has pushed a campaign to boycott Western retailers after the US, UK, Canada and the European Union imposed sanctions over human-rights abuses against ethnic minority Uyghurs in Xinjiang. The furor started when the Communist Youth League amplified a months-old statement from Sweden’s Hennes & Mauritz AB expressing concern about reports of forced labor in the far west region, and quickly spread to other companies.

Shares of H&M, Nike and others plummeted as Chinese government officials endorsed the boycotts and celebrities cut ties with brands including Adidas, New Balance and Japan’s Uniqlo. Meanwhile, Chinese apparel makers have seized the opportunity with statements supporting cotton made from Xinjiang, boosting local companies from sportswear maker Anta Sports Products to leisurewear brands including Zhejiang Semir Garment Co.

Biden’s insistence that China’s rise won’t proceeded unimpeded “on my watch” was abrasive. Making good on the promise “requires a host of US measures from geopolitics to trade to capital flows to the USD to achieve,” Rabobank’s Every wrote. That, he reminded folks, “will naturally be seen as a policy of containment by China.”

The Fed has a role in that containment effort. And they’re no strangers to “war” efforts aimed at rescuing Americans from problems that started in China.

“I liken it to Dunkirk,” Jerome Powell told NPR’s Morning Edition, on Thursday, describing the Fed’s effort to rescue the US economy from the short-lived depression brought on by the “China virus” (as Donald Trump habitually referred to the pandemic).

“It was time to get in the boats and get the people, not to check the inspection records and things like that,” Powell added. “Just get in the boats and go.”

Of course, Powell and his colleagues already have a lot on their plate. “They have enough challenges to deal with now that they face a K-shaped recovery, and are targeting inflation, and unemployment, and social justice,” Every said Friday. “Now add a Cold War they can’t afford to lose to that list.”