Lingering doubts about whether the US and China will, in fact, get across the finish line with an interim trade agreement tripped up risk assets at various intervals over the past several sessions, but all’s well that ends with more record highs.

Thanks in part to reassurances from Larry Kudlow, US equities closed the week on a strong note as the S&P logged its second-best day of the month Friday.

It was the sixth consecutive weekly gain for the benchmark, the best run since October of 2017.

Generally speaking, the S&P hasn’t been able to stay in overbought territory for very long outside of the post-tax cut euphoria and for a spell in early 2017. The last time US stocks were convincingly overbought was in late April, just days before Donald Trump broke the Buenos Aires trade truce with a Sunday evening tweet, setting in motion the May rout.

Speaking of the president, he wasn’t in a good mood on Friday, but he did take some time away from deriding congressional witnesses to talk up stocks. He even tweeted a CNBC clip celebrating Dow 28,000, and crammed in his own morning stock market tweet at the bottom.

https://t.co/8h6ZmdGlPf pic.twitter.com/shaijXMXli

— Donald J. Trump (@realDonaldTrump) November 15, 2019

The “Jobs, jobs, jobs” bit notwithstanding, Friday’s economic data was tepid, at best. Retail sales were mixed for October and Empire manufacturing underwhelmed.

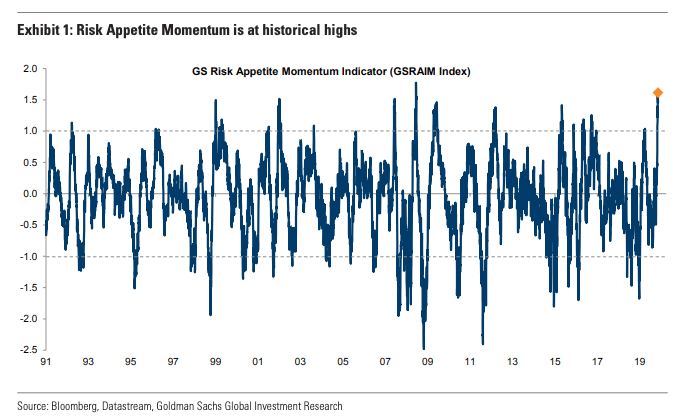

The recent push higher on trade optimism and speculation that an inflection in the global economy is imminent has driven Goldman’s Risk Appetite Momentum indicator to within a blip of its record high going back decades.

(Goldman)

The bank reminds you that “unlike the Risk Appetite Indicator, which is based on levels, the Risk Appetite Momentum indicator is based on 3-month changes and tracks short-term changes in investor sentiment”.

Earlier this week, Goldman declared that “the market is moving from TINA to FOMO”. The next day, the latest installment of BofA’s global fund manager survey proclaimed the onset of the FOMO mentality as well.

Goldman strikes a somewhat cautious tone on Friday. “High levels of RAI Momentum, e.g., above 1, have historically signaled negative asymmetry for equity returns”, the bank says. “Although the sharp increase in risk appetite has likely been exacerbated by bearish positioning, the high RAI Momentum suggests that investors have started to price in a bottoming of the growth slowdown, which increases the risk of disappointments”.

With stocks now clearly overextended, you’d be hard pressed to argue that a disappointment on the trade front wouldn’t entail equities giving some back. That’s not to say that the odds of a disappointment are higher or lower, it’s just to state the obvious. Trump has, in the past, used equity rallies as an excuse to ratchet up the pressure on Beijing on the assumption he’s “playing with the house’s money”, so to speak.

US equities have outperformed Mainland shares in China handily of late. Indeed, the S&P is sitting at its highest relative to the SHCOMP in more than a year.

The CSI 300 just logged its first weekly loss in four, and China’s economy is showing further signs of weakness. Fingers crossed Trump doesn’t decide to try and extract further concessions on the assumption Xi “needs” a deal.

Sometimes, it’s tempting to suggest China does, in fact, need an agreement more than Trump – at least from an economic perspective. The problem with that assessment is that if it were true, Beijing would have conceded by now. But they haven’t.

From a political perspective, you could easily argue that Xi would be better off with no deal at all than with a one-sided agreement that makes Beijing look weak. Trump, on the other hand, could use a “win”, and considering i) his base will buy whatever he’s selling and ii) markets will take whatever they can get, the White House would appear to have every incentive to get something done.

Trump is obviously desperate for a “deal”. And the projection of China being desperate the bigger tell is that he is. It will be nothing in the end. No diff from before the trade war started (except for the lost growth, damaged confidence, etc).

The republican messaging strategy is projection.

“the markets will take whatever they can get “…. This is true as long as it is a rally or inconsequential trading action . If not one of those two options the battle between simplifiers and complicators ensues. The former will look for return the the mean around the next corner or the next corner or the one after that…..The later has the advantage because inadvertently they will try the one or two things that have never been attempted and consequently serve to levitate the markets once again…..Context can be difficult here no matter what your experience level or

resources consist of.. Sooner or later this resolves itself and then everybody is on the same footing thanks to 20-20 hindsight… Thanking H….as always for his efforts to set parameters…

I see the obvious logic of why trump should want a non-deal “Phase 1 agreement” (meaning an agreement that at best gets back to status quo from where we began). But this is trump. Since when should we expect him to be logical? He’s a sociopath. I’m trying to see the other side of why we should expect the “negotiations” to fall apart and what that would look like. A thought problem as it were.