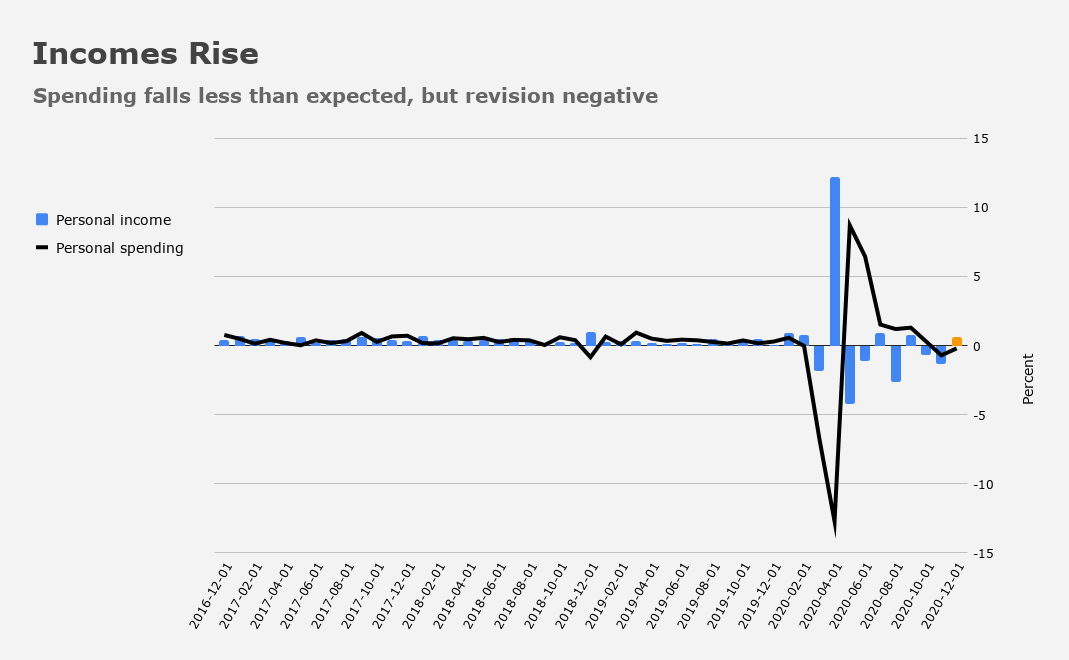

It might be “old news” in some respects, but personal income and spending data for December out Friday was better than expected.

Spending fell 0.2%, half of the expected 0.4% drop.

This of course comes on the heels of Thursday’s GDP report, and should be considered in that context. Personal spending for the quarter was weaker than expected, underscoring the extent to which waning stimulus, the winter COVID wave, and shrinking cash buffers are seemingly squeezing the American consumer. Note that November’s print was revised lower to -0.7% from an originally reported 0.4% drop.

Incomes rose 0.6%, a much stronger bounce than expected. However, you’ll note that it comes on the heels of a 1.3% drop in November.

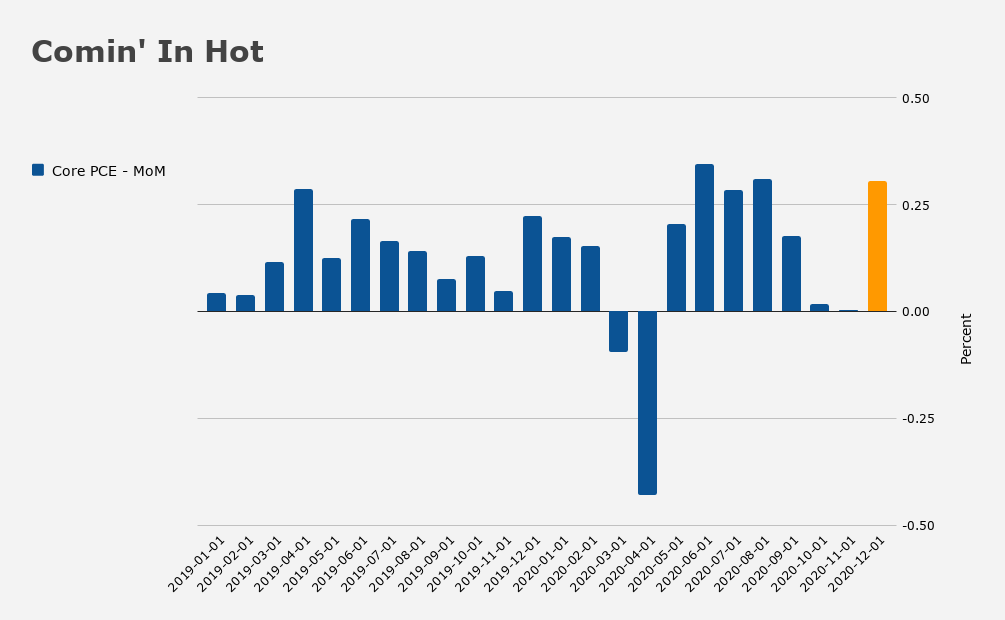

The standout from Friday’s data is probably the “hot” MoM rise in core PCE. At 0.3%, the increase was triple estimates. It’s also the biggest monthly jump since August. YoY, we’re at 1.5% on core.

None of this materially changes the macro narrative. Consumption is still falling and we know that incomes are impacted by federal assistance as the pandemic drags on.

“The increase in personal income in December primarily reflected increases in government social benefits, compensation, and personal dividend income that were partly offset by a decrease in proprietors’ income,” the government said.

At the margins, the PCE beats could bolster the reflation narrative, but, again, this is incremental information (at best) given the GDP report.