There was trouble in paradise as the new week dawned.

A promising start in Asia metamorphosed into a rout in Chinese shares and weakness across the region as the specter of rising yields continued to weigh on investor psychology. 10-year US yields hit 1.60% and the dollar was poised for a fourth day of gains.

The onshore yuan erased its 2021 gains against the greenback.

The narrative was all too easy to latch onto Monday. Good news — whether the imminent passage of Joe Biden’s stimulus plan or China’s blockbuster trade data — is becoming bad news, as it suggests more upside for bond yields and, perhaps, dollar strength. “US exceptionalism” could be poised to make a comeback as a cross-asset theme.

“The case is building for a year of US exceptionalism as US growth upgrades on account of mega fiscal stimulus plans, are likely to meaningfully outpace EM, including China, growth revisions,” JPMorgan suggested late last week.

The last time the US was mashing the fiscal pedal to the floor prompting yields to rise and market participants to fret that the Fed would be forced to lean more hawkish than they otherwise might, stocks ended up correcting sharply (in Q4 2018). Of course, there was no pandemic then. And the labor market was in much better shape. And the Fed was already actively tightening whereas today, they insist no such tightening is in the offing for at least another two years.

Nevertheless, there are parallels. And you could argue that the nature of the fiscal stimulus (demand-side versus supply-side) makes an overheat much more likely.

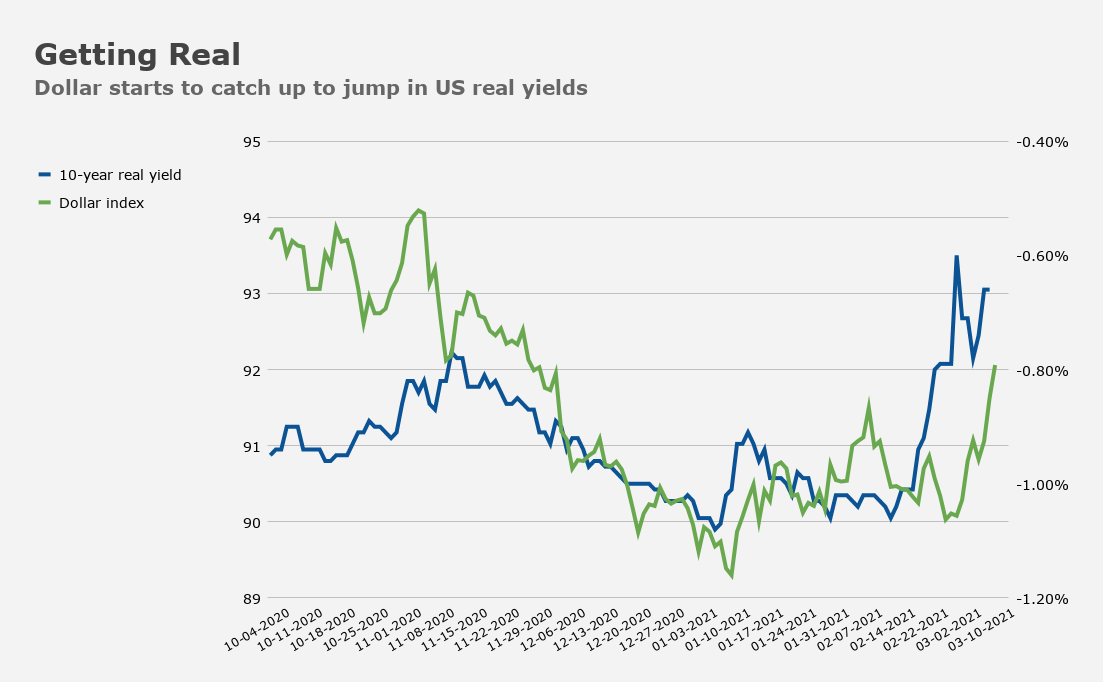

For the dollar, the paradox is familiar. Yes, the widening deficit “should” make the structural bear case, but the assumed reckoning baked into that bear thesis seems to get pushed further and further into the future as it becomes clear that stimulus can give the US an economic advantage. When the yield differentials pillar starts to move in favor of the greenback, it’s just fuel on the fire.

That’s daunting for risk assets. Especially those seen susceptible to a de-rating.

Arguably, the better the data, the more likely it is that the dynamic will be reinforced. “King dollar has made its return and options trading suggests further cash gains may be due,” Bloomberg’s Vassilis Karamanis declared. “As measured by the Bloomberg Dollar Spot Index, the greenback is enjoying the highest correlation between the cash and options market since August, and at levels rarely seen in the past decade when it comes to long-term wagers,” Karamanis added.

“This rise in real yields has driven the dollar higher, greenlit by the lack of willingness of Fed officials to push back against their increase,” BNY Mellon’s John Velis wrote Monday. “We expect that, as long as this increase in real yields persists, the dollar should continue to experience upward pressure, and it will require breakevens moving higher to put the brakes on the USD’s rise.”

Ultimately, a global recovery (i.e., the proverbial rising tide that lifts all boats) would be dollar bearish, but with the exception of China, it’s beginning to look like the US economy might be the standout when it comes to growth.

Some aren’t overly concerned about the prospect of US exceptionalism casting a pall over risk assets. “We think this USD rally is a bear market bounce and are invested in a Q2 story of a global recovery, which should lift all currencies – including the EUR,” ING said Monday. “Our call is that the current correction will provide some attractive entry levels for rejoining core bull trends against the USD given that the reflation story and equity and commodities gains have further to run.”

Fingers crossed on that. AxiCorp’s Stephen Innes had a straightforward take. “The dollar is stronger for no other reason than FX traders aren’t buying what the Fed is selling,” he remarked.

Closer to home, check out the MXP over the last week.

Higher USD may well damage our industrial side, which has been carrying the baton for us. Now higher mortgage rates may stifle housing. Will travel to Disneyworld offset all of that?

I like that final quote quite a bit

“The dollar is stronger for no other reason than FX traders aren’t buying what the Fed is selling,”