In a high profile, if not wholly unexpected, call, Goldman slashed its year-end S&P 500 target by 16%, blaming the trajectory of rates.

Last month, David Kostin adopted a cautious cadence, noting that thanks to the summer rally, the US benchmark hit the bank’s target four months early. He obliquely characterized the surge from the June lows as a “leap of faith.”

Since then, “the rate complex has shifted dramatically,” he wrote, lowering this year’s target to 3,600 from 4,300. The bank’s updated valuation model implies the S&P will be just 4,000 at the end of next year (figure below).

In a “hard landing” scenario, the S&P could fall to 3,400 within three months and would be roughly unchanged from current levels by year-end 2023.

For weeks, I’ve argued that the rapid rise in US real yields from lows seen in the aftermath of the July FOMC meeting suggested equity valuations likely needed to fall. Although multiples did retrace a portion of the re-rating seen during the summer rebound, additional valuation compression was a virtual certainty.

On September 10, I said the ongoing rise in US reals was irreconcilable with the relative calm in stocks. Four days later, I reiterated the point, following Wall Street’s worst day in two years. Then, on September 16, I was even more adamant. “Recent de-rating in equities was insufficient for multiples to fall commensurate with the rise in real yields, which are up across tenors near 2018 highs,” I wrote, in “Breaking Point,” calling reals “kryptonite for risk assets.”

The figure (below) is very daunting. Reals (neon green) are rising virtually uninterrupted. The shaded blue area is the one-month pace. Stocks should be much lower — the June lows will almost surely be breached.

Although I try to avoid speaking deterministically, it often feels as though this is poorly understood by everyday investors. Stocks will struggle in the face of ever higher real rates. It’s as close to a guarantee as you’re going to get, especially when rising reals are a reflection of tighter policy, not a firming growth outlook.

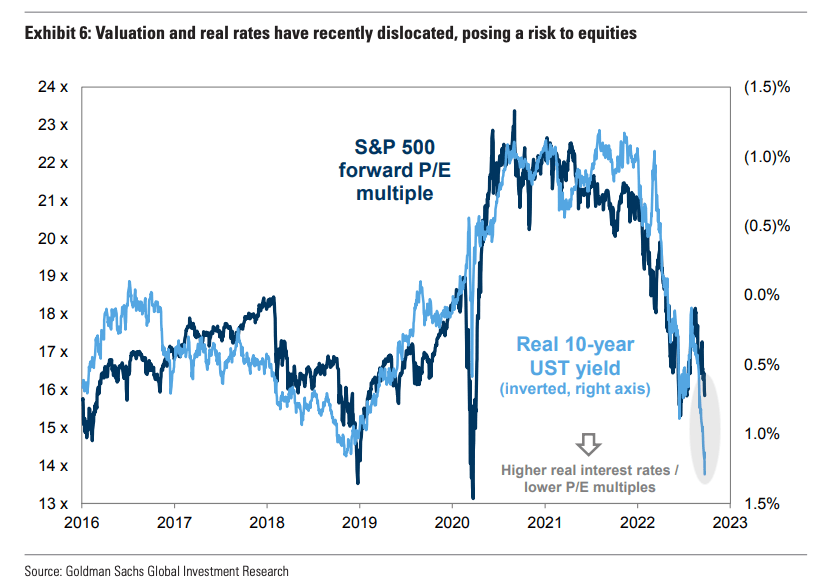

In his updated view, Kostin told the same story. “Changes in real yields have largely reflected the shift in Fed policy rather than growth expectations recently,” he wrote, adding that “the S&P 500 forward P/E multiple has collapsed from 21x at the start of the year when real rates were negative to 16x today when real rates are positive [but] in the past few weeks, the relationship has dislocated.”

Although valuations are lower from recent peaks, they “still trade above the level implied by the recent relationship with real rates,” Kostin said. “Based solely on the recent relationship with real yields, the S&P 500 should trade at a multiple of 14x rather than the current multiple of 16x.” The simple figure (above) illustrates the disconnect.

Kostin also addressed the ERP issue. Although a “resilient” growth outlook, still-anchored long-term inflation expectations and a rebound in consumer confidence may “help explain some narrowing of the yield gap,” the compression “has far surpassed the level implied by our macro model,” Kostin wrote. Stocks, he said, “appear priced for an optimistic outcome” considering “the likely path of data in the near-term.”

Speaking of the data, Kostin called inflation “more persistent than expected” and “unlikely to show clear signs of easing in the near-term.” Goods inflation may moderate, but “the broad-based strength in wage-sensitive services categories, such as shelter and food away from home, has added to the Fed’s challenge,” he fretted.

Goldman kept its 2023 forecast for index-level earnings, which was already below bottom-up consensus and represents a meager pace of profit growth (figure above). The bank still expects negative revisions and, as a reminder, believes margin forecasts are too optimistic.

