By David Stockman as originally published on Contra Corner and reprinted here with permission

All bets are off regarding conventional forecasts of the economic and financial future because central bankers have gone bonkers ever since the 2008 financial crisis. Their insane balance sheet eruptions have thoroughly obliterated all of the traditional relationships between Economy and Finance. The two are now virtually disconnected, suspended in their own separate silos.

Stated differently, busted financial market signaling mechanisms mean that all historically-rooted projections and inferences about the relationship between main street and Wall Street have become “inoperative” in the Nixonian sense. At month #103 of the business expansion, therefore, the S&P 500 at 2755 is flying blind.

Thus, if a recession were incepting in February, for example, there is nothing in today’s yield curve, credit spreads or bond pricing levels that would reliably warn you. That’s because all of these metrics arise from a gambling house vertical which is controlled, shaped and smothered by the central banks, not from the free market evolution of the real economy as was historically the case.

The overhang of $2.2 trillion of Fed-generated excess reserves in the banking system, for example, did indeed cause the asphyxiation of the once and former “money market”.

Yet how could it be otherwise under the current universal regime of monetary central planning? These folks are not in the business of “nudging” interest rates in the soft touch manner of the Fed back in the halcyon days of William McChesney Martin.

Instead, they are in the heavy-handed business of interest rate pegging (as in nailed to the wall), yield curve shaping (to purportedly stimulate housing and CapEx) and risk asset price-keeping (to promote wealth effects enthusiasm). That’s why we call the FOMC the “monetary politburo”.

Like their Kremlin predecessors, these 12 preternaturally wise and gifted men and women do mean to rule, not merely nudge (whether successfully or not is another matter and about as likely as Soviet Communism).

Accordingly, the current thin (54 basis points) twos-to-tens spread has precious little to do with the outlook for economic growth or profits on main street. Instead, it’s being manufactured inside the Eccles Building by a policy of jacking-up front-end rates sooner and faster than the slower and delayed ramp-up of QT (quantitative tightening) at the middle and back of the curve.

That is, the planned dump-a-thon of Fed-owned bonds and notes under QT is presently barely registering in the buying and selling equations of the electronic bond pits. Then again, QT is scheduled to hit a $600 billion in-their-face rate by next October, which will make for some pretty serious shape-shifting on the yield curve. But even that would be due to the monetary mechanics being implemented in the Eccles Building, not Economy-based price discovery on Wall Street.

At the end of the day, the truth is this: Modern central bankers believe that the free market in the financial system is always and everywhere wrong. Left to its own devices, money market rates would, apparently, be far too high, yields too fat and stock and bond prices too tepid. The nirvana of Keynesian full employment, therefore, would remain forever out of reach.

That is, save for the expert ministrations of our monetary central planners. Knowing what the market does not know about “correct” financial asset prices, central bankers have systematically falsified virtually every one of them: Casino prices have become anchored, therefore, in the dictates of the Eccles Building and its global counterparts, not free market price discovery.

How could it be otherwise when central banks have had their Big Fat Thumbs on the scale, sequestering debt securities by the trillions, thereby draining government and other bond markets of the massive “offers” that would otherwise weigh heavily on prices and yields?

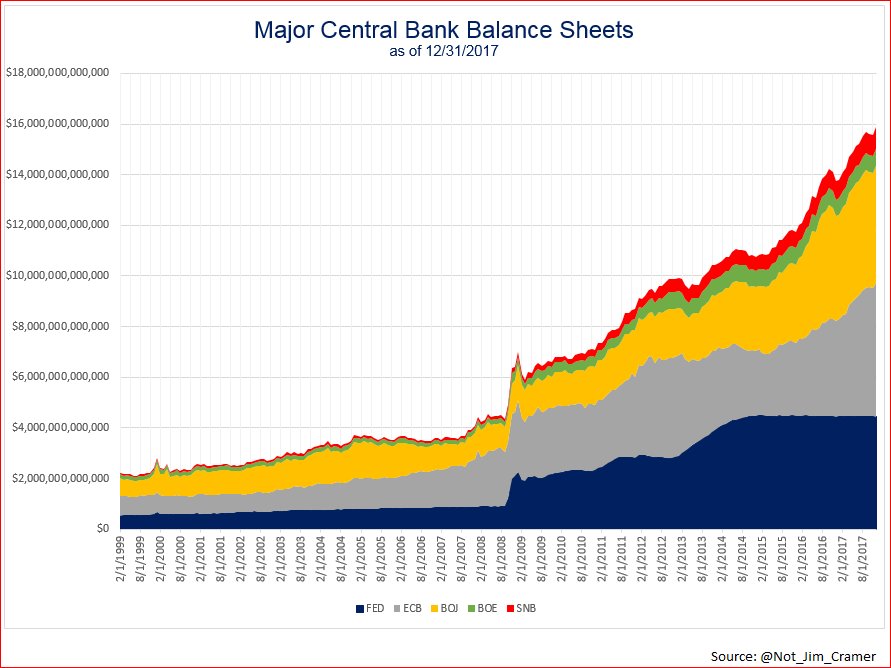

In fact, just the five major central banks have purchased $12 trillion of debt and other securities since 2007. But that’s not the half of it: Those massive buys were accompanied by a giant amplifier in the form of front-running speculators and arbitragers who hang around the casinos.

