Earlier this month, I wrote about the wave of bankruptcies washing over America in the wake of the COVID-19 lockdowns.

What was an acute liquidity crunch is now manifesting in an insolvency crisis for some firms. A new study from Aaron Allen & Associates suggests some two-thirds of publicly-traded restaurants are teetering precariously on the brink, for instance.

In the ten days since “Why You Have No Choice But To Buy Corporate Bonds Despite Black Swan Bankruptcy Spiral” was published, nearly 20 additional companies with at least $50 million in liabilities have filed. That brings the total for 2020 to nearly 100.

The black line shows the number of filings for such companies through May of each year. 2020 is on pace to rival 2009 by year-end.

Hertz is perhaps the most high profile casualty so far (for a number of company-specific reasons), but other recognizable names are in the mix. Recent examples include Neiman Marcus, Tuesday Morning, J.C. Penney, J. Crew, and 24 Hour Fitness, which is preparing to file even as gyms open their doors across America.

The key questions going forward (well, besides who’s next), revolve around the effect on investor psychology and, of course, the extent to which the impact on the labor force offsets rehiring tied to government assistance (e.g., the Paycheck Protection Program) and the reopening push. Remember, the majority of the more than 20 million Americans counted as losing jobs during the survey period for the April payrolls report said they see their predicament as “temporary“.

The latest data from Epiq (provided by the American Bankruptcy Institute) shows total US bankruptcies actually fell in April by 46% YoY. However, ABI notes that total commercial chapter 11 filings were up 26% to 560 last month from 444 in April of 2019. Year-to-date chapter 11 filings nationwide were the highest since 2013 through last month.

“The extraordinary measures taken by Congress and the Administration to assist individuals and businesses weather the initial economic shock caused by the pandemic have likely staved off bankruptcy filings to date”, ABI Executive Director Amy Quackenboss said three weeks ago. “As financial challenges continue to escalate amid this crisis, bankruptcy is sure to offer a financial safe harbor from the economic storm”.

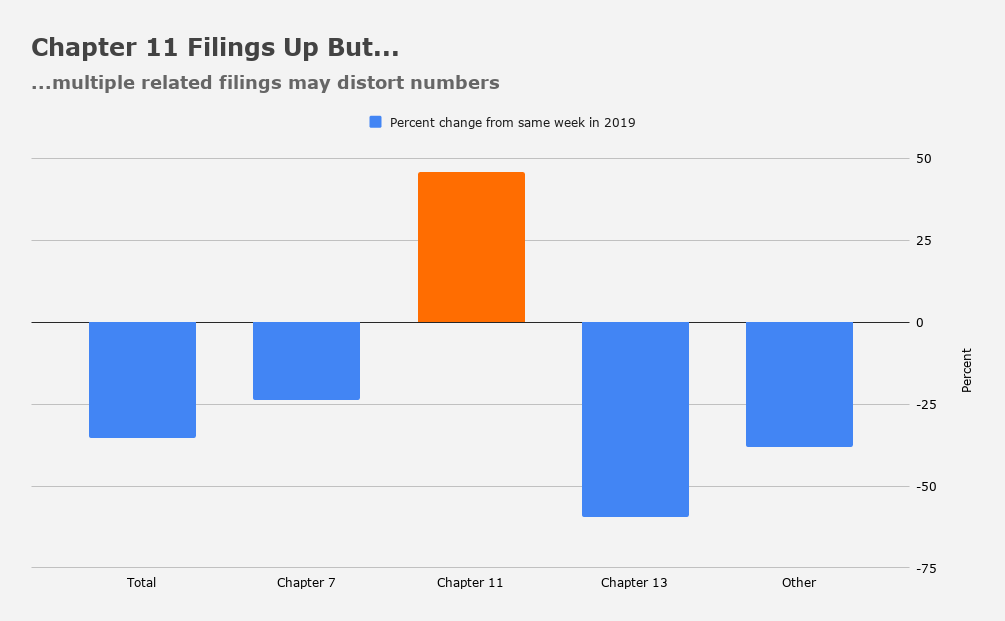

Weekly data from ABI tells an optically similar story. In the week ended May 24, total filings were down 35% from the same week in 2019, but chapter 11 filings were up 46%.