That said, Kostin’s new price target is entirely rates-driven — it’s all about valuations.

“We previously assumed real rates would end 2022 at roughly 0.5%, compared with our revised assumption of 1.5%,” he wrote. “The higher interest rate environment means that our implied year-end P/E multiple is cut from 18x to 15x.”

The involuntary reactions from your assessments of investor expectations and likely outcomes in this economy, along with those of Goldman, and others, are cold water on hot, youthful passion. But the assessments are real and trustworthy. Needless to say, my expectations for 2023 are not hot, or even warm at this stage.

Most serious investors buy stocks not “the market”. For longer term investors there are more opportunities today though there may be more over the coming months.

We will be talking about rate cuts and QE4ever sometime in the first half of ’23 I suspect. This economy cannot handle higher rates imo.

Be smart everyone.

Actually, buying “the market” is almost always the better trade than pretending that any of us are able to consistently beat a low-cost index fund over the long-term by picking individual stocks. It’s my contention that there has never (ever) been a “good” stock picker. Only lucky ones. Unless by “good” you mean “possessed of non-public information,” in which case yes, sure, there have been plenty of good stock pickers throughout history.

For individual investors yes.

For retired HF managers I totally disagree.

I absolutely do not mean via inside information.

For pro investors short term pressures cause underperformance. i.e. career risk.

There is something called “time arbitrage”. In my opinion one of the most successful strategies out there.

Most individual investors and many pros go with the crowd. That is often a losing strategy.

It is pretty simple buy great companies with competitive advantages at good prices. They do exist (I have been buying them today). I have a “margin of safety” on those buys imo.

But you are correct, if you don’t know what you are doing (most individuals and many “pros”) then buy the good, the bad and the ugly and hope for the 10+ baggers to bail you out of the other 250 garbage names in the SP500. (Not meaning to sound snarky). Just the reality. The SP500 tends to buy new names at highs hoping they go higher.

I’ll continue buying quality at good prices. 😉

Wishing you the best. Trade/invest well my friend.

I should add.

I think individuals have a HUGE advantage because they do not have to “swing at every pitch” and can maximize the “time arbitrage” opportunity.

These advantages are ENORMOUS. HFs can have that, mutual funds rarely have that advantage. Individuals have it if they want it.

The keys are to curb the greed and fear and do the basic equity analysis needed (valuation work, business competitive advantage work, etc).

When SPACs and meme’s and price to sales ratios are talked about it is usually a time to be cautious, careful. Sure you might miss out on the last burst. But when fine companies are available at free cash flow yields exceeding “normalized” 10yr treasuries and have some growth and are run by good mgmts and have sustainable competitive advantages it is a lot easier.

Hope this helps a little.

I just noticed your first reply after you left the second one.

You’ve been around these pages for quite a while, so you’re doubtlessly aware that any condescension (implied or otherwise) directed at me is woefully misplaced, to the point of being borderline bizarre in that it seems to suggest you haven’t been reading me very closely over the years.

Also, I’d note that any “retired hedge fund manager” who’s spending his or her days screening for GARP stocks instead of, you know, indulging in various manifestations of personal eccentricity, is either i) a masochist, ii) running a family office because he or she doesn’t have enough eccentricities to indulge or expensive hobbies to pursue, or iii) didn’t retire with enough in the way of readily available cash to just “own and roll 3m T-Bills yielding 3.10% in risk-free heaven,” as a buddy of mine whose job it is to talk to hedge funds all day put it last week.

Hope that helps a little. Wishing you the best and thanking you for helping me indulge my eccentricities here every day.

Thou Goldman people are supposed to be the smartest people in the world I do believe they are human like the rest of us. But if the Fed keeps on raising rates past the point Goldman has in their estimates it could go lower. Since we are only 30 or so points from breaking the June lows and Powell is still planning on raising rates we should go lower from here. My only issue is getting more cash in my investment accounts so I buy when we hit those levels.

Also, the PEs assumed are too low imo and the estimates (even in hard landing) are too high.

In ’07 at this time of the year we were looking at $93 for ’07 and $100 for ’08. Market was trading around 1500 or so. Financials were about 40%? of EPS? And they were overearning.

Today we probably do $180 for ’23. Higher quality because of tech (yes, tech is a secular grower).

Rates probably never get to 6%. But assuming $180 is underearning a bit and a 20x mult on “depressed” earnings we get 3600 for mid next year.

And if we look back. This estimates assumes SP500 earnings took 15 years to double!!!! Is that really overearning????? Sure, maybe the real number in ’07 was $70 but still not a gret compounding giving some of the greatest companies in the world exist today and were a small part of the ’07 SP500.

The market is manic depressive imo. Personally I think a lot of quality stocks will nicely outperform bonds over the next 2-10 years.

But market participants aren;t thinking in these terms.

But who knows, maybe I am wrong. I am not “buying the market” but I sure am buying some great companies at decent prices that will nicely compound over the years.