And these folks did get the hint—-buying that which central banks were pledged to buy. Sometimes right down to the CUSIP number.

This private front-runner effect was made all the more powerful, of course, by the fact that the key government bond markets—–US, German, Japanese—are deep and liquid, and therefore readily able to attract leveraged finance through the repo market and other short-term lending facilities.

Needless to say, buying a bond being levitated by the central bank’s open market desk on 95% repo bearing essentially zero cost is the closest thing to a legalized printing press ever invented. Literally, hundreds of billions of spread profits have been made by speculators since 2007 by simply buying the QE (longer term notes and bonds) and funding at the ZIRP peg.

But in getting unspeakably rich, they were most definitely not doing god’s work. To the contrary, the Fed’s massive direct purchases were already goosing bond prices to a fare-the-well; the front-runners just drove them even higher, pushing yields into the sub-basement of history as they did.

Moreover, the free money carry trade on US treasuries is just the beginning of the distortion and deformation flowing from monetary central planning What happens next is the hunt for yield.

That is, central bank repression has been so massive and unrelenting in the sovereign debt market that there is still upwards of $11 trillion of government paper yielding zero or negative returns. And you have the 10-year note of the quasi-bankrupt old age colony (nee Japan) yielding the next closest thing to zero—- exactly 7 basis points.

In a word, the resulting hunt for yield has generated an artificial demand for corporates, junk bonds and equities. So doing, this unnatural, induced demand for yield generated a new distortion within the distortion.

When there wasn’t enough LBOs and leveraged recaps to satisfy the thirst for yield, it did not take Wall Street underwriters long to persuade the stock option-obsessed denizens of the C-suites to sell bonds and use the proceeds to buy-in their own shares.

Needless to say, the very idea of debt-financed stock repurchases would have been considered beyond the pale back in 1987 when Greenspan launched the modern regime of Bubble Finance in earnest. But as shown in the graph below, on the margin virtually every dollar of S&P 500 debt issuance is now being matched by an equal volume of stock buybacks.

In short, corporate America is selling debt paper into booming bond markets to re-cycle the proceeds into their own version of a securities sequester program: stock buybacks. But that results mainly in the elevation of stock prices, not the higher investments in productive assets like plant, equipment and technology that our monetary central planners claim to be their goal.

In short, monetary central planners foolishly believe they are pegging interest rates and other prices in a manner that transmits directly into the real economy, and thereby elicits changes in spending among households and businesses designed to further their macro-economic goals.

But as the monetary technicians might say: The transmission mechanism has been short-circuited. Rather than levitating main street, central bankers have elicited a cascading, convoluted and combustible chase for returns inside the canyons of Wall Street, thereby inflating the price of most financial asset classes at self-fueling, accelerating rates.

In that regard, the current tepid 2% GDP growth rate has nothing to do with the massive coiled springs that have been generated inside the financial system. The former gains are entirely a function of the natural ability of capitalism to generate productivity growth and utilize available labor resources.

The $3.5 trillion of QE bond purchases by the Fed had exactly nothing to do with the modest real economic expansion since the 2007 peak.

The BOJ chart below shows the end game. If it doesn’t scare the bejesus out of you—we welcome you to your alternative financial universe.

But for our money we’d wager heavily that the 5X expansion of its balance sheet in the last nine years—-which resulted in its ownership of 45% of Japan’s prodigious debt and footings which now exceed 95% of GDP—-amounts to a financial firestorm waiting to happen.

Perhaps the absurdity of the situation is underscored by the fact that in the hey-day of industrial growth prior to 1914, the BOE’s footings under the gold standard rarely amounted to more than 2% of GDP. And the US economy—which grew by 3.7% per year between 1870 and 1914—- had no central bank footings, at all!

So the crazy fools at the BOJ have literally impregnated Japan’s financial system—and by extension and arbitrage much of the world’s—with coiled springs of distortion and combustible FEDs (financial explosive devices) that defy all previous historical experience.

But here’s the thing. The central bankers are now spooked by their own mad handiwork, and are accordingly beginning the great QT unwind—so that they have enough dry powder to bail-out the next recession.

But they are way too late. This time is different because getting prepped for the next crisis will first unleash a vicious circle of reverse cascades, uncoiling springs, flights from risk, deleveraging of carry trades and unfathomable like and similar unwinds inside the great bubbles fostered by the central banks over the last nine years.

The parabolic rise of BOJ’s balance sheet is only a slightly exaggerated form of what has happened worldwide, but what lurks inside is exactly the same: Namely, a cycle of plummeting financial asset prices that the “all-in” central banks will be powerless to reverse or even curtail.

Stated differently, this time there will be no March 2009 bottom and no maniacal central bank reflation of the bubble.

This time is different because this time the bubble will die.

Wow! RIP the world economy. Folks get some physical gold and silver door stops (wealth preservation), some good PM stocks (future investment) because the ride is going to be epic. Don’t buy ANY paper PM’s they will be worthless because they are oversold 100 times, good luck trying to collect your physical product. Stay very nimble and get out of as much debt as you can as fast as you can. Be safe.