On the eve of the first jobs report since Joe Biden assumed the presidency, US equities stormed ahead, rising a fourth session as last week’s tumult seemed a distant memory.

As the S&P gunned for another record, GameStop plunged — again.

Early last Thursday, at the height of the mania, GameStop briefly became the largest company in the Russell 2000. Fast forward just one week, and the stock had fallen from dizzying heights above $480 to below $60. The shares were down more than 80% on the week through Thursday afternoon.

Make no mistake, that’s a tragedy for someone. And probably for multitudes of someones (plural). For every millionaire last month’s mania minted, there were likely many latecomers who suffered catastrophic losses on their positions. Generally speaking, those hurt in the trade suggest they were “only having fun anyway” or “never took it seriously.” I hope they’re telling the truth. I really do.

Moving on, small-caps (as a group) fared well, surging nearly 2% Thursday. Headed into payrolls, the Russell 2000 was on track for its best week since the election/Pfizer readout.

But, as noted here Thursday, this week’s gains had an across-the-board feel to them. The Nasdaq 100, for example, was up almost 5%. Ebay, Netflix, and PayPal all jumped on Thursday.

Sentiment is getting a boost from upbeat data. Apparently, we’ve yet to reach the “good news is bad news” threshold. I contend we could get there eventually, but for now, the market is content to run on reflation narrative rocket fuel.

“[Thursday’s] US economic data saw further momentum re-accelerating the duration selloff already well underway in recent days, and [drove] another blast of ‘risk-on’ into an equities market which is trading like it’s short after the VaR-down last week,” Nomura’s Charlie McElligott said.

Remember when the “VIPs” had to be forcibly sold amid acute pain in short books? If you do, they don’t. It’s been a good week for the titans.

Notably, equities were able to perform despite a strong dollar. I’ve warned, tentatively, over the past couple of days that if the dollar’s bounce were to prove sustainable, it might eventually short-circuit the risk rally. But that goes into the same category as “eventually, good news could be bad news.” That is: It’s a story for another day.

Indeed, the Bloomberg dollar index at one point touched its best levels since December 2 Thursday. Treasurys were mixed ahead of the jobs report, but it’s worth noting that the 5s30s hit the widest since 2015 following better-than-expected claims data.

“With 10s at 1.14% and 30s at 1.93%, the market is poised for a potential ‘ah ha’ moment in one direction or the other,” BMO’s Ian Lyngen and Ben Jeffery wrote. “This may simply be in the form of confirmation of the prevailing range in the event the data doesn’t inspire a brighter economic outlook [but] the proximity to the 1.186% yield peak for 10s leaves open the potential for rates to be repriced higher should a strong round of hiring shift the sentiment on the lingering impact from the ‘dark winter’ of the pandemic to a less dire stance,” they added.

To be sure, expectations for payrolls were ratcheted higher this week — at least in folks’ minds. Between ADP and the upbeat read on the ISM Services employment subindex, there was rampant speculation that a big “beat” was in the cards. But is it still a “beat” if everyone expected it? We’re about to find out. Or not.

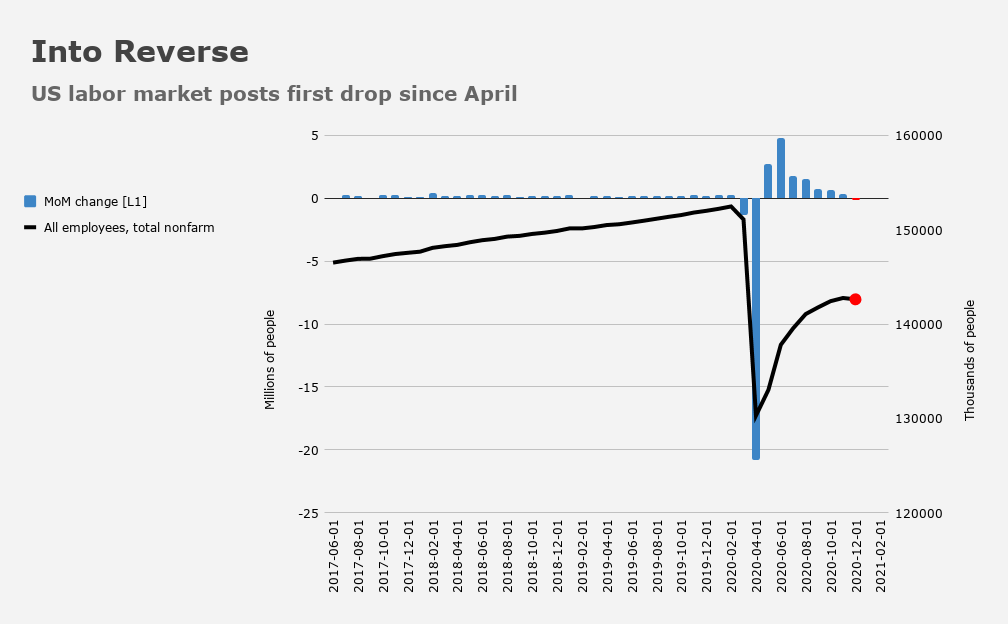

The key will be the leisure and hospitality sector. Market participants will be keen to know whether December’s purge (around a half-million jobs) was meaningfully ameliorated. Restaurants and bars were particularly hard-hit. As a quick reminder (which you probably don’t need), “you are here,” so to speak:

December’s drop was the first since April’s apocalyptic plunge. As of Thursday afternoon, it felt like nearly everyone believed January saw a rebound.

Meanwhile, on the stimulus front, it’s vote-a-rama time. The “worst part of the United States Senate,” as Brian Schatz called it, will find lawmakers forced to vote on hundreds (literally) of amendments in what Bloomberg aptly described as an “arcane parliamentary procedure.”

Politico offered what is perhaps the most succinct summary I’ve ever read of this truly absurd waste of air, breath, and time. “That public hazing is Senate tradition, the price the majority party pays to approve a budget resolution — an essential first move in bypassing the filibuster and passing major policy changes with a simple majority, the way Democrats did to enact Obamacare and Republicans did to achieve the 2017 tax cuts,” an article published Thursday read.

Schatz’s advice to the public: “Do anything to not watch vote-a-rama.”

Just another example of D.C. dysfunction and government paralysis.

If you’re wondering how Progressives would handle things if they were in charge, just ask Rashida Tlaib who, in a quote-tweeted response to someone discussing stimulus checks on social media Thursday, said: “This sh*t kills me. Stop messing around and get people their money.”

One imagines quite a few frustrated day-traders were screaming just that at their Robinhood apps around this time last week.

The last five minutes of trading across the three indices look like a veritable buying orgy.

No way I’d get out soon enough for when the next 6% down day hits. On those days, I wake up, check the market and know my “tight, trailing stop loss” (as the pros call them) is actually a 6% hit. Retail schmucks like me don’t stand a chance with our piddly little stop losses when those days happen.

I was re-watching a Grantham interview from January. He was asked about whether or not someone would be better off going to cash right now….