And yet, as the chart header indicates, this is difficult to illustrate simplistically. Consider, for example, the following excerpt from a blog post by Robert Lawless:

The thing about chapter 11 filings is that they are tricky to count. Each subsidiary of a corporate group gets counted as a separate filing such that one corporate group can artificially inflate the filings. The bankruptcy filing of Frontier Communications appears to have counted for over 90 of the 405 chapter 11 filings in the first two weeks of April this year. Gold’s Gym was responsible for 13 of the 334 filings in early May. The chapter 11 filings are inflated in this way every month, and the differences wash out over longer periods of time. But, when looking at shorter periods–even monthly periods–one entity with lots of affiliates can distort the numbers. I don’t think we should ignore the chapter 11 numbers, just recognize their imprecision. I am comfortable saying chapter 11 filings are roughly what they were one year ago.

That said, Lawless isn’t exactly optimistic about the outlook. Rather, he seems to suggest that the tsunami of filings has just been forestalled, not prevented.

“In addition to the ABI data, a few other key indicators we’re closely watching in order to track bankruptcies include the Bloomberg Bankruptcies Dashboard series and the number of customers filing for bankruptcies in the National Association of Credit Managers (NACM) survey”, NatWest wrote, in a recent note.

“So far, both gauges show tentative evidence of rising bankruptcies”, they go on to say, adding that “some of the increase likely reflects companies that may have already had existing operational and financial challenges that were exacerbated by the impact of COVID-19, [while] other companies may still be in the process of running down cash”.

As far as new business creation, the series is starting to normalize after a plunge (red line in the figure) but given the economic environment, one certainly imagines it will be a tall order for fledgling enterprises to get off the ground.

(NatWest)

“We continue to be skeptical that we will see a sustained ‘V-shaped’ recovery”, NatWest goes on to remark, in the same note, before suggesting that “the damage done from lost income, higher unemployment, and what appears to be a coming wave of bankruptcies, seem likely to weigh on consumer and business spending for some time even when the economy starts to recover”.

As for Professor Lawless, he said last week that a rise in bankruptcies is “the most probable scenario” in his opinion, but implored everyone to “have humility about how much predictive power our past experience gives us in the face of the current crisis”.

“The scale of the increase and how quickly it will come are very difficult to say”, he added.

Nasdaq hitting news highs soon, what liquidity problem? What recession? Times are great, Buy, Buy, Buy Lol

I may be one of the few subscribers to remember the Kumamoto earthquake of 2016. As an event, and rather understandably, it barely registered in the global media and was forgotten within days, yet it was quietly disrupting Japanese national output for months afterwards. It was a powerful lesson on the sustained impact of supply shocks in our highly interconnected economies.

Fast forward to 2020 and we have had a supply shock impacting almost every single company on the planet. The current predictions for its likely impact are, I suspect, not just overly optimistic, but hopelessly so. I hope I’m wrong.

“…how much predictive power our past experience gives us in the face of the current crisis”

The dice we are rolling now have a few more sides. When the Fed dials in a firm floor for Main Steet, do we have an economic keel to this ship? Really?

This seems to focus on large scale bankruptcies. Or am I missing something. If so what about the main street bankruptcies? Since the pain of this pandemic should be felt hardest on those least able to withstand the difficulties. I have heard of one bar that is closing remainder of year. The owner took a job as did bartender. The result is they are shut down paying rent out of paychecks until the bar can be opened again. Is this not an effective bankruptcy even if not filed?

I’m going to guess that total bankruptcies were down in April because of an inability to file the paperwork at closed courthouses.