Manufacturing output in the US posted a predictably enormous decline in April.

Predictable though it was, this is another example of a data point that is so anomalous it manages to preserve some of its shock value even as everyone knew it was coming.

Consider that for this series, we have data going back to 1919. The 13.7% MoM drop in April exceeds any decline seen over 101 years.

This is all the more astonishing considering the data covers the 30s and 40s, a period when the series was extraordinarily volatile.

On January 18 of last year, the Fed “celebrated 100 years of the industrial production index” with a handy history guide, which includes the first chart of the indexes, published in the Federal Reserve Bulletin in March 1922. Here is that chart:

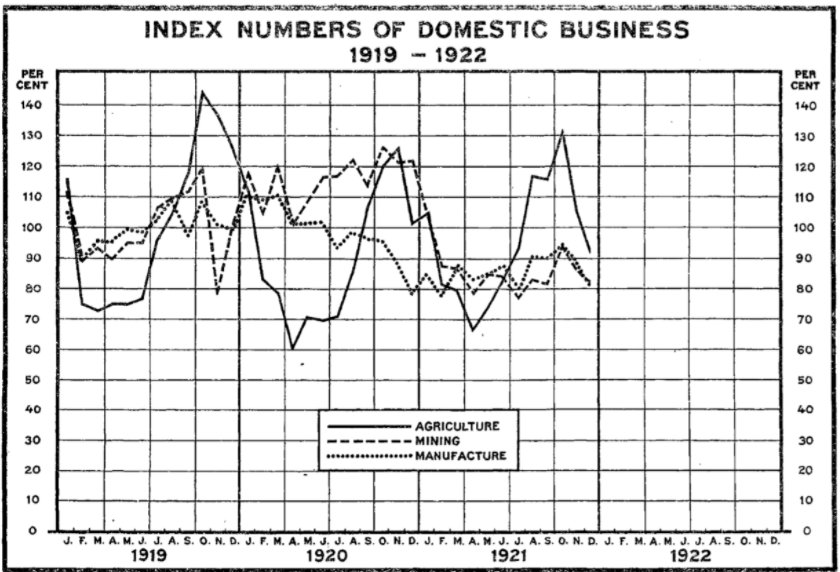

The Fed’s celebratory centennial report speaks to the point above about the volatility of the various series during the Depression and, after that, the war.

Consider the following from the Fed:

During the 1930s, the index of industrial production achieved prominence as an important indicator of macroeconomic trends. There were few methodological developments during this period, however, as members of the small staff who worked on the index were swept up in a number of projects related to the financial collapse, the Great Depression, and the New Deal.

As the economy improved and the pressure of other work demands eased, Federal Reserve staff members were able to refocus on the production indexes and, in 1940, published a major revision to the index. The revision was the first to include all industries in manufacturing, and it introduced a more detailed coverage of new and growing industries like machinery; it also introduced the use of production worker hours to measure the output of industries, such as chemicals and furniture, for which data on physical production were unavailable.

Economic activity in the early 1940s was dominated by the country’s involvement in World War II. Measuring production was especially challenging during this period of marked shifts in the composition of output. The activities of whole industries changed dramatically to support the war effort, and some industry names became misleading. The “auto and freight car” industry, for example, produced large numbers of planes and tanks. Furthermore, the typical seasonal variations of output for some industries evaporated during the war.

With that in mind, note that the COVID-19 crisis has managed to throw off a manufacturing production print so anomalous, it eclipses the largest percentage drops seen in the 30s and 40s, decades which witnessed a handful of 5%-10% declines (and surges, for that matter).

Capacity utilization plunged to 64.9% in April. That is also a series low, dating back 54 years.

It is exceedingly difficult to imagine how this kind of outright cessation in economic activity can somehow heal without scars.

It’s not so much that I actually doubt the “V-shaped” recovery narrative. The debate about “the letters” (so to speak) is somewhat silly considering the fact that with numbers this bad, any recovery at all will look like a “V” – if only a lower-case version, and if only for a few months. Hence the concerns about an eventual “W”.

The worry is that the US economy has suffered irreparable damage. Perhaps more importantly, I would contend that trends which were already in motion (e.g., the demise of brick and mortar retail and the disappearance of US manufacturing jobs) will be cemented, and otherwise perpetuated.

You could argue that on-shoring tied to a push aimed at severing what are now seen as risky supply chains will help bring back jobs, but I’d argue that rational management teams will at least consider whether it makes more sense to just speed up automation.

Why risk margins (which will invariably shrink if you make everything in the US) if you can just buy more robots? After all, a robot can’t get sick. It can malfunction, but it can’t catch a cold. And, crucially in the post-COVID world, a robot can’t sue you for getting the flu.

Coming full circle, I implore readers to consider that no matter how “expected” these numbers are under the circumstances, the fact that we knew they were coming doesn’t make them any less notable. Not by any stretch.

Covid-19 is so pernicious the health industry which in past recessions kept on adding jobs took a hit of approximately 1.1 million jobs. How many of those jobs will come back with the increasing use of telemedicine.

One more stunning achievement for the Trump years.

The US has had a steady decline in manufacturing, https://www.minnpost.com/macro-micro-minnesota/2012/02/history-lessons-understanding-decline-manufacturing/

Tesla manufacturing in the US is anomaly (and already there’s a China factory and a Europe factory).

The more insidious automation is software efficiency for service jobs like accounting, tutoring, etc.

Combined with the realization that remote video-only-employees could live anywhere (think lower wage localities/geographies), this crisis will accelerate the reduction in need for even white collar labor.

The dominoes I see are:

1. cheap capital (fed printing) available at the top (bank connections and relationship based lending)

2. capital invests (low risk since it’s “free money”) in automation (least risk for efficiency/production as outlined in the article)

3. cheap labor (domestic and international) due to the GreatDepressionII keeps wages low = less spending

So no inflation because consumers won’t have money (and industry are nervous and some just trying to survive – even the tech “winners” are cutting wages and have layoffs)… downward spiral.

Here’s a crazy idea: Chinese Consumer demand (along with a vaccine) will be what leads the world out of Depression.

“Why risk margins (which will invariably shrink if you make everything in the US) if you can just buy more robots?” Such a great question because it foreshadows so much about our future, reminds me of one of my favorite quotes: “The factory of the future will have only two employees, a man and a dog. The man will be there to feed the dog. The dog will be there to keep the man from touching the equipment.” Long live AI, at this point I would prefer a robot as president to the current human occupying the WH.

A competent AI may ascertain that a surplus of nonproductive homo sapiens is suboptimal.